Answered step by step

Verified Expert Solution

Question

1 Approved Answer

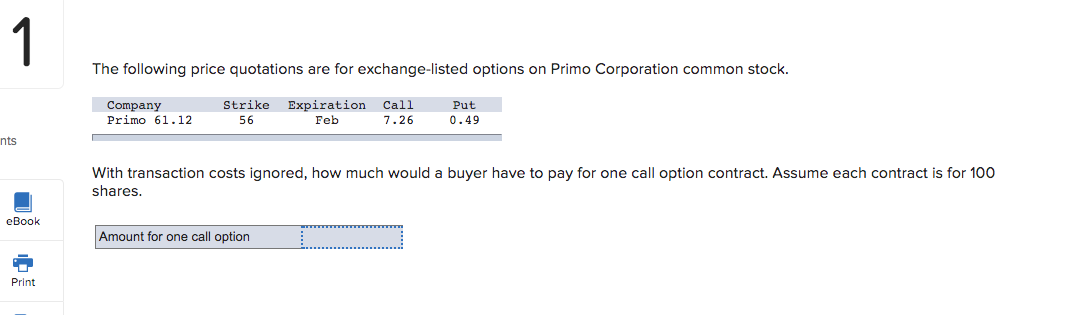

1 The following price quotations are for exchange-listed options on Primo Corporation common stock. Company Primo 61.12 Strike 56 Expiration Feb Call 7.26 Put 0.49

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Information Systems Control And Audit

Authors: Et Al. Hyo-Jeong Kim, Michael Mannino, Compiled By Koros Press Editorial Board

1st Edition