Answered step by step

Verified Expert Solution

Question

1 Approved Answer

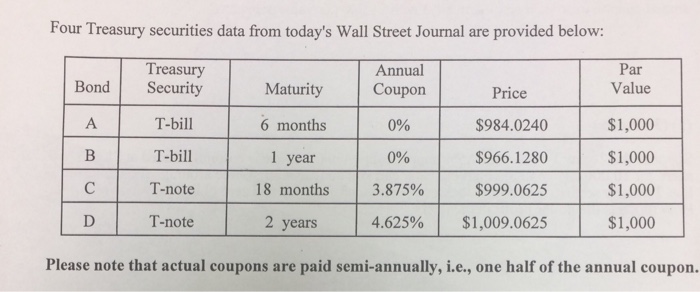

1. What are the zero prices for the 6-month, the 1-year, the 18-month, and the 2-year treasury securities above respectively? 2. What is the 6-month

1. What are the zero prices for the 6-month, the 1-year, the 18-month, and the 2-year treasury securities above respectively?

2. What is the 6-month forward rate beginning 1 year from today?

3. What is the 1 year forward rate beginning 6 months from today?

4. Given the zero prices obtained in (1) above. What should be the price of a 2-year T-note with 7.5% annual coupon (paid semiannually). With 1000 par value per share?

5. Suppose the 2 year T-note with 7.5% annual coupon in (4) above is currently traded at $1,010 per share for 10,000 shares in the market. How can you construct a risk-free arbitrage deal using all five treasury securities above to lock in a positive profit today and zero obligations in the future? How much is the dollar profit in the deal?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

A Blueprint For Lean Audit Lead Your Company To Higher Performance Levels

Authors: Maurice Washpun

1st Edition

B09R3DSLFF, 979-8408643707