Answered step by step

Verified Expert Solution

Question

1 Approved Answer

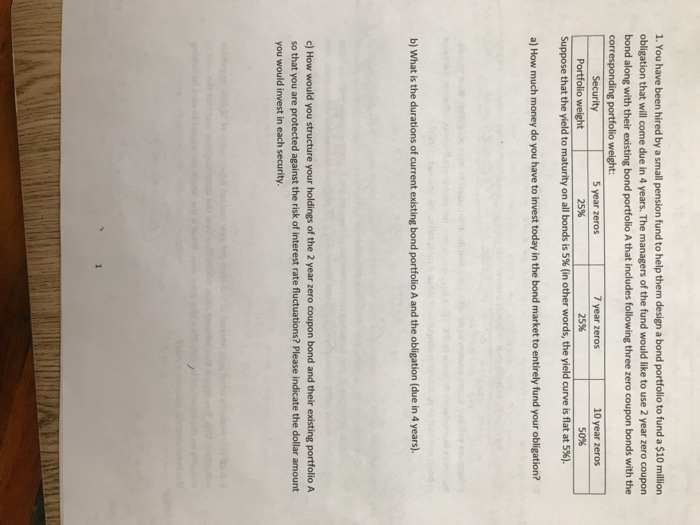

1. You have been hired by a small pension fund to help them design a bond portfolio to fund a $10 million obligation that will

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Market Integrity Do Our Equity Markets Pass The Test

Authors: Robert A. Schwartz , John Aidan Byrne, Eileen Stempel

1st Edition

3030028704,3030028712