Answered step by step

Verified Expert Solution

Question

1 Approved Answer

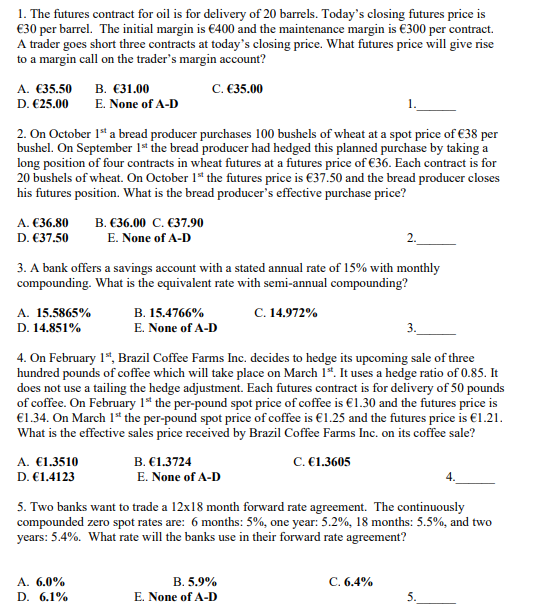

1. The futures contract for oil is for delivery of 20 barrels. Today's closing futures price is 30 per barrel. The initial margin is 400

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Sustainability In Public Administration Exploring The Concept Of Financial Health

Authors: Manuel Pedro Rodríguez Bolívar

1st Edition

3319579614, 3319579622, 9783319579610, 9783319579627