Answered step by step

Verified Expert Solution

Question

1 Approved Answer

(1 point) For all the problems in this section, use the binomial tree model. Unless otherwise stated, assume no arbitrage. The current spot price of

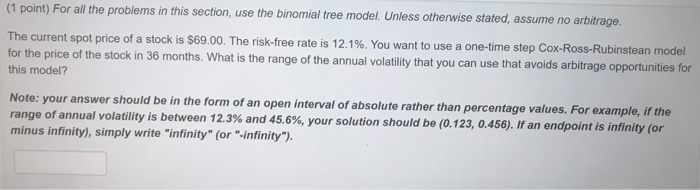

(1 point) For all the problems in this section, use the binomial tree model. Unless otherwise stated, assume no arbitrage. The current spot price of a stock is $69.00. The risk-free rate is 12.1%. You want to use a one-time step Cox-Ross-Rubinstean model for the price of the stock in 36 months. What is the range of the annual volatility that you can use that avoids arbitrage opportunities for this model? Note: your answer should be in the form of an open interval of absolute rather than percentage values. For example, if the range of annual volatility is between 12.3% and 45.6%, your solution should be (0.123, 0.456). If an endpoint is infinity (or minus infinity), simply write "infinity" (or "-infinity")

(1 point) For all the problems in this section, use the binomial tree model. Unless otherwise stated, assume no arbitrage. The current spot price of a stock is $69.00. The risk-free rate is 12.1%. You want to use a one-time step Cox-Ross-Rubinstean model for the price of the stock in 36 months. What is the range of the annual volatility that you can use that avoids arbitrage opportunities for this model? Note: your answer should be in the form of an open interval of absolute rather than percentage values. For example, if the range of annual volatility is between 12.3% and 45.6%, your solution should be (0.123, 0.456). If an endpoint is infinity (or minus infinity), simply write "infinity" (or "-infinity")

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Climate Finance Theory And Practice

Authors: Anil Markandya, Ibon Galarraga, Dirk Rübbelke

1st Edition

9814641804, 978-9814641807