1. Take Home Question #1: Conceptual Framework

Re: A New Era in Revenue Recognition Case Study: General Dynamics

On pages 11 & 12 of the case study, General Dynamics disclosed the role of estimates in determining reported contract revenue and costs.

Question: Is General Dynamics disclosure consistent with the objective of financial reporting? Why or Why not?

In drafting your answer, consider the following questions:

- What is the role of uncertainty in financial reporting?

- Will current and prospective capital providers find the information useful in making and monitoring their decisions? Why or why not?

- Is the disclosure consistent with the qualitative characteristics of financial information, specifically relevance and faithful representation? Why or why not?

why did the FASB required this type of reporting ?

How does the conceptual framework apply to the General Dynamics disclosure?

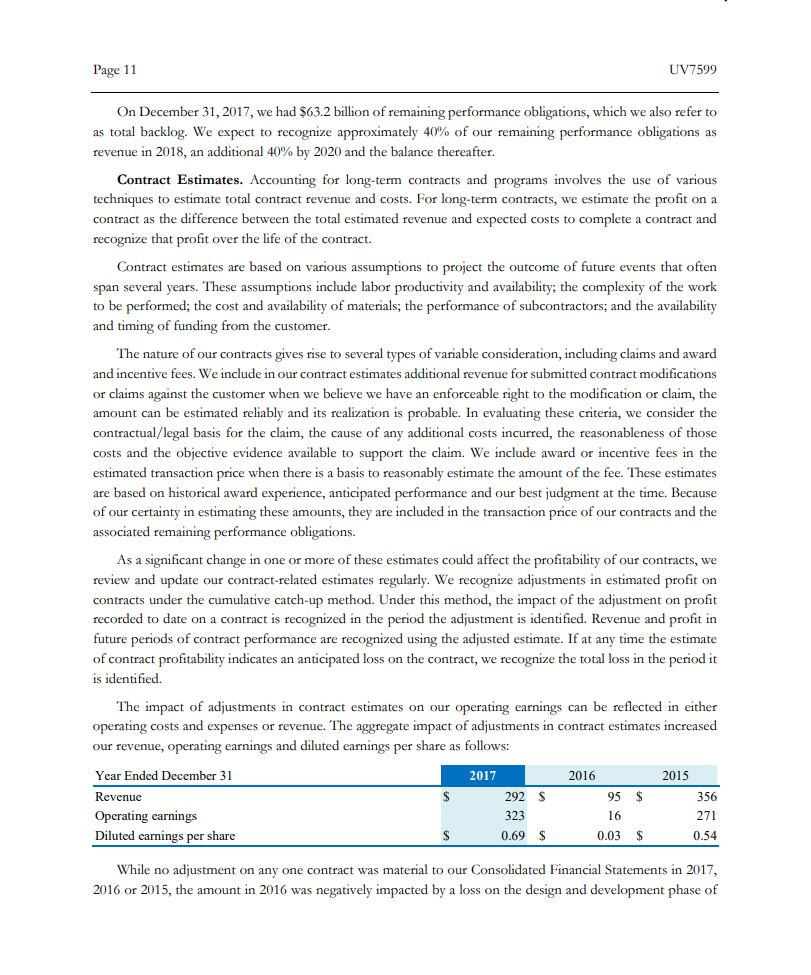

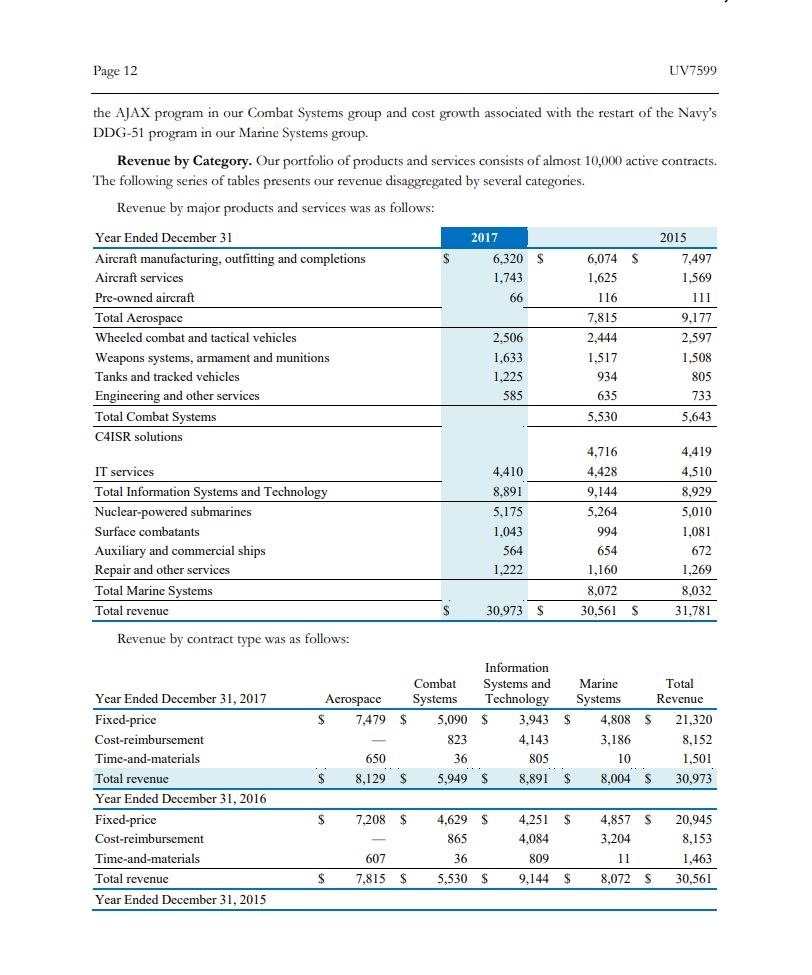

Page 11 UV7599 On December 31, 2017, we had $63.2 billion of remaining performance obligations, which we also refer to as total backlog. We expect to recognize approximately 40% of our remaining performance obligations as revenue in 2018, an additional 40% by 2020 and the balance thereafter. Contract Estimates. Accounting for long-term contracts and programs involves the use of various techniques to estimate total contract revenue and costs. For long-term contracts, we estimate the profit on a contract as the difference between the total estimated revenue and expected costs to complete a contract and recognize that profit over the life of the contract. Contract estimates are based on various assumptions to project the outcome of future events that often span several years. These assumptions include labor productivity and availability, the complexity of the work to be performed; the cost and availability of materials; the performance of subcontractors; and the availability and timing of funding from the customer. The nature of our contracts gives rise to several types of variable consideration, including claims and award and incentive fees. We include in our contract estimates additional revenue for submitted contract modifications or claims against the customer when we believe we have an enforceable right to the modification or claim, the amount can be estimated reliably and its realization is probable. In evaluating these criteria, we consider the contractual/legal basis for the claim, the cause of any additional costs incurred, the reasonableness of those costs and the objective evidence available to support the claim. We include award or incentive fees in the estimated transaction price when there is a basis to reasonably estimate the amount of the fee. These estimates are based on historical award experience, anticipated performance and our best judgment at the time. Because of our certainty in estimating these amounts, they are included in the transaction price of our contracts and the associated remaining performance obligations. As a significant change in one or more of these estimates could affect the profitability of our contracts, we review and update our contract-related estimates regularly. We recognize adjustments in estimated profit on contracts under the cumulative catch-up method. Under this method, the impact of the adjustment on profit recorded to date on a contract is recognized in the period the adjustment is identified. Revenue and profit in future periods of contract performance are recognized using the adjusted estimate. If at any time the estimate of contract profitability indicates an anticipated loss on the contract, we recognize the total loss in the period it is identified. The impact of adjustments in contract estimates on our operating earnings can be reflected in either operating costs and expenses or revenue. The aggregate impact of adjustments in contract estimates increased our revenue, operating earnings and diluted earnings per share as follows: Year Ended December 31 2017 2016 2015 Revenue 292 $ 95 $ 356 Operating earnings 323 16 271 Diluted earnings per share 0.69 $ 0.03 $ 0.54 $ While no adjustment on any one contract was material to our Consolidated Financial Statements in 2017, 2016 or 2015, the amount in 2016 was negatively impacted by a loss on the design and development phase of Page 12 UV7599 66 111 the AJAX program in our Combat Systems group and cost growth associated with the restart of the Navy's DDG-51 program in our Marine Systems group. Revenue by Category. Our portfolio of products and services consists of almost 10,000 active contracts The following series of tables presents our revenue disaggregated by several categories. Revenue by major products and services was as follows: Year Ended December 31 2017 2015 Aircraft manufacturing, outfitting and completions $ 6,320 $ 6,074 S 7,497 Aircraft services 1,743 1,625 1.569 Pre-owned aircraft 116 Total Aerospace 7,815 9,177 Wheeled combat and tactical vehicles 2,506 2,444 2,597 Weapons systems, armament and munitions 1.633 1,517 1,508 Tanks and tracked vehicles 1,225 805 Engineering and other services 635 733 Total Combat Systems 5,530 5,643 C4ISR solutions 4,716 4,419 IT services 4.410 4,428 4,510 Total Information Systems and Technology 8.891 9,144 8,929 Nuclear-powered submarines 5.175 5,264 5,010 Surface combatants 1,043 994 1,081 Auxiliary and commercial ships 564 654 672 Repair and other services 1,222 1,160 1,269 Total Marine Systems 8,072 8,032 Total revenue $ 30,973 $ 30,561 $ 31,781 Revenue by contract type was as follows: 934 585 Aerospace $ 7,479 $ Combat Systems 5,090 823 36 5,949 Information Systems and Marine Technology Systems $ 3,943 $ 4,808 4,143 3,186 805 10 $ 8,891 $ 8,004 $ Total Revenue 21,320 8,152 1,501 30,973 650 8,129 $ $ $ Year Ended December 31, 2017 Fixed-price Cost-reimbursement Time-and-materials Total revenue Year Ended December 31, 2016 Fixed-price Cost-reimbursement Time-and-materials Total revenue Year Ended December 31, 2015 $ 7,208 $ $ 4,629 865 4.251 $ 4,084 809 9,144 $ 4,857 $ 3,204 11 8,072 $ 20,945 8,153 1,463 30,561 36 607 7,815 $ $ 5,530 $ Page 11 UV7599 On December 31, 2017, we had $63.2 billion of remaining performance obligations, which we also refer to as total backlog. We expect to recognize approximately 40% of our remaining performance obligations as revenue in 2018, an additional 40% by 2020 and the balance thereafter. Contract Estimates. Accounting for long-term contracts and programs involves the use of various techniques to estimate total contract revenue and costs. For long-term contracts, we estimate the profit on a contract as the difference between the total estimated revenue and expected costs to complete a contract and recognize that profit over the life of the contract. Contract estimates are based on various assumptions to project the outcome of future events that often span several years. These assumptions include labor productivity and availability, the complexity of the work to be performed; the cost and availability of materials; the performance of subcontractors; and the availability and timing of funding from the customer. The nature of our contracts gives rise to several types of variable consideration, including claims and award and incentive fees. We include in our contract estimates additional revenue for submitted contract modifications or claims against the customer when we believe we have an enforceable right to the modification or claim, the amount can be estimated reliably and its realization is probable. In evaluating these criteria, we consider the contractual/legal basis for the claim, the cause of any additional costs incurred, the reasonableness of those costs and the objective evidence available to support the claim. We include award or incentive fees in the estimated transaction price when there is a basis to reasonably estimate the amount of the fee. These estimates are based on historical award experience, anticipated performance and our best judgment at the time. Because of our certainty in estimating these amounts, they are included in the transaction price of our contracts and the associated remaining performance obligations. As a significant change in one or more of these estimates could affect the profitability of our contracts, we review and update our contract-related estimates regularly. We recognize adjustments in estimated profit on contracts under the cumulative catch-up method. Under this method, the impact of the adjustment on profit recorded to date on a contract is recognized in the period the adjustment is identified. Revenue and profit in future periods of contract performance are recognized using the adjusted estimate. If at any time the estimate of contract profitability indicates an anticipated loss on the contract, we recognize the total loss in the period it is identified. The impact of adjustments in contract estimates on our operating earnings can be reflected in either operating costs and expenses or revenue. The aggregate impact of adjustments in contract estimates increased our revenue, operating earnings and diluted earnings per share as follows: Year Ended December 31 2017 2016 2015 Revenue 292 $ 95 $ 356 Operating earnings 323 16 271 Diluted earnings per share 0.69 $ 0.03 $ 0.54 $ While no adjustment on any one contract was material to our Consolidated Financial Statements in 2017, 2016 or 2015, the amount in 2016 was negatively impacted by a loss on the design and development phase of Page 12 UV7599 66 111 the AJAX program in our Combat Systems group and cost growth associated with the restart of the Navy's DDG-51 program in our Marine Systems group. Revenue by Category. Our portfolio of products and services consists of almost 10,000 active contracts The following series of tables presents our revenue disaggregated by several categories. Revenue by major products and services was as follows: Year Ended December 31 2017 2015 Aircraft manufacturing, outfitting and completions $ 6,320 $ 6,074 S 7,497 Aircraft services 1,743 1,625 1.569 Pre-owned aircraft 116 Total Aerospace 7,815 9,177 Wheeled combat and tactical vehicles 2,506 2,444 2,597 Weapons systems, armament and munitions 1.633 1,517 1,508 Tanks and tracked vehicles 1,225 805 Engineering and other services 635 733 Total Combat Systems 5,530 5,643 C4ISR solutions 4,716 4,419 IT services 4.410 4,428 4,510 Total Information Systems and Technology 8.891 9,144 8,929 Nuclear-powered submarines 5.175 5,264 5,010 Surface combatants 1,043 994 1,081 Auxiliary and commercial ships 564 654 672 Repair and other services 1,222 1,160 1,269 Total Marine Systems 8,072 8,032 Total revenue $ 30,973 $ 30,561 $ 31,781 Revenue by contract type was as follows: 934 585 Aerospace $ 7,479 $ Combat Systems 5,090 823 36 5,949 Information Systems and Marine Technology Systems $ 3,943 $ 4,808 4,143 3,186 805 10 $ 8,891 $ 8,004 $ Total Revenue 21,320 8,152 1,501 30,973 650 8,129 $ $ $ Year Ended December 31, 2017 Fixed-price Cost-reimbursement Time-and-materials Total revenue Year Ended December 31, 2016 Fixed-price Cost-reimbursement Time-and-materials Total revenue Year Ended December 31, 2015 $ 7,208 $ $ 4,629 865 4.251 $ 4,084 809 9,144 $ 4,857 $ 3,204 11 8,072 $ 20,945 8,153 1,463 30,561 36 607 7,815 $ $ 5,530 $