Question

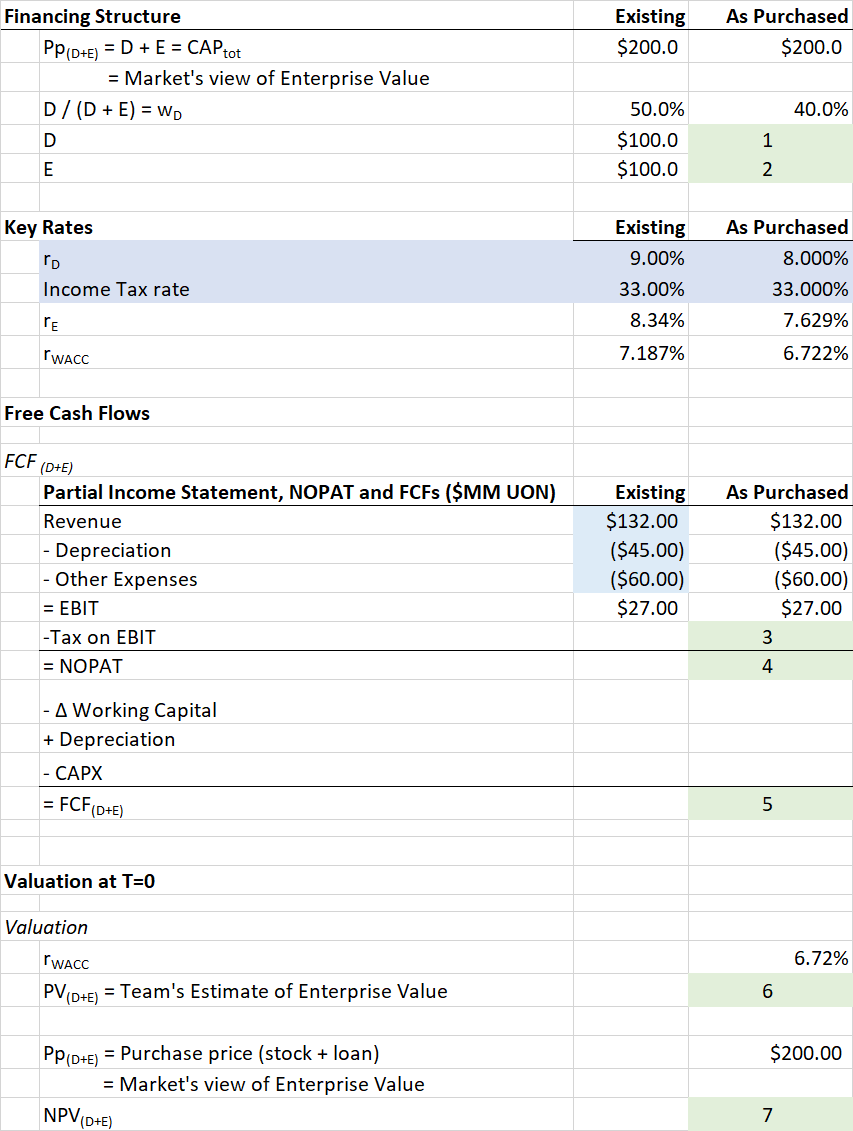

1. What is quantity 1 (shown in a green-background cell)? 2. What is quantity 2 (shown in a green-background cell)? 3. What is the absolute

1. What is quantity 1 (shown in a green-background cell)?

1. What is quantity 1 (shown in a green-background cell)?

2. What is quantity 2 (shown in a green-background cell)?

3. What is the absolute value of quantity 3 (shown in a green-background cell)?

4. What is quantity 4 (shown in a green-background cell)?

5. What is quantity 5 (shown in a green-background cell)?

6. What is quantity 6 (shown in a green-background cell)?

7. What is quantity 7 (shown in a green-background cell)?

8. Based on your answer for quantity 7, should the team consider going ahead with this project? Choose one answer and one reason.

Because the NPV > 0

Yes

No

Not enough information is provided to answer this question.

Because the team cannot make a final determination without analyzing out-of-model considerations.

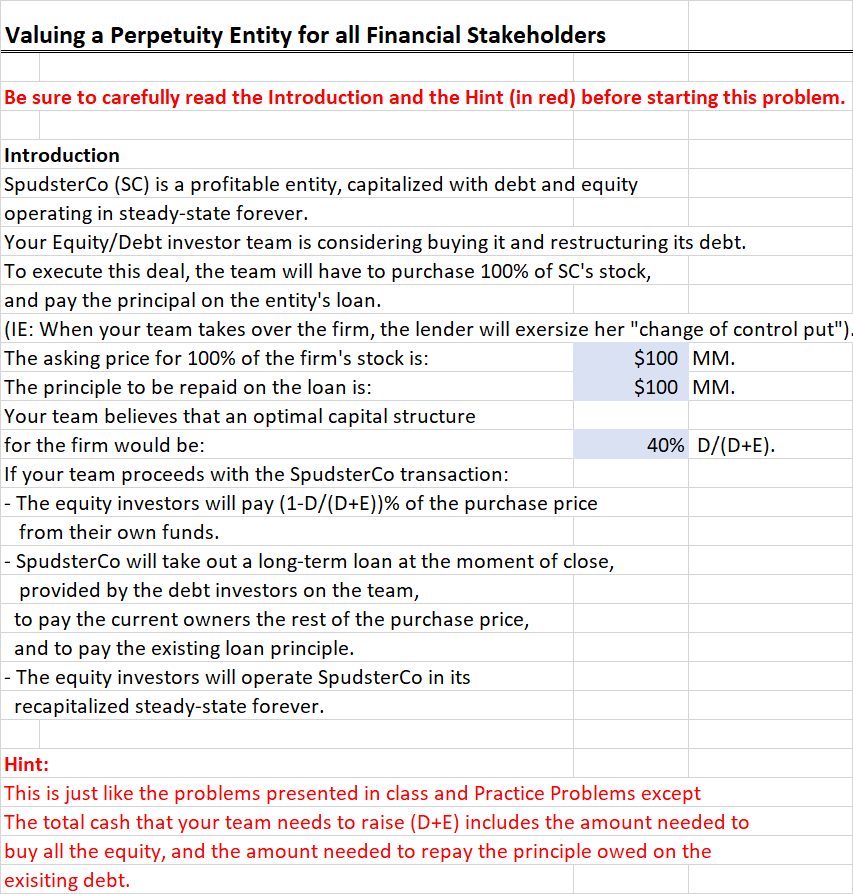

Because the NPV Valuing a Perpetuity Entity for all Financial Stakeholders Be sure to carefully read the Introduction and the Hint (in red) before starting this problem. Introduction SpudsterCo (SC) is a profitable entity, capitalized with debt and equity operating in steady-state forever. Your Equity/Debt investor team is considering buying it and restructuring its debt. To execute this deal, the team will have to purchase 100% of SC's stock, and pay the principal on the entity's loan. (IE: When your team takes over the firm, the lender will exersize her "change of control put"). The asking price for 100% of the firm's stock is: $100 MM. The principle to be repaid on the loan is: $100 MM. Your team believes that an optimal capital structure for the firm would be: 40% D/(D+E). If your team proceeds with the SpudsterCo transaction: - The equity investors will pay (1-D/(D+E))% of the purchase price from their own funds. - SpudsterCo will take out a long-term loan at the moment of close, provided by the debt investors on the team, to pay the current owners the rest of the purchase price, and to pay the existing loan principle. - The equity investors will operate SpudsterCo in its recapitalized steady-state forever. Hint: This is just like the problems presented in class and Practice Problems except The total cash that your team needs to raise (D+E) includes the amount needed to buy all the equity, and the amount needed to repay the principle owed on the exisiting debt. Existing $200.0 As Purchased $200.0 Financing Structure PP (D+E) = D + E = CAPtot = Market's view of Enterprise Value D/(D + E) = Wp D E 40.0% 50.0% $100.0 $100.0 1 2 Key Rates rp Income Tax rate Existing 9.00% 33.00% 8.34% As Purchased 8.000% 33.000% 7.629% 6.722% rwACC 7.187% Free Cash Flows FCF (D+E) Partial Income Statement, NOPAT and FCFS ($MM UON) Revenue - Depreciation - Other Expenses = EBIT -Tax on EBIT = NOPAT Existing $132.00 ($45.00) ($60.00) $27.00 As Purchased $132.00 ($45.00) ($60.00) $27.00 3 4 - A Working Capital + Depreciation - CAPX = FCF (D+E) 5 Valuation at T=0 Valuation 6.72% rwACC PV(D+E) = Team's Estimate of Enterprise Value 6 $200.00 PP (D+E) = Purchase price (stock + loan) = Market's view of Enterprise Value NPV (O+E) 7 Valuing a Perpetuity Entity for all Financial Stakeholders Be sure to carefully read the Introduction and the Hint (in red) before starting this problem. Introduction SpudsterCo (SC) is a profitable entity, capitalized with debt and equity operating in steady-state forever. Your Equity/Debt investor team is considering buying it and restructuring its debt. To execute this deal, the team will have to purchase 100% of SC's stock, and pay the principal on the entity's loan. (IE: When your team takes over the firm, the lender will exersize her "change of control put"). The asking price for 100% of the firm's stock is: $100 MM. The principle to be repaid on the loan is: $100 MM. Your team believes that an optimal capital structure for the firm would be: 40% D/(D+E). If your team proceeds with the SpudsterCo transaction: - The equity investors will pay (1-D/(D+E))% of the purchase price from their own funds. - SpudsterCo will take out a long-term loan at the moment of close, provided by the debt investors on the team, to pay the current owners the rest of the purchase price, and to pay the existing loan principle. - The equity investors will operate SpudsterCo in its recapitalized steady-state forever. Hint: This is just like the problems presented in class and Practice Problems except The total cash that your team needs to raise (D+E) includes the amount needed to buy all the equity, and the amount needed to repay the principle owed on the exisiting debt. Existing $200.0 As Purchased $200.0 Financing Structure PP (D+E) = D + E = CAPtot = Market's view of Enterprise Value D/(D + E) = Wp D E 40.0% 50.0% $100.0 $100.0 1 2 Key Rates rp Income Tax rate Existing 9.00% 33.00% 8.34% As Purchased 8.000% 33.000% 7.629% 6.722% rwACC 7.187% Free Cash Flows FCF (D+E) Partial Income Statement, NOPAT and FCFS ($MM UON) Revenue - Depreciation - Other Expenses = EBIT -Tax on EBIT = NOPAT Existing $132.00 ($45.00) ($60.00) $27.00 As Purchased $132.00 ($45.00) ($60.00) $27.00 3 4 - A Working Capital + Depreciation - CAPX = FCF (D+E) 5 Valuation at T=0 Valuation 6.72% rwACC PV(D+E) = Team's Estimate of Enterprise Value 6 $200.00 PP (D+E) = Purchase price (stock + loan) = Market's view of Enterprise Value NPV (O+E) 7

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting Tools For Business Decision Making

Authors: Paul D. Kimmel

3rd Canadian Edition

0470836792, 978-0470836798