Answered step by step

Verified Expert Solution

Question

1 Approved Answer

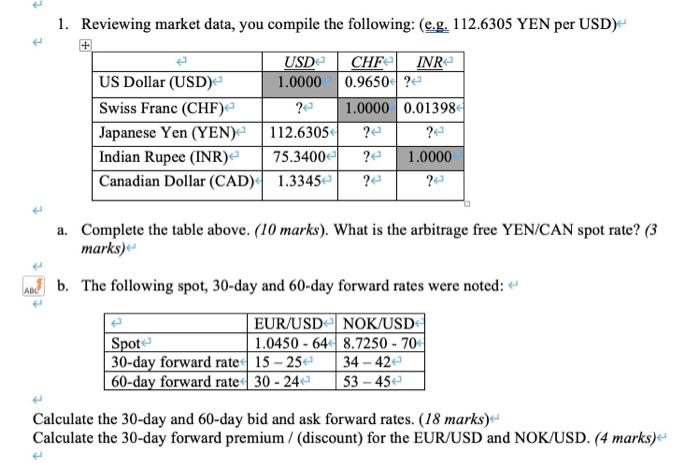

1. Reviewing market data, you compile the following: (e.g. 112.6305 YEN per USD) USD US Dollar (USD) 1.0000 Swiss Franc (CHF) ? Japanese Yen (YEN)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Market Takers Edge Insider Strategies From The Options Trading Floor

Authors: Dan Passarelli

1st Edition

007175492X,0071754946