Answered step by step

Verified Expert Solution

Question

1 Approved Answer

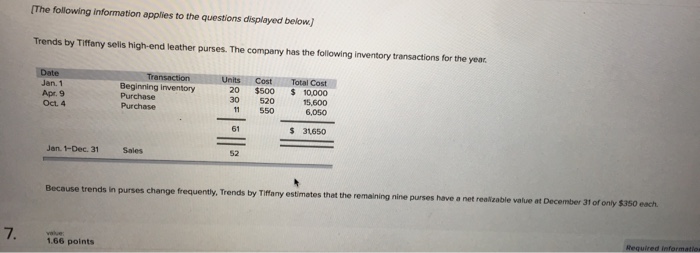

1. Using FIFO, calculate ending inventory and cost of goods sold. 2. Using LIFO, calculate ending inventory and cost of goods sold. 3-a. Determine the

1. Using FIFO, calculate ending inventory and cost of goods sold.

2. Using LIFO, calculate ending inventory and cost of goods sold.

3-a. Determine the amount of ending inventory to report using lower of cost and net realizable value.

3-b. Record any necessary adjustment under (a) FIFO. (If no entry is required for a transaction/event, select "No journal entry required" in the first account field.)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

A Guide To Auditing Programmes And Projects

Authors: Andrew Schuster, APM Assurance SIG

1st Edition

191330521X, 978-1913305215