Question: 1. Using the 2019 financial statement information for Ford combined with the Valueline survery, score Ford based on the 10 original screening criteria. (Make a

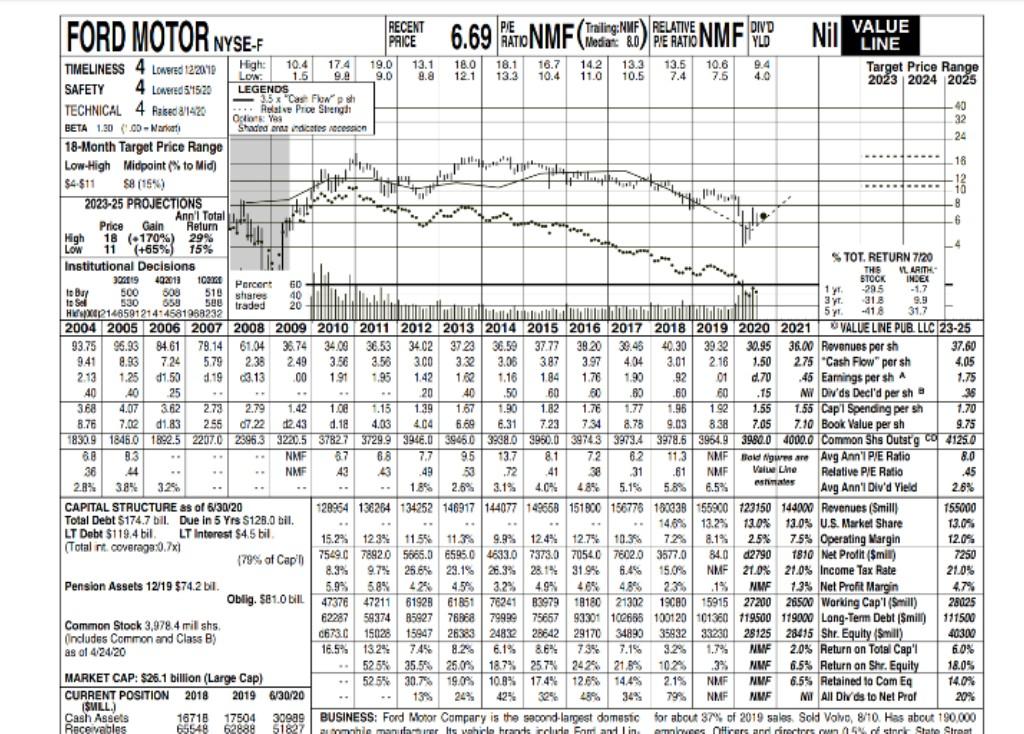

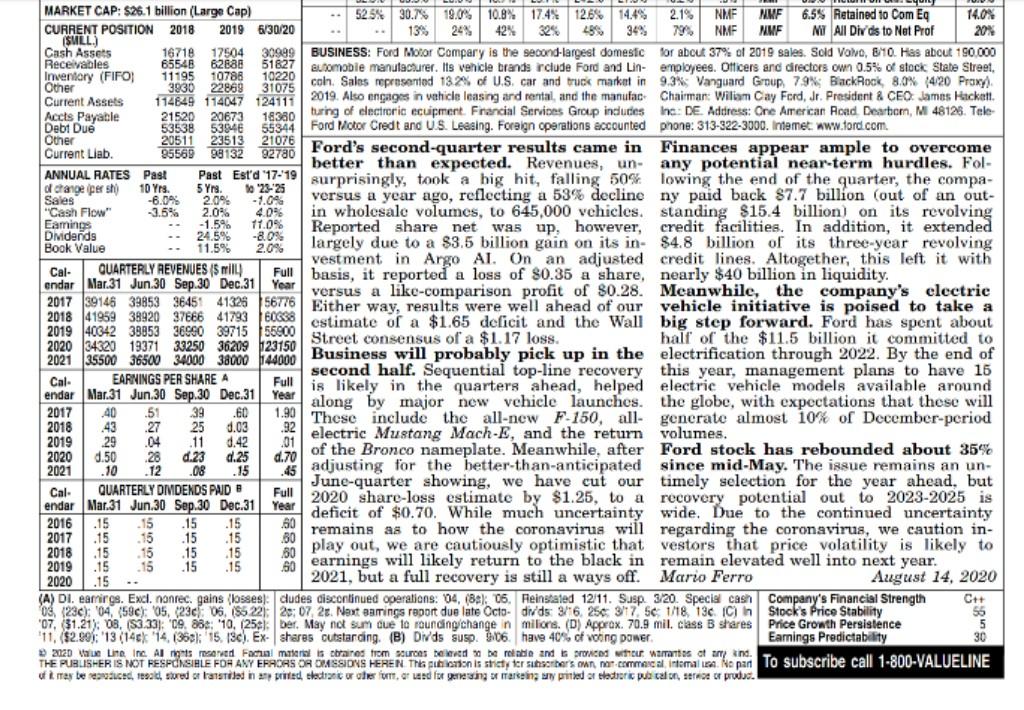

1. Using the 2019 financial statement information for Ford combined with the Valueline survery, score Ford based on the 10 original screening criteria. (Make a spreadsheet) 2. Would Ford make it to the second round? Why or why not? 3. Now assume Ford passes the initial round. Would it be considered a buy after going through the second round? Why or why not? 4. What was the criteria for the Rea-Graham fund? 5. Now look at Ford based on the new reduced criteria. Would Ford be included as a candidate for investment? Why or why not? FORD MOTOR NYSE- 6.69 RONMF (Tedene ) PELANNE NMF VND Nil VALUE High: . to Sol RECENT PE Trailing:NMF RELATIVE DIVD F PRICE LINE TIMELINESS 4 Lowered 12:20:19 10.4 17.4 19.0 13.1 18.0 18.1 16.7 14.2 13.3 13.5 10.6 9.4 Target Price Range LON 1.5 9.0 8.a 12.1 13.3 10.4 11.0 10.5 7.4 7.5 4.0 SAFETY 4 Lowered 541520 LEGENDS 2023 2024 2025 35 Cas Flowpoh TECHNICAL 4 Rased 3/1470 - Relate Pro Strengh 40 Ocore Ya 32 BETA 130.00- Narice Shaded on indicates con 18-Month Target Price Range 24 Low-High Midpoint (% to Mid 18 $4.$11 $8 (154) INT 12 10 2023-25 PROJECTIONS 8 Ann' Total Price Gain Return 6 High 18 (170%) 29% Low 11 (+65%) 15% 4 Institutional Decisions STOT. RETURN 7/20 THE 392019 VLAAITH 402011 100m Poreert 60 STOCK INDEX to Buy 500 809 518 -29.5 40 -1.7 shares 530 650 sel traded 20 3 y. 318 9.9 HX2148591214:4581988232 5 y 31.7 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 VALUELNE PUB LLC 23-25 93.75 96.93 84.61 78.14 61.04 3574 34.00 36.53 3402 37 23 36.50 37.77 3920 36.45 40.30 3932 30.95 36.00 Revenues per sh 37.60 9.41 8.93 724 5.79 2.38 2.49 3.58 3.56 3.00 3.32 3.06 3.87 3.97 4.04 3.01 2.16 1.50 275 Cash Flow" per sh 4,05 2.13 1.25 d1.50 1.19 63.13 00 1.91 1.42 12 1.16 184 1.78 199 92 01 0.70 .45 Earnings per sh 1.75 40 40 25 ** 20 40 .50 60 60 89 60 60 .15 W DIVds Decld per she 36 3.68 4.07 3.62 2.73 2.79 1.42 1.08 1.15 139 1.67 1.90 1.82 1.78 1.77 1.96 1.92 1.55 1.55 Cap'l Spending per sh 1.70 8.78 7.02 d1.83 2.55 07.22 12.43 d. 18 4.03 4.04 6.69 6.31 7.23 7.34 8.78 0.16 9.03 838 7.05 7.10 Book Value per sh 9.75 18329 1846.0 18.2.5 2207.0 23963 3220.5 37827 3729.9 3948.0 39450 3:28.0 3950.0 39743 3973.4 378.6 3954.9 3980.0 4000.0 Common Shs Outstg Co4125.0 68 8.3 NMF 3.7 68 7.7 95 13.7 81 81 72 8.2 113 NMF Bold Ngwear Avg Ann'i P/E Ratio 8.0 36 44 NME 42 .49 53 .72 41 31 .61 NMF Value Line Relative P/E Ratio 45 28% 38% 3.25 1.8% 2.6% 3.1% 4.0% 48% 5.1% 5.8% 6.5% estimates Avg Ann'i Div'd Yield 2.6% CAPITAL STRUCTURE 83 of 6/30/20 120954 138264 134252 146917 144077 149658 151800 156776 180238155900 123150 144000 Revenues (Smill) 155000 Total Debt $174.7 bil. Due in 5 Yrs $128.0 bil. 14.6% 13.2% 13.0% 13.0% U.S. Market Share 13.0% LT Debt $119.4 bil. LT Interest $4.5 bil 15.2% 123% 11.56 11.39% 9.9% 12,4% 12.75 10.39 7.2% 8.1% (Total nt coverage:0.7x1 2.5% 7.5% Operating Margin 12.0% 179% of Cap 7529.0 78920 5665.0 6595.0 4633.0 7373.0 70540 7602. 3577.0 84.0 02790 1810 Net Profit (Smil) 7250 97% . 25.6% 23.1% 26.3% 28.1 31.9% 6.4% 15.0% NMF 21.0% 21.0% Income Tax Rate 21.0% Pension Assets 12/19 $74.2 bil. 5.9% 5.8% 3.04 42% 4.5% 450 3.2% 9.30 4.9% 46% SON 234 .1% NWF SD 19 1.3% Net Profit Margin Oblig. 581.0 L 47376 47% 47211 61928 61851 76241 83979 19CAO 1818021302 D 15915 w 27200 26500 Working Cap' (Smil) 28125 62287 Common Stock 3,978.4 mil shs 59374 85927 78BE8 79999 75667 93301 102685 100120101360 119500 119000 Long-Term Debt (Smil) 111500 C673 end (Includes Common and Class B) 15028 15947 26383 24832 28642 2917034893 3583233230 wa 28125 28415 Shr. Equity (Smil) 40300 as of 42420 16.5% 1324 8.25 6.1% 8.6% 73% 3.29 1.7% NMF 2.0% Return on Total Cap'l 6.0% 525% 35,5% 25.0% 18.7% 257% 242% 21,8% 1024 3% NIMF 6.5% Return on Shr. Equity 18.0% MARKET CAP: $26.1 billion (Large Cap) $ 525% 30.7% 19.0% 10.8% 17.4% 12.6% 14.4% 2.1% NMF NUF 6.5% Retained la Cam Eq 14.0% CURRENT POSITION 2018 2019 6/30/20 13 24% 42% 324 34% NMF NMF MI All Dds to Net Prof SULL) 20% Cash Assets 16718 17504 30.ag BUSINESS: Ford Motor Compary is the second-largest domestc for about 37% of 2019 sales Sold Volvo, 810. Has about 190.000 Receivables 65548 62888 51827 mshie manner wohirio franciscus Sami and in les Hirers and directors own of ster State Strost Sales hon . big step Full basis, it reported a loss of 30.35 a share, credit $40 bin together, this left it with versus a like-comparison profit of 80.28. Meanwhile, the companys electrie Year" likely in the MARKET CAP: $26.1 billion (Large Cap) 52.5% 30.7% 19.0% 10.8% 17.48 12.614.4% 2.1% NME NMF 6.5S Retained to Com Eq 14.0% CURRENT POSITION 2018 2019 6/30/20 139 24% 42% 394 299 349, NMF NMF MI All Divds to Net Prof 20% (SULL.) Cash Assets 16718 17504 30999 BUSINESS: Ford Motor Compary is the second-largest domesic for about 37% of 2019 sales. Sold Volvo, 810. Has about 190.000 Receivables 65546 62888 51827 automoble manutacturer. Its vehicle brands rclude Ford and Lin- employees. Officers and directors own 0.5% of stock State Street, Inventory (FIFO) 11195 10788 10220 Other 3930 22869 31075 coln Sales represented 13.2% of U.S. car and truck market in 9.3% Vanguard Group 79%; BackRock, 8.0% 420 Proxy) Current Assets 114849 114047 124111 2019. Also engages in vehicle leasing and rental, and the manufac Chairman: William Cay Ford, Jr. President & CEO James Hackett Accts Payable 21520 20673 18380 turing of electronic ecuipment. Francial Services Group indudes Inc. DE. Address: One American Road Dearborn, M 48126. Tele Debt Due 53538 5394 55344 Ford Motor Credt and U.S. Leasing. Foreign operations accounted phone: 313-322-3000. Intemet www.tord.com Other 20511 23513 21076 Current Liab 95569 98132 92780 Ford's second-quarter results came in Finances appear ample to overcome better than expected. Revenues, un any potential near-term hurdles. Fol- ANNUAL RATES Past Past Estd 17-19 al change persht 10 Yrs. 5 Yrs to 23-25 surprisingly, took a big hit, falling 50% lowing the end of the quarter, the compa- -6.0% 20% -1.0% versus a year ago, reflecting a 53% decline ny paid back $7.7 billion (out of an out- "Cash Flow" 3.5% 2.0% 4.0% in wholesale volumes, to 645,000 vehicles. on its revolving Earings -1.5% 11.0% Didends 24.5% -8.0% its in- $4.8 billion Book Value largely due to a $3.5 billion gain on 11.5% 2.0% of its three-year revolving . Cal- QUARTERLY REVENUES(5 mill endar Mar 31 Jun 30 Sep.30 Dec.31 Year 2018 41959 38920 37686 41793 BOGS estimate of a $1.65 deficit and the Wall to a 2019 40842 38953 36000 39715 55200 Street consensus of a $1.17 loss. forward. Ford has spent about hair of the $11.5 billion it committed to 2021 35500 36500 34000 38000 144000 to Cal. A lis endar Mar 31 Jun 30 Sep.30 Dec.31 18 quarters ahead, helped electric vehicle models available around by major new vehicle launches the globe, with expectations that these will 2017 ,40 .51 39 .60 1.90 These -F, all- 2018 43 .27 25 0.03 29 .04 .11 volumes. d.42 2.0 of the Bronco nameplate. Meanwhile, after Ford stock has rebounded about 35% 2020 0.50 d.23 d.25 2021 10 .12 .08 .15 1.4. adjusting for the better than-anticipated since mid-May. The issue remains an un- Cal. QUARTERLY DMDENDS PAID share-loss by $1. endar Mar 31 Jun 30 Sep.30 Dec.31 Year to a deficit of $0.70. While much uncertainty wide. Due to the continued uncertainty recovery potential out to 2023-2025 is 2016 .15 .15 .15 .15 2017 .15 15 15 80 remains as to how the coronavirus will regarding the coronavirus, we caution in- .15 2018 15 15 15 .15 80 play out, we are cautiously optimistic that vestors that price volatility is likely to 2019 .15 15 .15 .15 60 earnings will likely return to the black in remain elevated well into next year. 2020 .15 2021, but a full recovery is still a ways off. Mario Ferro August 14, 2020 (A) DI. earings. Excl. nonrec. gains (losses: dudes discontinued operations: 04, (8), 06. Reinstated 12/11. Susp. 3/20. Special cash Company's Financial Strength CH 08, 1230): 104, (590) 05, 230 06. (85221 20:07 2. Next eamings raport due late Octo- dids: 3/16 256 317 5 1/18, 130 C) in Stock's Price Stability 55 '07, 31.21): 08. (83.33): 09. 28: 10. (25): Der. May not sum due to rounding change in milions. (D) Approx. 70.9 mil. class B shares Price Growth Persistence 11. $2.99: 13 (146k 14. (362: 15.13). Ex- shares outstarding. (B) Dids susp. 9:06. have 40% of voong power Earnings Predictability 30 2020 Van Line, Inc. All roved Facial materslis ebraines from sources Dedo berele and proced with warranties of any kind. THE PUBLISHER IS NOT RESPONSIALE FOR ANY EFRORS OR OMISSIONS HEREN Thion is strict ter sisters own, nor commacul Tintoma in "Me par To subscribe call 1-800-VALUELINE of a berec, 189, stored or raid in an inte ta urte, or weed for genesing or arsein wy printed or sledic pub calon, Stor produce 2012 septes 2300 Business will probably pick up in the electrification through 2022. By the end of EARNINGS PER SHARE 2019 5 1. Using the 2019 financial statement information for Ford combined with the Valueline survery, score Ford based on the 10 original screening criteria. (Make a spreadsheet) 2. Would Ford make it to the second round? Why or why not? 3. Now assume Ford passes the initial round. Would it be considered a buy after going through the second round? Why or why not? 4. What was the criteria for the Rea-Graham fund? 5. Now look at Ford based on the new reduced criteria. Would Ford be included as a candidate for investment? Why or why not? FORD MOTOR NYSE- 6.69 RONMF (Tedene ) PELANNE NMF VND Nil VALUE High: . to Sol RECENT PE Trailing:NMF RELATIVE DIVD F PRICE LINE TIMELINESS 4 Lowered 12:20:19 10.4 17.4 19.0 13.1 18.0 18.1 16.7 14.2 13.3 13.5 10.6 9.4 Target Price Range LON 1.5 9.0 8.a 12.1 13.3 10.4 11.0 10.5 7.4 7.5 4.0 SAFETY 4 Lowered 541520 LEGENDS 2023 2024 2025 35 Cas Flowpoh TECHNICAL 4 Rased 3/1470 - Relate Pro Strengh 40 Ocore Ya 32 BETA 130.00- Narice Shaded on indicates con 18-Month Target Price Range 24 Low-High Midpoint (% to Mid 18 $4.$11 $8 (154) INT 12 10 2023-25 PROJECTIONS 8 Ann' Total Price Gain Return 6 High 18 (170%) 29% Low 11 (+65%) 15% 4 Institutional Decisions STOT. RETURN 7/20 THE 392019 VLAAITH 402011 100m Poreert 60 STOCK INDEX to Buy 500 809 518 -29.5 40 -1.7 shares 530 650 sel traded 20 3 y. 318 9.9 HX2148591214:4581988232 5 y 31.7 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 VALUELNE PUB LLC 23-25 93.75 96.93 84.61 78.14 61.04 3574 34.00 36.53 3402 37 23 36.50 37.77 3920 36.45 40.30 3932 30.95 36.00 Revenues per sh 37.60 9.41 8.93 724 5.79 2.38 2.49 3.58 3.56 3.00 3.32 3.06 3.87 3.97 4.04 3.01 2.16 1.50 275 Cash Flow" per sh 4,05 2.13 1.25 d1.50 1.19 63.13 00 1.91 1.42 12 1.16 184 1.78 199 92 01 0.70 .45 Earnings per sh 1.75 40 40 25 ** 20 40 .50 60 60 89 60 60 .15 W DIVds Decld per she 36 3.68 4.07 3.62 2.73 2.79 1.42 1.08 1.15 139 1.67 1.90 1.82 1.78 1.77 1.96 1.92 1.55 1.55 Cap'l Spending per sh 1.70 8.78 7.02 d1.83 2.55 07.22 12.43 d. 18 4.03 4.04 6.69 6.31 7.23 7.34 8.78 0.16 9.03 838 7.05 7.10 Book Value per sh 9.75 18329 1846.0 18.2.5 2207.0 23963 3220.5 37827 3729.9 3948.0 39450 3:28.0 3950.0 39743 3973.4 378.6 3954.9 3980.0 4000.0 Common Shs Outstg Co4125.0 68 8.3 NMF 3.7 68 7.7 95 13.7 81 81 72 8.2 113 NMF Bold Ngwear Avg Ann'i P/E Ratio 8.0 36 44 NME 42 .49 53 .72 41 31 .61 NMF Value Line Relative P/E Ratio 45 28% 38% 3.25 1.8% 2.6% 3.1% 4.0% 48% 5.1% 5.8% 6.5% estimates Avg Ann'i Div'd Yield 2.6% CAPITAL STRUCTURE 83 of 6/30/20 120954 138264 134252 146917 144077 149658 151800 156776 180238155900 123150 144000 Revenues (Smill) 155000 Total Debt $174.7 bil. Due in 5 Yrs $128.0 bil. 14.6% 13.2% 13.0% 13.0% U.S. Market Share 13.0% LT Debt $119.4 bil. LT Interest $4.5 bil 15.2% 123% 11.56 11.39% 9.9% 12,4% 12.75 10.39 7.2% 8.1% (Total nt coverage:0.7x1 2.5% 7.5% Operating Margin 12.0% 179% of Cap 7529.0 78920 5665.0 6595.0 4633.0 7373.0 70540 7602. 3577.0 84.0 02790 1810 Net Profit (Smil) 7250 97% . 25.6% 23.1% 26.3% 28.1 31.9% 6.4% 15.0% NMF 21.0% 21.0% Income Tax Rate 21.0% Pension Assets 12/19 $74.2 bil. 5.9% 5.8% 3.04 42% 4.5% 450 3.2% 9.30 4.9% 46% SON 234 .1% NWF SD 19 1.3% Net Profit Margin Oblig. 581.0 L 47376 47% 47211 61928 61851 76241 83979 19CAO 1818021302 D 15915 w 27200 26500 Working Cap' (Smil) 28125 62287 Common Stock 3,978.4 mil shs 59374 85927 78BE8 79999 75667 93301 102685 100120101360 119500 119000 Long-Term Debt (Smil) 111500 C673 end (Includes Common and Class B) 15028 15947 26383 24832 28642 2917034893 3583233230 wa 28125 28415 Shr. Equity (Smil) 40300 as of 42420 16.5% 1324 8.25 6.1% 8.6% 73% 3.29 1.7% NMF 2.0% Return on Total Cap'l 6.0% 525% 35,5% 25.0% 18.7% 257% 242% 21,8% 1024 3% NIMF 6.5% Return on Shr. Equity 18.0% MARKET CAP: $26.1 billion (Large Cap) $ 525% 30.7% 19.0% 10.8% 17.4% 12.6% 14.4% 2.1% NMF NUF 6.5% Retained la Cam Eq 14.0% CURRENT POSITION 2018 2019 6/30/20 13 24% 42% 324 34% NMF NMF MI All Dds to Net Prof SULL) 20% Cash Assets 16718 17504 30.ag BUSINESS: Ford Motor Compary is the second-largest domestc for about 37% of 2019 sales Sold Volvo, 810. Has about 190.000 Receivables 65548 62888 51827 mshie manner wohirio franciscus Sami and in les Hirers and directors own of ster State Strost Sales hon . big step Full basis, it reported a loss of 30.35 a share, credit $40 bin together, this left it with versus a like-comparison profit of 80.28. Meanwhile, the companys electrie Year" likely in the MARKET CAP: $26.1 billion (Large Cap) 52.5% 30.7% 19.0% 10.8% 17.48 12.614.4% 2.1% NME NMF 6.5S Retained to Com Eq 14.0% CURRENT POSITION 2018 2019 6/30/20 139 24% 42% 394 299 349, NMF NMF MI All Divds to Net Prof 20% (SULL.) Cash Assets 16718 17504 30999 BUSINESS: Ford Motor Compary is the second-largest domesic for about 37% of 2019 sales. Sold Volvo, 810. Has about 190.000 Receivables 65546 62888 51827 automoble manutacturer. Its vehicle brands rclude Ford and Lin- employees. Officers and directors own 0.5% of stock State Street, Inventory (FIFO) 11195 10788 10220 Other 3930 22869 31075 coln Sales represented 13.2% of U.S. car and truck market in 9.3% Vanguard Group 79%; BackRock, 8.0% 420 Proxy) Current Assets 114849 114047 124111 2019. Also engages in vehicle leasing and rental, and the manufac Chairman: William Cay Ford, Jr. President & CEO James Hackett Accts Payable 21520 20673 18380 turing of electronic ecuipment. Francial Services Group indudes Inc. DE. Address: One American Road Dearborn, M 48126. Tele Debt Due 53538 5394 55344 Ford Motor Credt and U.S. Leasing. Foreign operations accounted phone: 313-322-3000. Intemet www.tord.com Other 20511 23513 21076 Current Liab 95569 98132 92780 Ford's second-quarter results came in Finances appear ample to overcome better than expected. Revenues, un any potential near-term hurdles. Fol- ANNUAL RATES Past Past Estd 17-19 al change persht 10 Yrs. 5 Yrs to 23-25 surprisingly, took a big hit, falling 50% lowing the end of the quarter, the compa- -6.0% 20% -1.0% versus a year ago, reflecting a 53% decline ny paid back $7.7 billion (out of an out- "Cash Flow" 3.5% 2.0% 4.0% in wholesale volumes, to 645,000 vehicles. on its revolving Earings -1.5% 11.0% Didends 24.5% -8.0% its in- $4.8 billion Book Value largely due to a $3.5 billion gain on 11.5% 2.0% of its three-year revolving . Cal- QUARTERLY REVENUES(5 mill endar Mar 31 Jun 30 Sep.30 Dec.31 Year 2018 41959 38920 37686 41793 BOGS estimate of a $1.65 deficit and the Wall to a 2019 40842 38953 36000 39715 55200 Street consensus of a $1.17 loss. forward. Ford has spent about hair of the $11.5 billion it committed to 2021 35500 36500 34000 38000 144000 to Cal. A lis endar Mar 31 Jun 30 Sep.30 Dec.31 18 quarters ahead, helped electric vehicle models available around by major new vehicle launches the globe, with expectations that these will 2017 ,40 .51 39 .60 1.90 These -F, all- 2018 43 .27 25 0.03 29 .04 .11 volumes. d.42 2.0 of the Bronco nameplate. Meanwhile, after Ford stock has rebounded about 35% 2020 0.50 d.23 d.25 2021 10 .12 .08 .15 1.4. adjusting for the better than-anticipated since mid-May. The issue remains an un- Cal. QUARTERLY DMDENDS PAID share-loss by $1. endar Mar 31 Jun 30 Sep.30 Dec.31 Year to a deficit of $0.70. While much uncertainty wide. Due to the continued uncertainty recovery potential out to 2023-2025 is 2016 .15 .15 .15 .15 2017 .15 15 15 80 remains as to how the coronavirus will regarding the coronavirus, we caution in- .15 2018 15 15 15 .15 80 play out, we are cautiously optimistic that vestors that price volatility is likely to 2019 .15 15 .15 .15 60 earnings will likely return to the black in remain elevated well into next year. 2020 .15 2021, but a full recovery is still a ways off. Mario Ferro August 14, 2020 (A) DI. earings. Excl. nonrec. gains (losses: dudes discontinued operations: 04, (8), 06. Reinstated 12/11. Susp. 3/20. Special cash Company's Financial Strength CH 08, 1230): 104, (590) 05, 230 06. (85221 20:07 2. Next eamings raport due late Octo- dids: 3/16 256 317 5 1/18, 130 C) in Stock's Price Stability 55 '07, 31.21): 08. (83.33): 09. 28: 10. (25): Der. May not sum due to rounding change in milions. (D) Approx. 70.9 mil. class B shares Price Growth Persistence 11. $2.99: 13 (146k 14. (362: 15.13). Ex- shares outstarding. (B) Dids susp. 9:06. have 40% of voong power Earnings Predictability 30 2020 Van Line, Inc. All roved Facial materslis ebraines from sources Dedo berele and proced with warranties of any kind. THE PUBLISHER IS NOT RESPONSIALE FOR ANY EFRORS OR OMISSIONS HEREN Thion is strict ter sisters own, nor commacul Tintoma in "Me par To subscribe call 1-800-VALUELINE of a berec, 189, stored or raid in an inte ta urte, or weed for genesing or arsein wy printed or sledic pub calon, Stor produce 2012 septes 2300 Business will probably pick up in the electrification through 2022. By the end of EARNINGS PER SHARE 2019 5

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts