Question

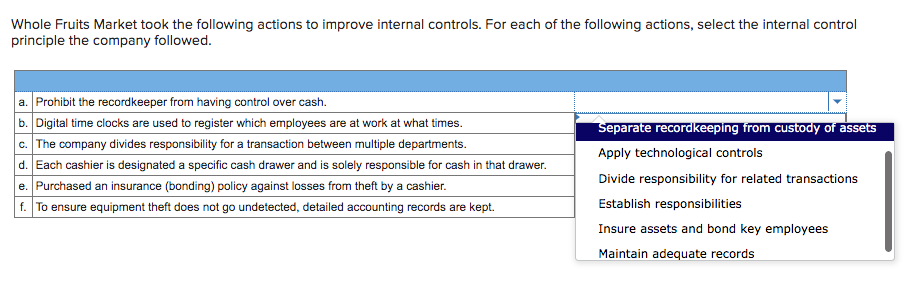

1. Whole Fruits Market took the following actions to improve internal controls. For each of the following actions, select the internal control principle the company

1. Whole Fruits Market took the following actions to improve internal controls. For each of the following actions, select the internal control principle the company followed.

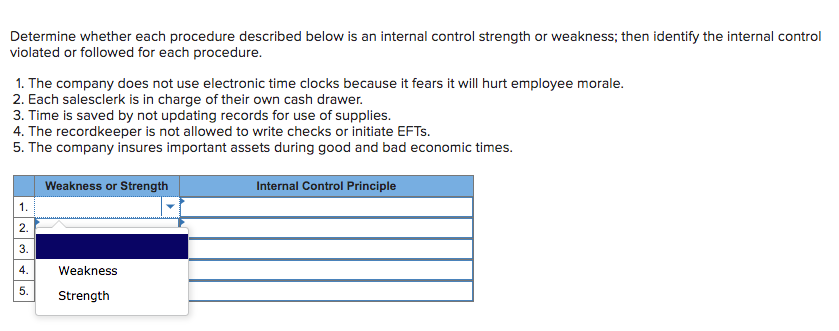

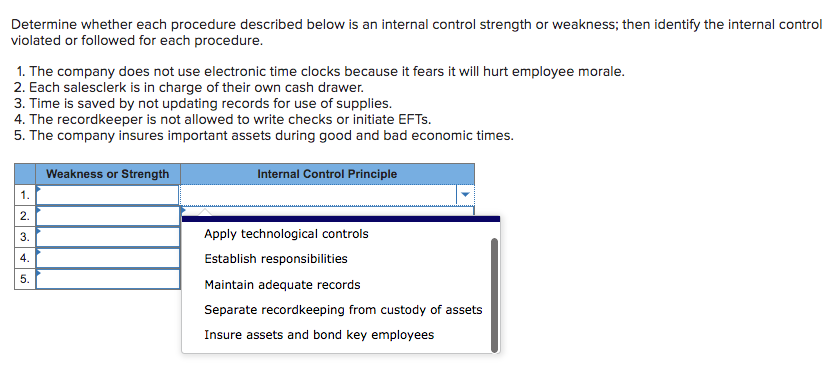

2. Determine whether each procedure described below is an internal control strength or weakness; then identify the internal control violated or followed for each procedure.

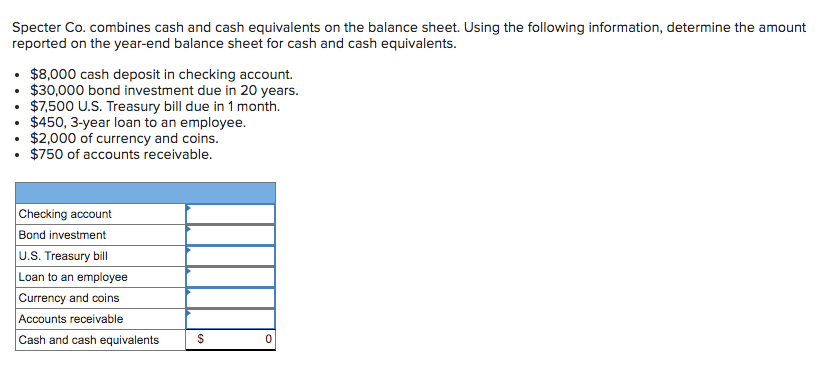

3. Specter Co. combines cash and cash equivalents on the balance sheet. Using the following information, determine the amount reported on the year-end balance sheet for cash and cash equivalents.

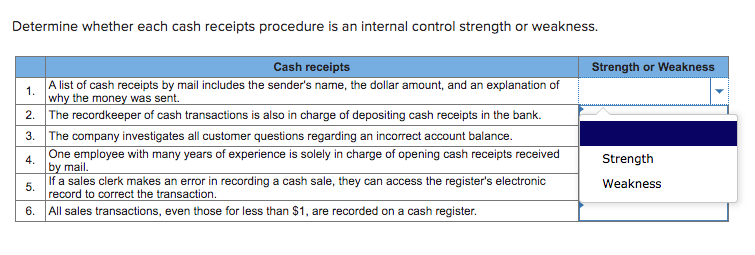

4. Determine whether each cash receipts procedure is an internal control strength or weakness.

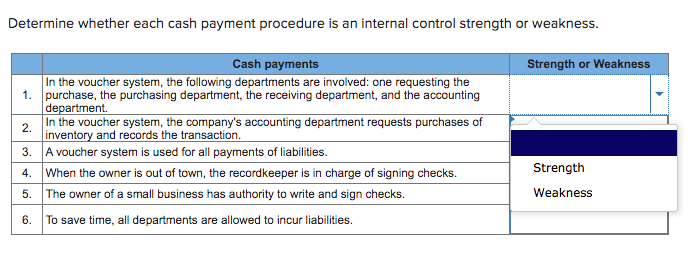

5. Determine whether each cash payment procedure is an internal control strength or weakness.

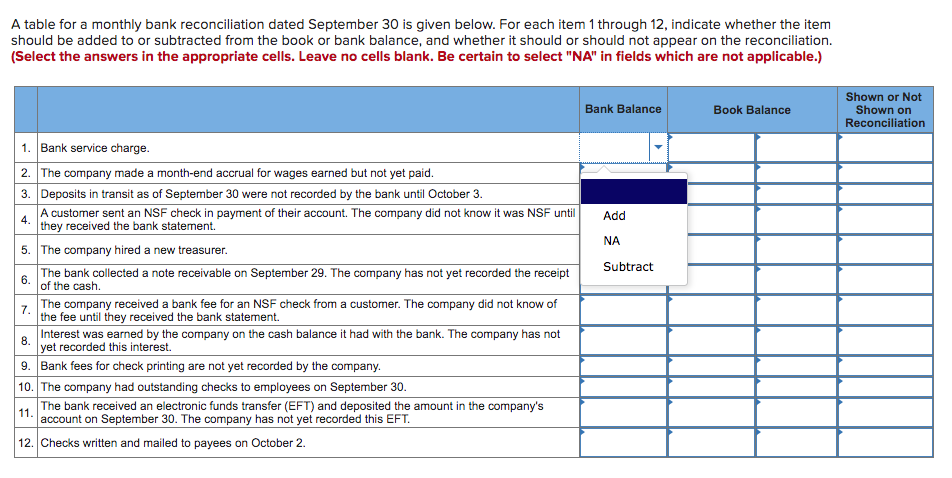

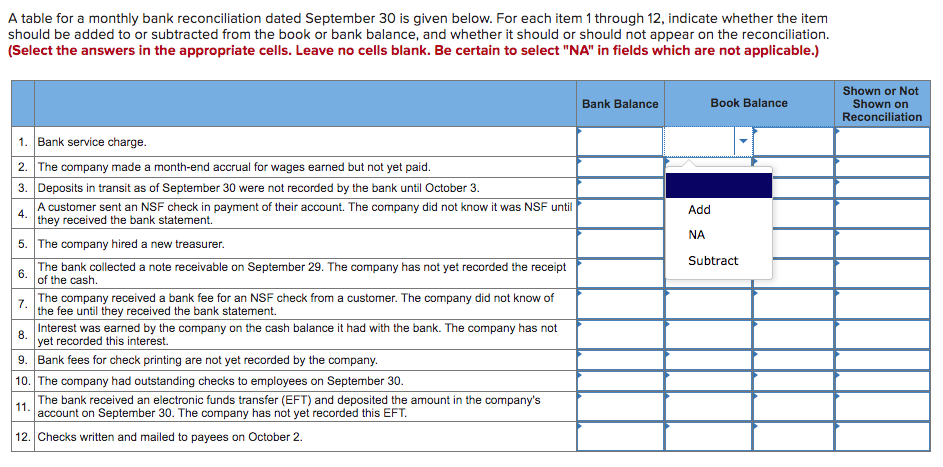

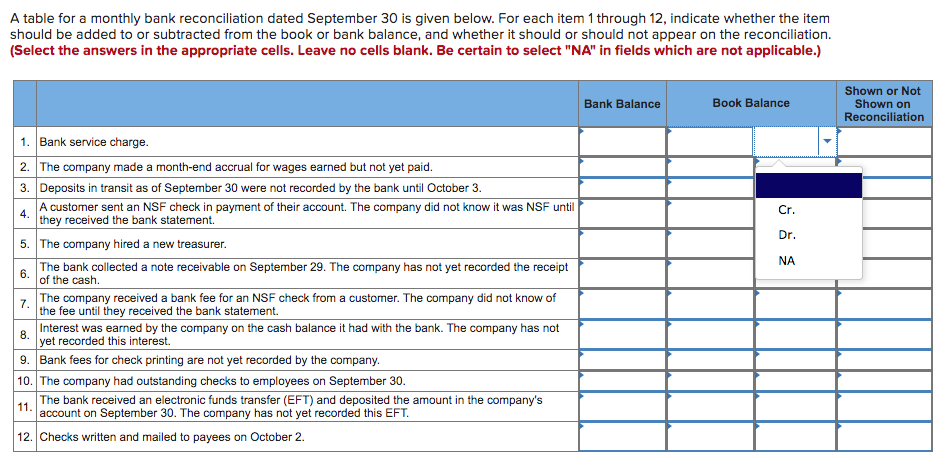

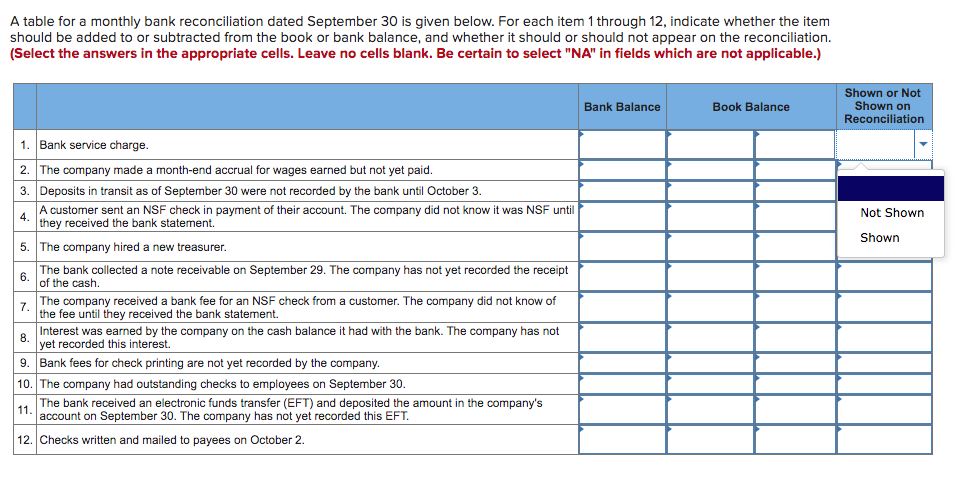

6. A table for a monthly bank reconciliation dated September 30 is given below. For each item 1 through 12, indicate whether the item should be added to or subtracted from the book or bank balance, and whether it should or should not appear on the reconciliation.

Whole Fruits Market took the following actions to improve internal controls. For each of the following actions, select the internal control principle the company followed. a. Prohibit the recordkeeper from having control over cash. b. Digital time clocks are used to register which employees are at work at what times. c. The company divides responsibility for a transaction between multiple departments. d. Each cashier is designated a specific cash drawer and is solely responsible for cash in that drawer. e. Purchased an insurance (bonding) policy against losses from theft by a cashier. f. To ensure equipment theft does not go undetected, detailed accounting records are kept. Separate recordkeeping from custody of assets Apply technological controls Divide responsibility for related transactions Establish responsibilities Insure assets and bond key employees Maintain adequate records Determine whether each procedure described below is an internal control strength or weakness; then identify the internal control violated or followed for each procedure. 1. The company does not use electronic time clocks because it fears it will hurt employee morale. 2. Each salesclerk is in charge of their own cash drawer. 3. Time is saved by not updating records for use of supplies. 4. The recordkeeper is not allowed to write checks or initiate EFTs. 5. The company insures important assets during good and bad economic times. Weakness or Strength Internal Control Principle 1. 2. 3. 4. Weakness 5. Strength Determine whether each procedure described below is an internal control strength or weakness; then identify the internal control violated or followed for each procedure. 1. The company does not use electronic time clocks because it fears it will hurt employee morale. 2. Each salesclerk is in charge of their own cash drawer. 3. Time is saved by not updating records for use of supplies. 4. The recordkeeper is not allowed to write checks or initiate EFTs. 5. The company insures important assets during good and bad economic times. Weakness or Strength Internal Control Principle 1. 2. 3. 4. 5. Apply technological controls Establish responsibilities Maintain adequate records Separate recordkeeping from custody of assets Insure assets and bond key employees Specter Co. combines cash and cash equivalents on the balance sheet. Using the following information, determine the amount reported on the year-end balance sheet for cash and cash equivalents. $8,000 cash deposit in checking account. $30,000 bond investment due in 20 years. $7,500 U.S. Treasury bill due in 1 month. $450, 3-year loan to an employee. $2,000 of currency and coins. $750 of accounts receivable. Checking account Bond investment U.S. Treasury bill Loan to an employee Currency and coins Accounts receivable Cash and cash equivalents S 0 Determine whether each cash receipts procedure is an internal control strength or weakness. Strength or Weakness 1. Cash receipts A list of cash receipts by mail includes the sender's name, the dollar amount, and an explanation of why the money was sent. 2. The recordkeeper of cash transactions is also in charge of depositing cash receipts in the bank. 3. The company investigates all customer questions regarding an incorrect account balance. One employee with many years of experience is solely in charge of opening cash receipts received by mail. If a sales clerk makes an error in recording a cash sale, they can access the register's electronic record to correct the transaction. 6. All sales transactions, even those for less than $1, are recorded on a cash register. 4. Strength Weakness 5. Determine whether each cash payment procedure is an internal control strength or weakness. Strength or Weakness 2. Cash payments In the voucher system, the following departments are involved: one requesting the 1. purchase, the purchasing department, the receiving department, and the accounting department In the voucher system, the company's accounting department requests purchases of inventory and records the transaction. 3. A voucher system is used for all payments of liabilities. 4. When the owner is out of town, the recordkeeper is in charge of signing checks. The owner of a small business has authority to write and sign checks. 6. To save time, all departments are allowed to incur liabilities. Strength 5. Weakness A table for a monthly bank reconciliation dated September 30 is given below. For each item 1 through 12, indicate whether the item should be added to or subtracted from the book or bank balance, and whether it should or should not appear on the reconciliation. (Select the answers in the appropriate cells. Leave no cells blank. Be certain to select "NA" in fields which are not applicable.) Bank Balance Book Balance Shown or Not Shown on Reconciliation Add NA Subtract 6. 1. Bank service charge. 2. The company made a month-end accrual for wages earned but not yet paid. 3. Deposits in transit as of September 30 were not recorded by the bank until October 3. A customer sent an NSF check in payment of their account. The company did not know it was NSF until 4. they received the bank statement 5. The company hired a new treasurer. The bank collected a note receivable on September 29. The company has not yet recorded the receipt of the cash 7. The company received a bank fee for an NSF check from a customer. The company did not know of the fee until they received the bank statement Interest was earned by the company on the cash balance it had with the bank. The company has not yet recorded this interest. 9. Bank fees for check printing are not yet recorded by the company. 10. The company had outstanding checks to employees on September 30. 11. The bank received an electronic funds transfer (EFT) and deposited the amount in the company's account on September 30. The company has not yet recorded this EFT. 12. Checks written and mailed to payees on October 2. 8. A table for a monthly bank reconciliation dated September 30 is given below. For each item 1 through 12, indicate whether the item should be added to or subtracted from the book or bank balance, and whether it should or should not appear on the reconciliation. (Select the answers in the appropriate cells. Leave no cells blank. Be certain to select "NA" in fields which are not applicable.) Bank Balance Book Balance Shown or Not Shown on Reconciliation 4. Add NA Subtract 1. Bank service charge. 2. The company made a month-end accrual for wages earned but not yet paid. 3. Deposits in transit as of September 30 were not recorded by the bank until October 3. A customer sent an NSF check in payment of their account. The company did not know it was NSF until they received the bank statement. 5. The company hired a new treasurer. 6. The bank collected a note receivable on September 29. The company has not yet recorded the receipt of the cash 7. The company received a bank fee for an NSF check from a customer. The company did not know of the fee until they received the bank statement. Interest was earned by the company on the cash balance it had with the bank. The company has not yet recorded this interest. 9. Bank fees for check printing are not yet recorded by the company. 10. The company had outstanding checks to employees on September 30. The bank received an electronic funds transfer (EFT) and deposited the amount in the company's account on September 30. The company has not yet recorded this EFT. 12. Checks written and mailed to payees on October 2. 8. 11. A table for a monthly bank reconciliation dated September 30 is given below. For each item 1 through 12, indicate whether the item should be added to or subtracted from the book or bank balance, and whether it should or should not appear on the reconciliation. (Select the answers in the appropriate cells. Leave no cells blank. Be certain to select "NA" in fields which are not applicable.) Bank Balance Book Balance Shown or Not Shown on Reconciliation Cr. Dr. NA 1. Bank service charge. 2. The company made a month-end accrual for wages earned but not yet paid. 3. Deposits in transit as of September 30 were not recorded by the bank until October 3. 4. A customer sent an NSF check in payment of their account. The company did not know it was NSF until they received the bank statement. 5. The company hired a new treasurer. 6. The bank collected a note receivable on September 29. The company has not yet recorded the receipt of the cash. 7. The company received a bank fee for an NSF check from a customer. The company did not know of the fee until they received the bank statement. 8. Interest was earned by the company on the cash balance it had with the bank. The company has not yet recorded this interest. 9. Bank fees for check printing are not yet recorded by the company. 10. The company had outstanding checks to employees on September 30. 11. The bank received an electronic funds transfer (EFT) and deposited the amount in the company's account on September 30. The company has not yet recorded this EFT. 12. Checks written and iled to payees on October 2. A table for a monthly bank reconciliation dated September 30 is given below. For each item 1 through 12, indicate whether the item should be added to or subtracted from the book or bank balance, and whether it should or should not appear on the reconciliation. (Select the answers in the appropriate cells. Leave no cells blank. Be certain to select "NA" in fields which are not applicable.) Bank Balance Book Balance Shown or Not Shown on Reconciliation Not Shown 4. Shown 1. Bank service charge. 2. The company made a month-end accrual for wages earned but not yet paid. 3. Deposits in transit as of September 30 were not recorded by the bank until October 3. A customer sent an NSF check in payment of their account. The company did not know it was NSF until they received the bank statement. 5. The company hired a new treasurer. 6. The bank collected a note receivable on September 29. The company has not yet recorded the receipt of the cash. The company received a bank fee for an NSF check from a customer. The company did not know of 7. the fee until they received the bank statement. Interest was earned by the company on the cash balance it had with the bank. The company has not 8 yet recorded this interest 9. Bank fees for check printing are not yet recorded by the company. 10. The company had outstanding checks to employees on September 30. The bank received an electronic funds transfer (EFT) and deposited the amount in the company's 11. account on September 30. The company has not yet recorded this EFT. 12. Checks written and mailed to payees on October 2. 8

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial & Managerial Accounting For Undergraduates

Authors: Jason Wallace, James Nelson, Karen Christensen, Theodore Hobson, Scott L. Matthews

2nd Edition

161853310X, 9781618533104