Answered step by step

Verified Expert Solution

Question

1 Approved Answer

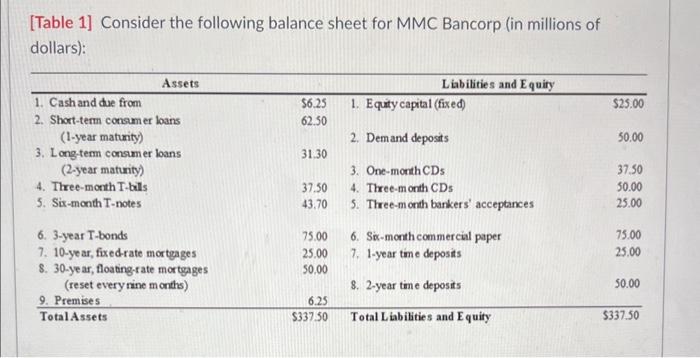

1. what is the repricing gap over the next year for the MMC? Hint: First, caluclate one-year rate-sensitive liabilities. a) -$62,550,000 b) $18,800,000 c) -$68,800,000

1. what is the repricing gap over the next year for the MMC? Hint: First, caluclate one-year rate-sensitive liabilities.

a) -$62,550,000

b) $18,800,000

c) -$68,800,000

d) -$12,550,000

e) -$18,800,000

2. Assume the same information from [Table 1] as in previous question.

Calculate the expected change in the net interest incime for the bank if interest rates rise by 1 percent on both RSAs and RSLs.

a) $188,000

b) -$688,000

c) -$625,500

d) -$125,500

e) -$188,000

3. calculate the wxpected change in the net interest income for the bank if interest rates rise by 1.2 percent on RSAs and by 1 percent on RSLs.

a) $199,400

b) -$225,600

c) $188,000

d) -$199,400

e) -$188,000

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Options Futures And Other Derivatives

Authors: John Hull

11th Global Edition

1292410655, 9781292410654