Answered step by step

Verified Expert Solution

Question

1 Approved Answer

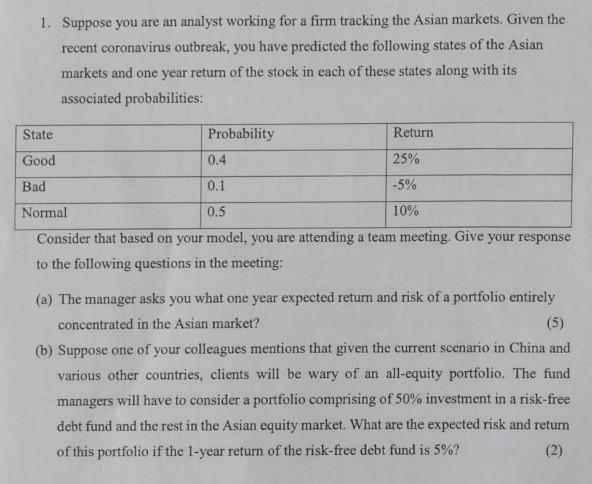

1. Suppose you are an analyst working for a firm tracking the Asian markets. Given the recent coronavirus outbreak, you have predicted the following states

1. Suppose you are an analyst working for a firm tracking the Asian markets. Given the recent coronavirus outbreak, you have predicted the following states of the Asian markets and one year return of the stock in each of these states along with its associated probabilities: Consider that based on your model, you are attending a team meeting. Give your response to the following questions in the meeting: (a) The manager asks you what one year expected return and risk of a portfolio entirely concentrated in the Asian market? (b) Suppose one of your colleagues mentions that given the current scenario in China and various other countries, clients will be wary of an all-equity portfolio. The fund managers will have to consider a portfolio comprising of 50% investment in a risk-free debt fund and the rest in the Asian equity market. What are the expected risk and return of this portfolio if the 1-year return of the risk-free debt fund is 5%

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Moorad Choudhry Anthology Website Past Present And Future Principles Of Banking And Finance

Authors: Moorad Choudhry

1st Edition

1118779738, 978-1118779736