Question

1] Read the article: CH8 Discussion Board - Bob's Bicycles 2] Respond to the following questions: List one reason discussed for the direct labor efficiency

1] Read the article: CH8 Discussion Board - Bob's Bicycles

2] Respond to the following questions: List one reason discussed for the direct labor efficiency variance for Bob's bicycles. List one reason discussed for the total direct materials variance for Bob's bicycles. List one of the three important facts to keep in mind when calculating overhead variances.

[3] Respond to a classmates post and list one interesting thing you found about the article.

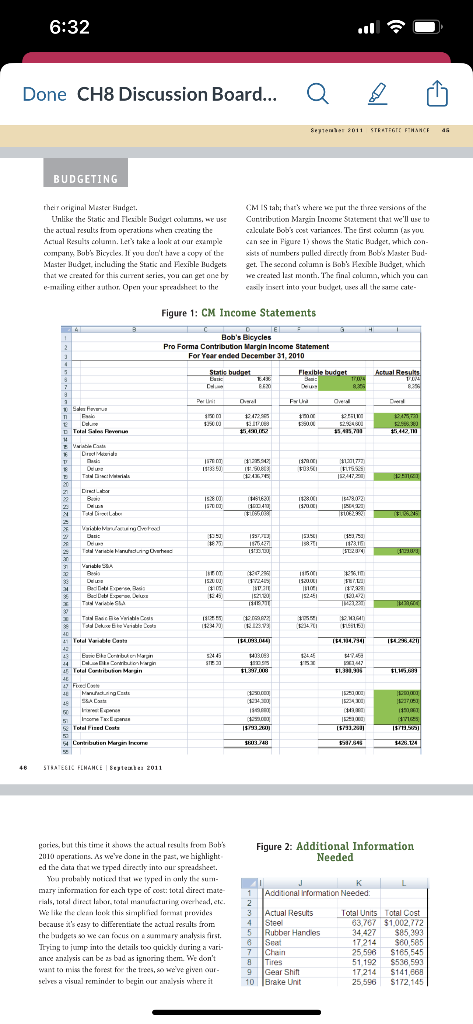

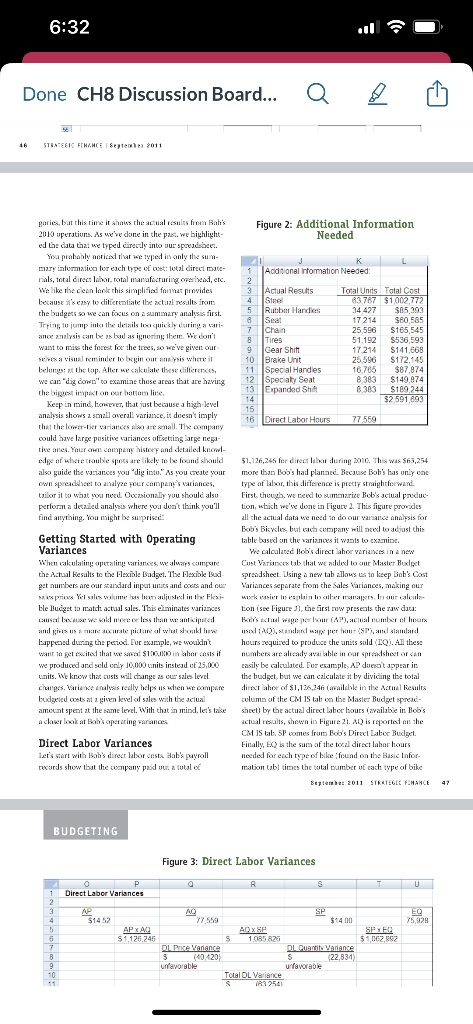

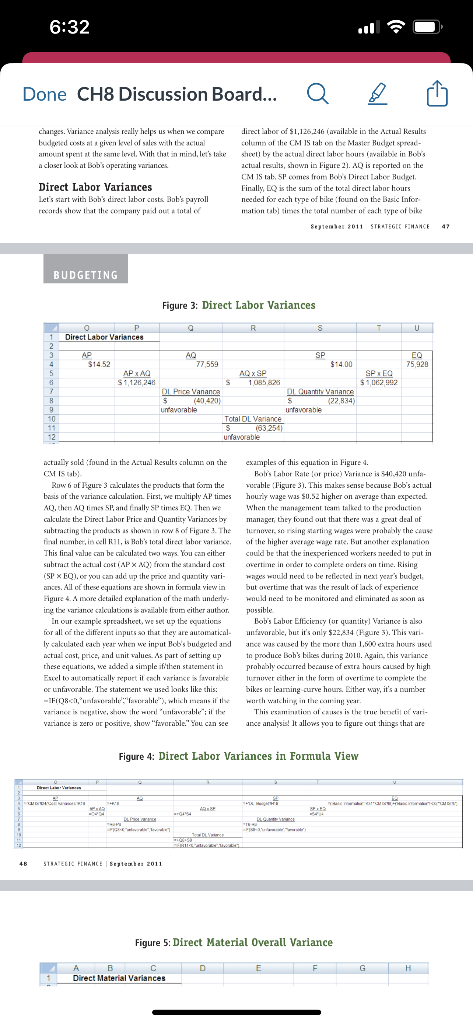

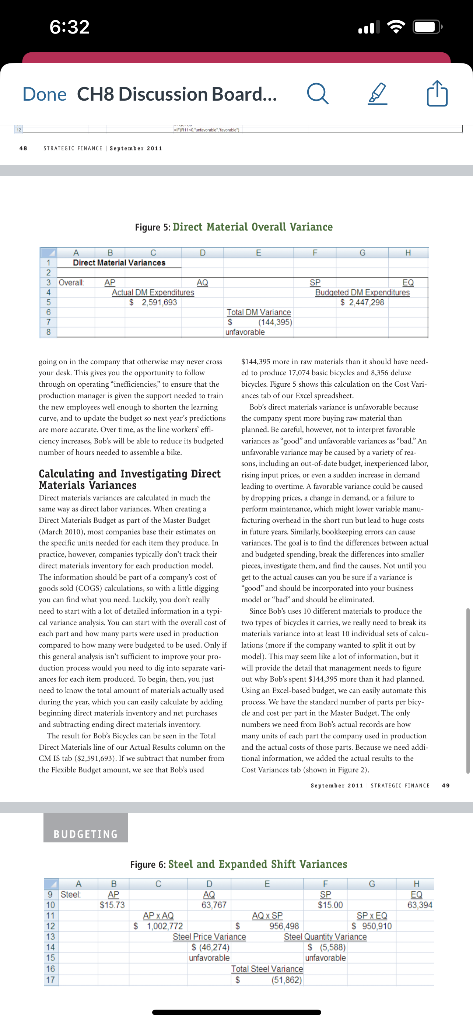

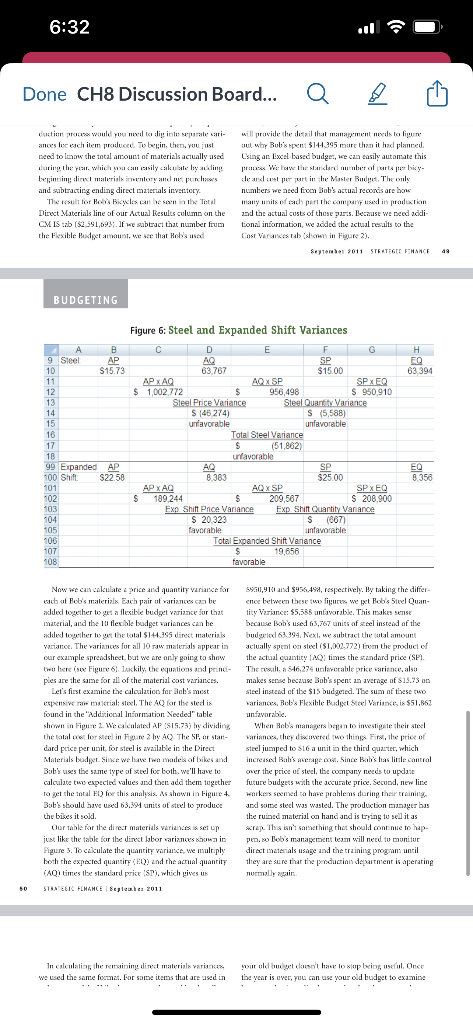

Completing a Benchmarking Analysis with Your Excel-based Master Budget By Jason Porter and Teresa Stephenson, CMA udgeting. One the year is ower, anmpany lenders chen think that the budget no kinge exres a purpose. The eccuintans and mandgemeat ream rypically apend a gear deal of tine and energy creating, the budget but then the yeur winds to a close, and the budget is pushed to une side or thrown into the made. What belp could the old bodget be cow? Bat thewwing wuzy a good budget at the end of the verr anahyses allows you to ainist the story: to see haw the company performed, when it deviztsd from the plan, and why thuse deviations vocurred. It also prorides you with tbe tools to crezte a more contincing story-a more zecurate badget-nest yea: This is the third and Einal attice in our series descrit- Creating the Actual Contribution ing haw you can use an Fxch-basa. Master Badge for Margin. Income Statement making managerial decisiuns, In the first arbicle, we la the first two articles oc this series, we created two of safety fur Bub's Bicies. In the stoond article we crested July 2011i using the information from Bub's Master Bada Flexible Budess and started analyzing the compary's get toriginally deueleped in Strangie finarce, Fehruarysakes and contribution margin vaciances. In this artick, July 2010 , Neat tame the Flesble Budpe i,Augus. 201]: we examine Beb's actual results and use thera to chkculate using the budgesed production infurmation but actual the company' aperating variarces. In deiag sa, we hope sales quentities. This mooth we add the last "budget," to provide crough details and tiscussiva 90 you can use which istit really a budpet at all, even it it does ret theee tools to analyre zamy type of businese Unfortunately lumped in with the bailyets lnstead. this final statement we won't he able to loak at eret posible rype of operat- reports actual results in the Contribution Margis lncane tant exmples and discuss their implications. managers to ezsily compare actual results side by side So fire up your spradshes, werm up your calculator, with the original budget and the variable budgee, and stech your fingers, and letis pal Hhey can invelipate the dilliererees, ar carianes, frum BUDGETING theif ariginal Misca Bulget. Sh. [S tali; that's where we out ite thece rensinas af the Wnlike the Static and Rexible Buciget columns, we use Cuntribution Blargi Inoune Staternent that we'll use to the astuil results from oferstions when creating the czksulate Lob's cost variances. To: first coiarn (is you ompany Bob's Bicytles. If wou dua't have a woyy of the sists of numbers pulled direttly from Beb's Miater BudMaster Hudget, iscluding the Staric and Fexible Hudgets get. The second odamn is Bab's Hexihle Hudget, whidh thet we created for th s curent seriss, you can get ane by we creatod las month. The final column, which wou can e-mailing either author. Open your spreadehert to the easly insert into syour budget, uses all the same cate- Fiqure 1: CM Income Statements rhes original Mesras Hudpet. S.M IS tah; thar's where we pur the three persions of the Unlike the Static and Flesible Buiget oolumns, wx use Centribution Mlargin Lnoune Statement that we'll use to the attual results frum operations when treating the cikeulate Eob's cot variances. Tae first coiarn (as yvu. Actual Results calumin. Ler's raka a lank at oar example cen sac in Figure 1) show the Static Badger, which oonommexny Bab's Bicrtes. It sua doc't have a topy of be sists of numbers pulled directly from Bob's Mister BudAlater liudget, iscluding the Static and Fexible ludgets get. The second oolamn is Eab's Flexible llodget, whidu that we created for this curent series, you can get ose by we creatod last month. The nal columus, which you car Figure 1: CM Income Statements paries but this tire it shaus the ac ual rewits form Babis Figure 2: Additional Information 2010 operations. A s we'e done in the pass, we lighlight Needed ed the data that we tfped directly into aur spreddstiee. mary information for euch trpe of cost: total direct mave rials, tosal dircen lahki, rotal niaiufacrurieg ortel wakl, cre. Wie like the e ein lact this simpli iod formul provides because it's easy to differratiate the watal resalt fromrhe lvadpes wo we san fokits nn a summe re aitalys fic it. Trying to jump into the details too quickly daring a sriance zalysis zan be as bad as ignering them. Wr don't wait ra nive the forme for the trbes, so meve gisen carseives a visuzl reminder to begin out anzirsis where it gaties, bat this rimx it ahawx the acual resules from Bahis Figure 2: Additional Information. 2010 uperations. As we've done in the past. we highlightNeeded ed the data that ue typed direcdy into vur spoedibeet. Yisa prabahly noricad thar we typed in anly the sunmury intormation for each trpe of ovet: total direct mateWe like the ceen lank this simplifind fonmat prowides becaus itisesy to ditferentiate tbe actal resalts from the budgess so we can focus on a summary analysis first. Trping, to jump inta the delsils too quickly daring a sariance amalysis can be as tad as ipnering, them. We don' want to miss the forest for the trees, so weve given our sehro a visual remimler to begin our amk rsis whate it beleng: an the top, After we cakulate these tilfereses, we can "dig down" 00 examias those arms that are hzving the biggest inpiot on cur botam lire. Kezp in mind, bowerer, that just because a high-level analysis shows 2 small overall warimse, is doesn't imply that the lomet-tict varianees alsa are senall. The oompany could have large pusitive cariances aftseting arge negathe anes. thur oten company histor and detailed knowialso guide the variances you "dig into." As you create your more than Boo's had planned. Becuuse Bob's bas uniy cose own speadklaet to analye pour company's varianoes, type of labor, this difference is precty straightfowewe. tailor it ta wat you necd. Ooczsionally you sbould also First thewgh, we ceed to semenarie Bob's actual producperform a detriled analysis where yoa doa't think you'll Eon, which we've done in Figure 2. This figure prorides find anything. You might be suprised: all the actual data we need to do our varianee analrsis for Getting Started with Operating table bosed an the sariznoxs it wants to exnanine. Variances Whe calcalaed lobis diroct lahoe veriaks in a new When cakulating speraling sariances, ue aluars campare Cust Viriascer tab that we added to dur Master Budpet the Natual Besults to the Fexible Badget. Tbe Fexibke Eod- spresdsheet. Using a new tab allous us to lisep Bab's Cost get nurrbers are our stardard input unirs and ooess and our Wariances separate from the Sales Variances, making our ble Budget to math attual sales. This eiminates variznes ton iste Figure 3 l the first raw preseats the raw data: bappesed during the peiod. For exumpl, ws woukdnt heurs requized to prodoce the anits sold IQ!. All thes: watr to get exited that we sacat \$100mo in laber casts if numbers are alteady avsi able in oar spreadsheer of \&an we produced ard seld only 10,000 units instead of 25,000 tasily be calculated. For example, 2 doesct appear in cnits. We know that custs will thange is cue sales levet the budget, but we can calculate it ty divicing the total chargss. variake unalywis reilly helps us uten we compare dimt abox of $1,136,246 (arailable in the saruel results budgeived oots at 2 given kvel of sales with the actual celumn of the CM 15 tab on the Master Budget spreacamount spent 2t the same level. With that in mind, let's taixe sheet) by the actual direct laber bours izailabie in Bob's Direct IS tab. SP comes fram Bob's Dirct Laboc Budget. Direct Labor Variances Sinally, EQ is the sum of the tocal direct labar hours let's start with Bob's direct labor cnsta Bab's payroll needed for each type of bike ifound on the Basic Inforrecords show that the coanpany prid out a tutal of mation tabl times the tatal namber of cach type of bike Bepienbez 2011 SIketsite f.haAct BUDGETING Figure 3: Direct Labor Variances Done CH8 Discussion Board... charges. varizese znalysis really helps us when we compare direct laboe of $1,126,246 (arailable in the Actuz] Results ameent spert th the same lert, With the in mind, leits taise shextl by the actusl direct laber baurs iavailabe in Bob's a claser look at Eob's operating varinces actual resalts, shewn in Figure 2). AQ is reported an the CM 15 tab, 5T oomes fram Bodrs Dircel laber Budpel. Direct Labor Variances Einally, DQ is the sura of the bocz direct labor hours Let's start with Bob's direct labor casts. Bab's payroll needed for ezch thpe of bilie ;found on the Bisic Infor: roards show that the connany padid aus a total of mation tabl timats the catal mamber of tadt type of bike BUDGETING Figure 3: Direct Labor Variances actually sold ;found in the Actual Results calemn on the examples of this equation in Figure 4. C.M IS [ab? Bolis [aber Rate lor price) Variene is 5+40,420 unfa- Rnw 6 of Jqure 3 rakulabes the pouducts that form the wocable :Tigare 3). This malies sense because Bob's actual bas of the variance calculation. Eirst, we maltiply AP times houry wage was \$0.52 higher on arerage than expected. AQ, thet AQ times 5P, and finally SP times FQ. Thes we When the manigement tam talked ra the producaion cakulate the Direct labor Prise and Quantity Varianoes by manager, they found out that there was z great deal of This firal salue san be cakulated twa ways. Vou can either could be that the inexperienced wocksers aceded to put in subtract the actual wst IAP W. from the s.axlard cost owertine in order to canplere ordera an time. Rising (SP EQ), or you can add up the prooe wod quantity sari- wages wudd ned to be refletted in next year's budget. ances. All of thex equations are shewn in formula view in but atertime that was the result of lack of experience Higure 4. A more detaikd explanation of the math anderly- wokd need to he monitored and eliminated as son as ing be sariano taleubtions is anilable from either autbor. pussible. In our exzmple spreadshect, we set up tbe eantions Bob's Labur Effeciency (or quantity) variance is also for all of the different inputs $ that they are autamatical- unfavardbe, hur it's anly $22, s.4 . Fgure 31 . This varily sakulated each par when we input Bob's budgeted and aroe was caused by the mare than l.500 eatra hours used octual cast, peice, and unit values. As part of setting up to produce Bob's bilies during 201t. Aggain, this variance these equations, we added a simple ifithen statensent in prohably occurred because of extra haurs cuused by high Eucel to auturatitally repurt it ench variance is faveralat furnuser vither in the furm at awrlime to complete be or enfuocable. The statersent we used lonks like this: bikes ar learning curve hours. Either way, it's a namber vatiance is zero ar positive, shew "favorable." Wou can see ance analysis! lt allows you to figure out things that are Figure 4: Direct Labor Variances in Formula View Figure 5: Direct Material Overall Variance Figure 5: Direct Material Overall Variance thrugh on cperatizg "inefliciencies" to ensure that the bicytes Nagure 5 shews this calculation en the Cest Varicurve, and to update the badget so next verr's predictions the cumpony spent mone bucing zaw material than are mare accarare. Oyer time as the libe workers' eff- plannoti. Be arefill however, not ta iweapme fovarable ciency increses, Bub's will be able to reduke its budgeted sariznes 2 " pood and unfwwerable variances as "bad." An number of hoars needed to assemble a bilis. Unfavonable veranoe mar be calsed by a rariaty of reaCalculating and Investigating Direct sising, inpul priks or cwen a sibder intras in dersand MaterialsVarianceskisingingtoorikertineAdfavarablewariasecoudbecaused Dicext malerials veriatcts are taleulated in mude the by dopping prics, a ctange in datiand or a failure to same uay as diext laber varianes. When crealicg a pertorm maiblerano, which might lower sariabke maneDirect Materials Dodget as part of the Master Budget focturing onetsead in the shart rea but lead to huge costs practice, however, companies typoczlly con't track their and budgeted spending, break the differences into smaller direer materials insentary for each prodectian modk. pioces, imstigate thetm, and find the causes, Nos unil poup The information sbould be part of a company's cost of get to the actuz causes can you be sure if a variance is gocds sold (CoGs) calculations, sa with a litte digging "good" axd shauld be incorporated into pour bezesess need to start with a lot of detzied inforation in a topi- Since Bob's lses lo diEerent anateials to produce the cal verance analis. You con star with the oxeroll cast of twa tfpes of hicydes it carrien, we really need ta break its each part and haw many parts were used in production materiak mariance into at least In individual sess af cakincompored to bow many were budyeted to be used. Only if latives imuce if the company wanted to split it wat by this geseral asalysis inn't sufficient to improne pour pro- modeli. This may sem like 2 lot of isformation, bat it ciotien procke wsuld pou need to die inlo sxparate sari- will pracide the detail that management needs to ligune ances for exch item produced. To begin, then, vou, just out wiry Bub's spen: \$141395 more then it had planced. bed to lane the total anount of materiak actually ased I.sing an Exal-based budees, we can easily autamate this befinning direct materials imexntory and net purchases de and cost per pert in the Master Budect. The only and sabtracting ending direct materials inventory. numbers we aced fiom liob's actual reoond are hoe Direct Materials line of our Actual Besuls column on the and the actual cost of those parts. Because we beed zdiCM IS tab i $2,351,699;. If we subteact that number from tonal information, we aded the actual resilts to the Cost Virarcicobb istamo in Figure 2). segleabeE c011 STKETEGC FIHANCE BUDGETING Figure 6: Steel and Expanded Shift Variances beed to taaw the total amount of materiaks actually ased Lsing an Exel based budges, we can easily autamate this and subtracting ending direct mattrials inventecy. numbers we ased ficon Bob's actual reconds are bow Direct Materials line of our Actual Besults sulume on the esd the actual susts of these per:s. Because we beed addiCM is :ab i $2,391,693. If we sabtact that number frum tonal information, we zided the actual res.lts to the the Fexitle Hedser amaum, ve sec that Hobs usad Cosr Viramces ab isdonon in Figure 2 ). sepienber so11 stketeger frhance 49 BUDGETING Figure 6: Steel and Expanded Shift Variances Now we can cakulate 2 price and quantitf veriase for Ss 511,4101 and $45 s.ts4, respectively. By taking the differtasth af Bebb's materialx. Exch pair of rariances caa be ence between these tuo figurec ue pet Bob's 5teel Quanadded together to get a flexille budget varimae for that tity Viriance: 55,535 untaworable. This make sense material, ard the it flewhle budget varianoes can be becabse bob's used 63,767 units of steel insteid of the veriance. The rariznos fur all 10raw materals appest in setually spent on steel (\$1,002,772) form the product of our example spreodshest, but we are only gaing ta show the actual chaaticy (MQ) times the standard price iSP). pies are the same for all of the material cost variances. makes sense beczuse Bab's spent a average of $15.93 ou Let's first examise the calculation far Bab's mest stel insted of the $15 budgeted. The sum of these tho found in the "?ddiriccal lnsormation Needed" table unfiworible. shown in Figue 2. We ciculated if : {515,73 ) l diwiding When Reb's mantgers began to imestigne their stect the fotal oom for sleel in Figune 2 by AQ. The SF, or stan- varianos, they dioxavered too thinge Fire, the price of dard peice per unit, for steel is wavilakle in the Direct steel jumped to 816 a unit in the third couster, which Bob's uses the same type of sted for both. we'll have to over the price of stell, the conpony needs to update calculate two expected values and tien add them twgether future budgess with the accurate price. Second, new line to get the total fiq foe this analysis. A shown in Figure 4. werkes soensed ta hawe prablens during their troining Bobb's soould bave weed 63,394 units of sted to produce and some stecl was wasted. The production camper bas the bikes it sold. the ruined material on hand and is tring to sel it as Our tabk for the dimer materials werialces is set up siep. Thas inn't samsthing thet should onnt nue to hapHigure 3. To cakulate the quantity Fariasse, we multiply dirat materials usage and the training progens until (AQ! times tbe standard price 'SP), which gives us nermblly zesain. Completing a Benchmarking Analysis with Your Excel-based Master Budget By Jason Porter and Teresa Stephenson, CMA udgeting. One the year is ower, anmpany lenders chen think that the budget no kinge exres a purpose. The eccuintans and mandgemeat ream rypically apend a gear deal of tine and energy creating, the budget but then the yeur winds to a close, and the budget is pushed to une side or thrown into the made. What belp could the old bodget be cow? Bat thewwing wuzy a good budget at the end of the verr anahyses allows you to ainist the story: to see haw the company performed, when it deviztsd from the plan, and why thuse deviations vocurred. It also prorides you with tbe tools to crezte a more contincing story-a more zecurate badget-nest yea: This is the third and Einal attice in our series descrit- Creating the Actual Contribution ing haw you can use an Fxch-basa. Master Badge for Margin. Income Statement making managerial decisiuns, In the first arbicle, we la the first two articles oc this series, we created two of safety fur Bub's Bicies. In the stoond article we crested July 2011i using the information from Bub's Master Bada Flexible Budess and started analyzing the compary's get toriginally deueleped in Strangie finarce, Fehruarysakes and contribution margin vaciances. In this artick, July 2010 , Neat tame the Flesble Budpe i,Augus. 201]: we examine Beb's actual results and use thera to chkculate using the budgesed production infurmation but actual the company' aperating variarces. In deiag sa, we hope sales quentities. This mooth we add the last "budget," to provide crough details and tiscussiva 90 you can use which istit really a budpet at all, even it it does ret theee tools to analyre zamy type of businese Unfortunately lumped in with the bailyets lnstead. this final statement we won't he able to loak at eret posible rype of operat- reports actual results in the Contribution Margis lncane tant exmples and discuss their implications. managers to ezsily compare actual results side by side So fire up your spradshes, werm up your calculator, with the original budget and the variable budgee, and stech your fingers, and letis pal Hhey can invelipate the dilliererees, ar carianes, frum BUDGETING theif ariginal Misca Bulget. Sh. [S tali; that's where we out ite thece rensinas af the Wnlike the Static and Rexible Buciget columns, we use Cuntribution Blargi Inoune Staternent that we'll use to the astuil results from oferstions when creating the czksulate Lob's cost variances. To: first coiarn (is you ompany Bob's Bicytles. If wou dua't have a woyy of the sists of numbers pulled direttly from Beb's Miater BudMaster Hudget, iscluding the Staric and Fexible Hudgets get. The second odamn is Bab's Hexihle Hudget, whidh thet we created for th s curent seriss, you can get ane by we creatod las month. The final column, which wou can e-mailing either author. Open your spreadehert to the easly insert into syour budget, uses all the same cate- Fiqure 1: CM Income Statements rhes original Mesras Hudpet. S.M IS tah; thar's where we pur the three persions of the Unlike the Static and Flesible Buiget oolumns, wx use Centribution Mlargin Lnoune Statement that we'll use to the attual results frum operations when treating the cikeulate Eob's cot variances. Tae first coiarn (as yvu. Actual Results calumin. Ler's raka a lank at oar example cen sac in Figure 1) show the Static Badger, which oonommexny Bab's Bicrtes. It sua doc't have a topy of be sists of numbers pulled directly from Bob's Mister BudAlater liudget, iscluding the Static and Fexible ludgets get. The second oolamn is Eab's Flexible llodget, whidu that we created for this curent series, you can get ose by we creatod last month. The nal columus, which you car Figure 1: CM Income Statements paries but this tire it shaus the ac ual rewits form Babis Figure 2: Additional Information 2010 operations. A s we'e done in the pass, we lighlight Needed ed the data that we tfped directly into aur spreddstiee. mary information for euch trpe of cost: total direct mave rials, tosal dircen lahki, rotal niaiufacrurieg ortel wakl, cre. Wie like the e ein lact this simpli iod formul provides because it's easy to differratiate the watal resalt fromrhe lvadpes wo we san fokits nn a summe re aitalys fic it. Trying to jump into the details too quickly daring a sriance zalysis zan be as bad as ignering them. Wr don't wait ra nive the forme for the trbes, so meve gisen carseives a visuzl reminder to begin out anzirsis where it gaties, bat this rimx it ahawx the acual resules from Bahis Figure 2: Additional Information. 2010 uperations. As we've done in the past. we highlightNeeded ed the data that ue typed direcdy into vur spoedibeet. Yisa prabahly noricad thar we typed in anly the sunmury intormation for each trpe of ovet: total direct mateWe like the ceen lank this simplifind fonmat prowides becaus itisesy to ditferentiate tbe actal resalts from the budgess so we can focus on a summary analysis first. Trping, to jump inta the delsils too quickly daring a sariance amalysis can be as tad as ipnering, them. We don' want to miss the forest for the trees, so weve given our sehro a visual remimler to begin our amk rsis whate it beleng: an the top, After we cakulate these tilfereses, we can "dig down" 00 examias those arms that are hzving the biggest inpiot on cur botam lire. Kezp in mind, bowerer, that just because a high-level analysis shows 2 small overall warimse, is doesn't imply that the lomet-tict varianees alsa are senall. The oompany could have large pusitive cariances aftseting arge negathe anes. thur oten company histor and detailed knowialso guide the variances you "dig into." As you create your more than Boo's had planned. Becuuse Bob's bas uniy cose own speadklaet to analye pour company's varianoes, type of labor, this difference is precty straightfowewe. tailor it ta wat you necd. Ooczsionally you sbould also First thewgh, we ceed to semenarie Bob's actual producperform a detriled analysis where yoa doa't think you'll Eon, which we've done in Figure 2. This figure prorides find anything. You might be suprised: all the actual data we need to do our varianee analrsis for Getting Started with Operating table bosed an the sariznoxs it wants to exnanine. Variances Whe calcalaed lobis diroct lahoe veriaks in a new When cakulating speraling sariances, ue aluars campare Cust Viriascer tab that we added to dur Master Budpet the Natual Besults to the Fexible Badget. Tbe Fexibke Eod- spresdsheet. Using a new tab allous us to lisep Bab's Cost get nurrbers are our stardard input unirs and ooess and our Wariances separate from the Sales Variances, making our ble Budget to math attual sales. This eiminates variznes ton iste Figure 3 l the first raw preseats the raw data: bappesed during the peiod. For exumpl, ws woukdnt heurs requized to prodoce the anits sold IQ!. All thes: watr to get exited that we sacat \$100mo in laber casts if numbers are alteady avsi able in oar spreadsheer of \&an we produced ard seld only 10,000 units instead of 25,000 tasily be calculated. For example, 2 doesct appear in cnits. We know that custs will thange is cue sales levet the budget, but we can calculate it ty divicing the total chargss. variake unalywis reilly helps us uten we compare dimt abox of $1,136,246 (arailable in the saruel results budgeived oots at 2 given kvel of sales with the actual celumn of the CM 15 tab on the Master Budget spreacamount spent 2t the same level. With that in mind, let's taixe sheet) by the actual direct laber bours izailabie in Bob's Direct IS tab. SP comes fram Bob's Dirct Laboc Budget. Direct Labor Variances Sinally, EQ is the sum of the tocal direct labar hours let's start with Bob's direct labor cnsta Bab's payroll needed for each type of bike ifound on the Basic Inforrecords show that the coanpany prid out a tutal of mation tabl times the tatal namber of cach type of bike Bepienbez 2011 SIketsite f.haAct BUDGETING Figure 3: Direct Labor Variances Done CH8 Discussion Board... charges. varizese znalysis really helps us when we compare direct laboe of $1,126,246 (arailable in the Actuz] Results ameent spert th the same lert, With the in mind, leits taise shextl by the actusl direct laber baurs iavailabe in Bob's a claser look at Eob's operating varinces actual resalts, shewn in Figure 2). AQ is reported an the CM 15 tab, 5T oomes fram Bodrs Dircel laber Budpel. Direct Labor Variances Einally, DQ is the sura of the bocz direct labor hours Let's start with Bob's direct labor casts. Bab's payroll needed for ezch thpe of bilie ;found on the Bisic Infor: roards show that the connany padid aus a total of mation tabl timats the catal mamber of tadt type of bike BUDGETING Figure 3: Direct Labor Variances actually sold ;found in the Actual Results calemn on the examples of this equation in Figure 4. C.M IS [ab? Bolis [aber Rate lor price) Variene is 5+40,420 unfa- Rnw 6 of Jqure 3 rakulabes the pouducts that form the wocable :Tigare 3). This malies sense because Bob's actual bas of the variance calculation. Eirst, we maltiply AP times houry wage was \$0.52 higher on arerage than expected. AQ, thet AQ times 5P, and finally SP times FQ. Thes we When the manigement tam talked ra the producaion cakulate the Direct labor Prise and Quantity Varianoes by manager, they found out that there was z great deal of This firal salue san be cakulated twa ways. Vou can either could be that the inexperienced wocksers aceded to put in subtract the actual wst IAP W. from the s.axlard cost owertine in order to canplere ordera an time. Rising (SP EQ), or you can add up the prooe wod quantity sari- wages wudd ned to be refletted in next year's budget. ances. All of thex equations are shewn in formula view in but atertime that was the result of lack of experience Higure 4. A more detaikd explanation of the math anderly- wokd need to he monitored and eliminated as son as ing be sariano taleubtions is anilable from either autbor. pussible. In our exzmple spreadshect, we set up tbe eantions Bob's Labur Effeciency (or quantity) variance is also for all of the different inputs $ that they are autamatical- unfavardbe, hur it's anly $22, s.4 . Fgure 31 . This varily sakulated each par when we input Bob's budgeted and aroe was caused by the mare than l.500 eatra hours used octual cast, peice, and unit values. As part of setting up to produce Bob's bilies during 201t. Aggain, this variance these equations, we added a simple ifithen statensent in prohably occurred because of extra haurs cuused by high Eucel to auturatitally repurt it ench variance is faveralat furnuser vither in the furm at awrlime to complete be or enfuocable. The statersent we used lonks like this: bikes ar learning curve hours. Either way, it's a namber vatiance is zero ar positive, shew "favorable." Wou can see ance analysis! lt allows you to figure out things that are Figure 4: Direct Labor Variances in Formula View Figure 5: Direct Material Overall Variance Figure 5: Direct Material Overall Variance thrugh on cperatizg "inefliciencies" to ensure that the bicytes Nagure 5 shews this calculation en the Cest Varicurve, and to update the badget so next verr's predictions the cumpony spent mone bucing zaw material than are mare accarare. Oyer time as the libe workers' eff- plannoti. Be arefill however, not ta iweapme fovarable ciency increses, Bub's will be able to reduke its budgeted sariznes 2 " pood and unfwwerable variances as "bad." An number of hoars needed to assemble a bilis. Unfavonable veranoe mar be calsed by a rariaty of reaCalculating and Investigating Direct sising, inpul priks or cwen a sibder intras in dersand MaterialsVarianceskisingingtoorikertineAdfavarablewariasecoudbecaused Dicext malerials veriatcts are taleulated in mude the by dopping prics, a ctange in datiand or a failure to same uay as diext laber varianes. When crealicg a pertorm maiblerano, which might lower sariabke maneDirect Materials Dodget as part of the Master Budget focturing onetsead in the shart rea but lead to huge costs practice, however, companies typoczlly con't track their and budgeted spending, break the differences into smaller direer materials insentary for each prodectian modk. pioces, imstigate thetm, and find the causes, Nos unil poup The information sbould be part of a company's cost of get to the actuz causes can you be sure if a variance is gocds sold (CoGs) calculations, sa with a litte digging "good" axd shauld be incorporated into pour bezesess need to start with a lot of detzied inforation in a topi- Since Bob's lses lo diEerent anateials to produce the cal verance analis. You con star with the oxeroll cast of twa tfpes of hicydes it carrien, we really need ta break its each part and haw many parts were used in production materiak mariance into at least In individual sess af cakincompored to bow many were budyeted to be used. Only if latives imuce if the company wanted to split it wat by this geseral asalysis inn't sufficient to improne pour pro- modeli. This may sem like 2 lot of isformation, bat it ciotien procke wsuld pou need to die inlo sxparate sari- will pracide the detail that management needs to ligune ances for exch item produced. To begin, then, vou, just out wiry Bub's spen: \$141395 more then it had planced. bed to lane the total anount of materiak actually ased I.sing an Exal-based budees, we can easily autamate this befinning direct materials imexntory and net purchases de and cost per pert in the Master Budect. The only and sabtracting ending direct materials inventory. numbers we aced fiom liob's actual reoond are hoe Direct Materials line of our Actual Besuls column on the and the actual cost of those parts. Because we beed zdiCM IS tab i $2,351,699;. If we subteact that number from tonal information, we aded the actual resilts to the Cost Virarcicobb istamo in Figure 2). segleabeE c011 STKETEGC FIHANCE BUDGETING Figure 6: Steel and Expanded Shift Variances beed to taaw the total amount of materiaks actually ased Lsing an Exel based budges, we can easily autamate this and subtracting ending direct mattrials inventecy. numbers we ased ficon Bob's actual reconds are bow Direct Materials line of our Actual Besults sulume on the esd the actual susts of these per:s. Because we beed addiCM is :ab i $2,391,693. If we sabtact that number frum tonal information, we zided the actual res.lts to the the Fexitle Hedser amaum, ve sec that Hobs usad Cosr Viramces ab isdonon in Figure 2 ). sepienber so11 stketeger frhance 49 BUDGETING Figure 6: Steel and Expanded Shift Variances Now we can cakulate 2 price and quantitf veriase for Ss 511,4101 and $45 s.ts4, respectively. By taking the differtasth af Bebb's materialx. Exch pair of rariances caa be ence between these tuo figurec ue pet Bob's 5teel Quanadded together to get a flexille budget varimae for that tity Viriance: 55,535 untaworable. This make sense material, ard the it flewhle budget varianoes can be becabse bob's used 63,767 units of steel insteid of the veriance. The rariznos fur all 10raw materals appest in setually spent on steel (\$1,002,772) form the product of our example spreodshest, but we are only gaing ta show the actual chaaticy (MQ) times the standard price iSP). pies are the same for all of the material cost variances. makes sense beczuse Bab's spent a average of $15.93 ou Let's first examise the calculation far Bab's mest stel insted of the $15 budgeted. The sum of these tho found in the "?ddiriccal lnsormation Needed" table unfiworible. shown in Figue 2. We ciculated if : {515,73 ) l diwiding When Reb's mantgers began to imestigne their stect the fotal oom for sleel in Figune 2 by AQ. The SF, or stan- varianos, they dioxavered too thinge Fire, the price of dard peice per unit, for steel is wavilakle in the Direct steel jumped to 816 a unit in the third couster, which Bob's uses the same type of sted for both. we'll have to over the price of stell, the conpony needs to update calculate two expected values and tien add them twgether future budgess with the accurate price. Second, new line to get the total fiq foe this analysis. A shown in Figure 4. werkes soensed ta hawe prablens during their troining Bobb's soould bave weed 63,394 units of sted to produce and some stecl was wasted. The production camper bas the bikes it sold. the ruined material on hand and is tring to sel it as Our tabk for the dimer materials werialces is set up siep. Thas inn't samsthing thet should onnt nue to hapHigure 3. To cakulate the quantity Fariasse, we multiply dirat materials usage and the training progens until (AQ! times tbe standard price 'SP), which gives us nermblly zesainStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Auditing A Business Risk Approach

Authors: Karla Johnstone, Audrey Gramling, Larry Rittenberg

8th edition

538476230, 978-0538476232