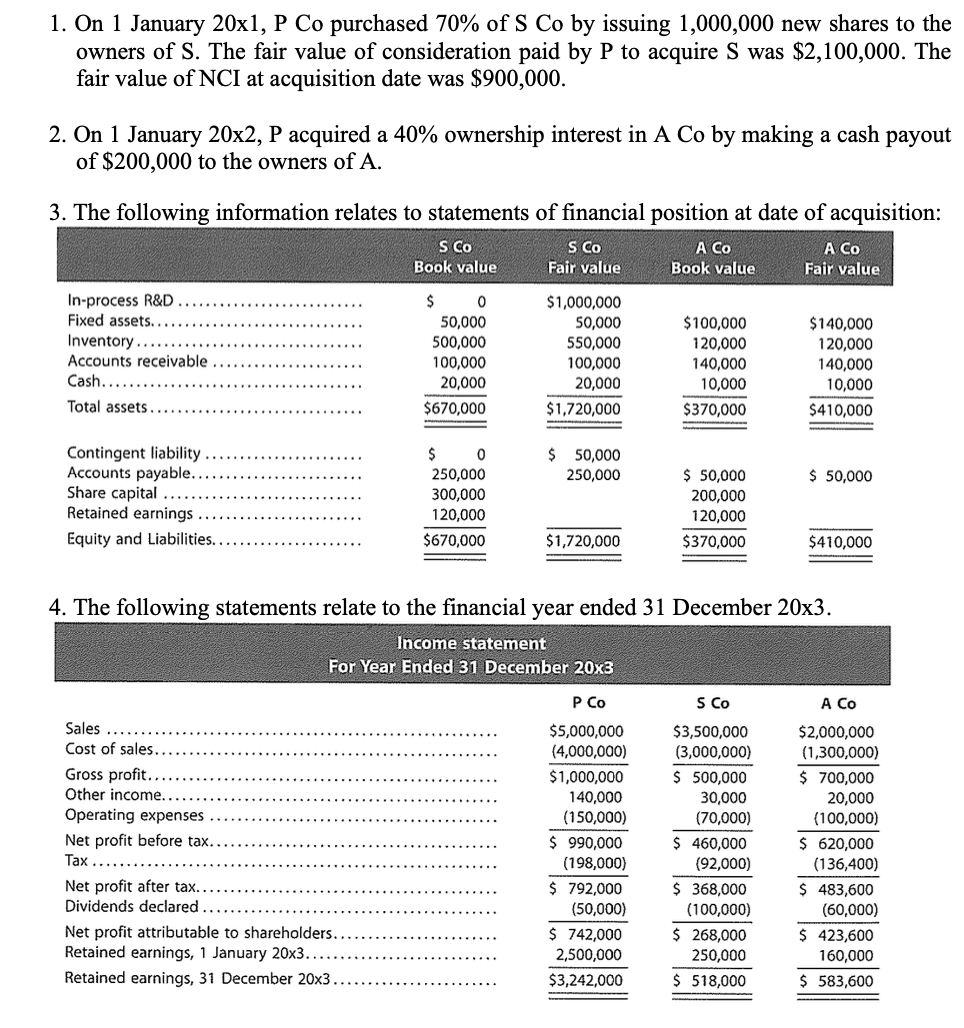

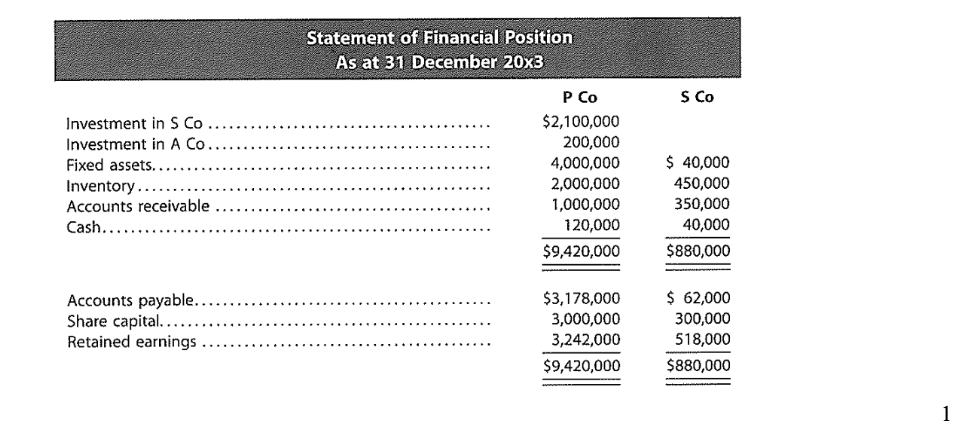

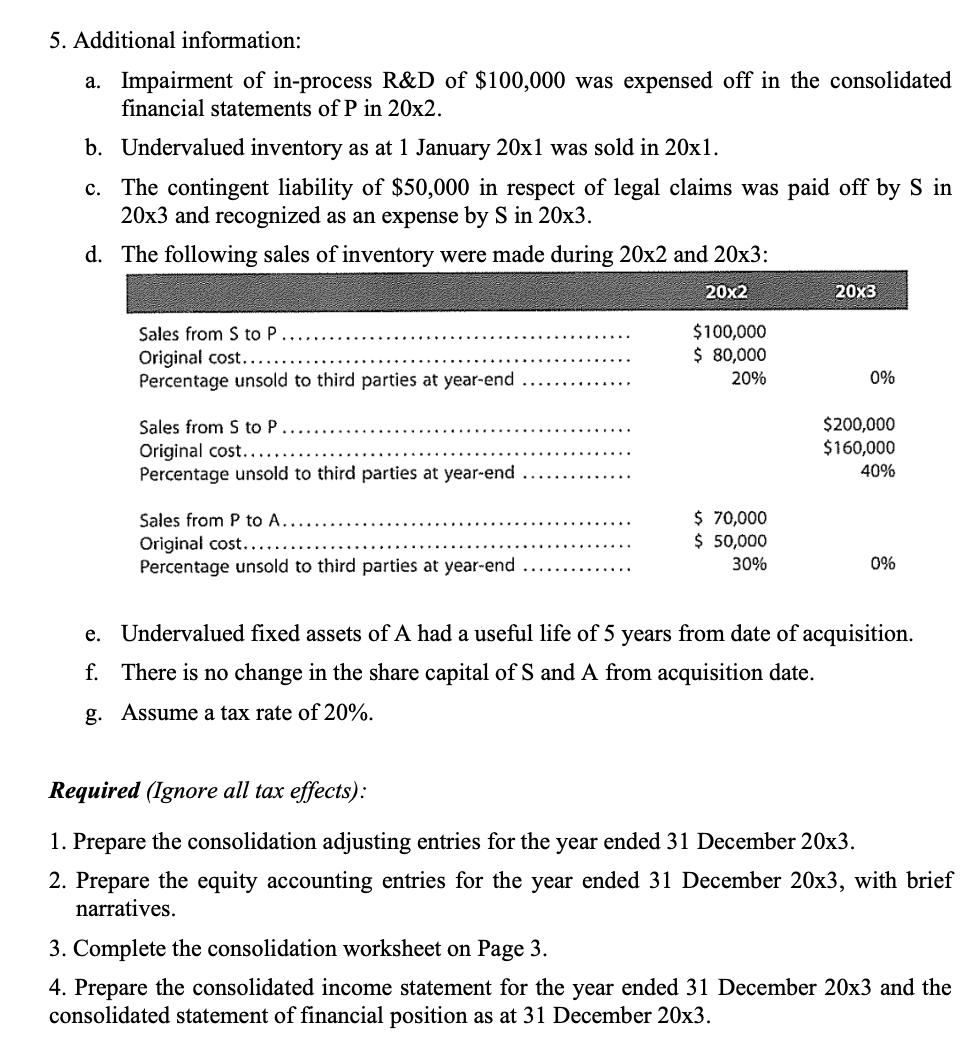

1. On 1 January 20x1, P Co purchased 70% of S Co by issuing 1,000,000 new shares to the owners of S. The fair value of consideration paid by P to acquire S was $2,100,000. The fair value of NCI at acquisition date was $900,000. 2. On 1 January 20x2, P acquired a 40% ownership interest in A Co by making a cash payout of $200,000 to the owners of A. 3. The following information relates to statements of financial position at date of acquisition: SCO Book value S Co Fair value A CO Book value Fair value In-process R&D Fixed assets.. Inventory Accounts receivable Cash.. Total assets $ 0 50,000 500,000 100,000 20,000 $670,000 $1,000,000 50,000 550,000 100,000 20,000 $1,720,000 $100,000 120,000 140,000 10,000 $370,000 $140,000 120,000 140,000 10,000 $410,000 $ 50,000 250,000 $ 50,000 Contingent liability Accounts payable. Share capital Retained earnings Equity and Liabilities.. $ 0 250,000 300,000 120,000 $670,000 $ 50,000 200,000 120,000 $370,000 $1,720,000 $410,000 4. The following statements relate to the financial year ended 31 December 20x3. Income statement For Year Ended 31 December 20x3 SCO A CO Sales Cost of sales Gross profit.. Other income.. Operating expenses Net profit before tax... Tax Net profit after tax.. Dividends declared Net profit attributable to shareholders... Retained earnings, 1 January 20x3. Retained earnings, 31 December 2003 $5,000,000 (4,000,000) $1,000,000 140,000 (150,000) $ 990,000 (198,000) $ 792,000 (50,000) $ 742,000 2,500,000 $3,242,000 $3,500,000 (3,000,000) $ 500,000 30,000 (70,000) $ 460,000 (92,000) 368,000 (100,000) $ 268,000 250,000 518,000 $2,000,000 (1,300,000) $ 700,000 20,000 (100,000) $ 620,000 (136,400) $ 483,600 (60,000) $ 423,600 160,000 $ 583,600 Statement of Financial Position As at 31 December 20x3 P Co SCO Investment in S Co Investment in A CO Fixed assets. Inventory Accounts receivable Cash.. $2,100,000 200,000 4,000,000 2,000,000 1,000,000 120,000 $9,420,000 $ 40,000 450,000 350,000 40,000 $880,000 Accounts payable. Share capital... Retained earnings $3,178,000 3,000,000 3,242,000 $9,420,000 $ 62,000 300,000 518,000 $880,000 1 5. Additional information: a. Impairment of in-process R&D of $100,000 was expensed off in the consolidated financial statements of P in 20x2. b. Undervalued inventory as at 1 January 20xl was sold in 20x1. c. The contingent liability of $50,000 in respect of legal claims was paid off by S in 20x3 and recognized as an expense by S in 20x3. d. The following sales of inventory were made during 20x2 and 20x3: 20x2 20x3 Sales from S to P Original cost. Percentage unsold to third parties at year-end $100,000 $ 80,000 20% 0% Sales from S to P Original cost..... Percentage unsold to third parties at year-end $200,000 $160,000 40% Sales from P to A.... Original cost.. Percentage unsold to third parties at year-end $ 70,000 $ 50,000 30% 096 e. Undervalued fixed assets of A had a useful life of 5 years from date of acquisition. f. There is no change in the share capital of S and A from acquisition date. g. Assume a tax rate of 20%. Required (Ignore all tax effects): 1. Prepare the consolidation adjusting entries for the year ended 31 December 20x3. 2. Prepare the equity accounting entries for the year ended 31 December 20x3, with brief narratives. 3. Complete the consolidation worksheet on Page 3. 4. Prepare the consolidated income statement for the year ended 31 December 20x3 and the consolidated statement of financial position as at 31 December 20x3. 1. On 1 January 20x1, P Co purchased 70% of S Co by issuing 1,000,000 new shares to the owners of S. The fair value of consideration paid by P to acquire S was $2,100,000. The fair value of NCI at acquisition date was $900,000. 2. On 1 January 20x2, P acquired a 40% ownership interest in A Co by making a cash payout of $200,000 to the owners of A. 3. The following information relates to statements of financial position at date of acquisition: SCO Book value S Co Fair value A CO Book value Fair value In-process R&D Fixed assets.. Inventory Accounts receivable Cash.. Total assets $ 0 50,000 500,000 100,000 20,000 $670,000 $1,000,000 50,000 550,000 100,000 20,000 $1,720,000 $100,000 120,000 140,000 10,000 $370,000 $140,000 120,000 140,000 10,000 $410,000 $ 50,000 250,000 $ 50,000 Contingent liability Accounts payable. Share capital Retained earnings Equity and Liabilities.. $ 0 250,000 300,000 120,000 $670,000 $ 50,000 200,000 120,000 $370,000 $1,720,000 $410,000 4. The following statements relate to the financial year ended 31 December 20x3. Income statement For Year Ended 31 December 20x3 SCO A CO Sales Cost of sales Gross profit.. Other income.. Operating expenses Net profit before tax... Tax Net profit after tax.. Dividends declared Net profit attributable to shareholders... Retained earnings, 1 January 20x3. Retained earnings, 31 December 2003 $5,000,000 (4,000,000) $1,000,000 140,000 (150,000) $ 990,000 (198,000) $ 792,000 (50,000) $ 742,000 2,500,000 $3,242,000 $3,500,000 (3,000,000) $ 500,000 30,000 (70,000) $ 460,000 (92,000) 368,000 (100,000) $ 268,000 250,000 518,000 $2,000,000 (1,300,000) $ 700,000 20,000 (100,000) $ 620,000 (136,400) $ 483,600 (60,000) $ 423,600 160,000 $ 583,600 Statement of Financial Position As at 31 December 20x3 P Co SCO Investment in S Co Investment in A CO Fixed assets. Inventory Accounts receivable Cash.. $2,100,000 200,000 4,000,000 2,000,000 1,000,000 120,000 $9,420,000 $ 40,000 450,000 350,000 40,000 $880,000 Accounts payable. Share capital... Retained earnings $3,178,000 3,000,000 3,242,000 $9,420,000 $ 62,000 300,000 518,000 $880,000 1 5. Additional information: a. Impairment of in-process R&D of $100,000 was expensed off in the consolidated financial statements of P in 20x2. b. Undervalued inventory as at 1 January 20xl was sold in 20x1. c. The contingent liability of $50,000 in respect of legal claims was paid off by S in 20x3 and recognized as an expense by S in 20x3. d. The following sales of inventory were made during 20x2 and 20x3: 20x2 20x3 Sales from S to P Original cost. Percentage unsold to third parties at year-end $100,000 $ 80,000 20% 0% Sales from S to P Original cost..... Percentage unsold to third parties at year-end $200,000 $160,000 40% Sales from P to A.... Original cost.. Percentage unsold to third parties at year-end $ 70,000 $ 50,000 30% 096 e. Undervalued fixed assets of A had a useful life of 5 years from date of acquisition. f. There is no change in the share capital of S and A from acquisition date. g. Assume a tax rate of 20%. Required (Ignore all tax effects): 1. Prepare the consolidation adjusting entries for the year ended 31 December 20x3. 2. Prepare the equity accounting entries for the year ended 31 December 20x3, with brief narratives. 3. Complete the consolidation worksheet on Page 3. 4. Prepare the consolidated income statement for the year ended 31 December 20x3 and the consolidated statement of financial position as at 31 December 20x3