Answered step by step

Verified Expert Solution

Question

1 Approved Answer

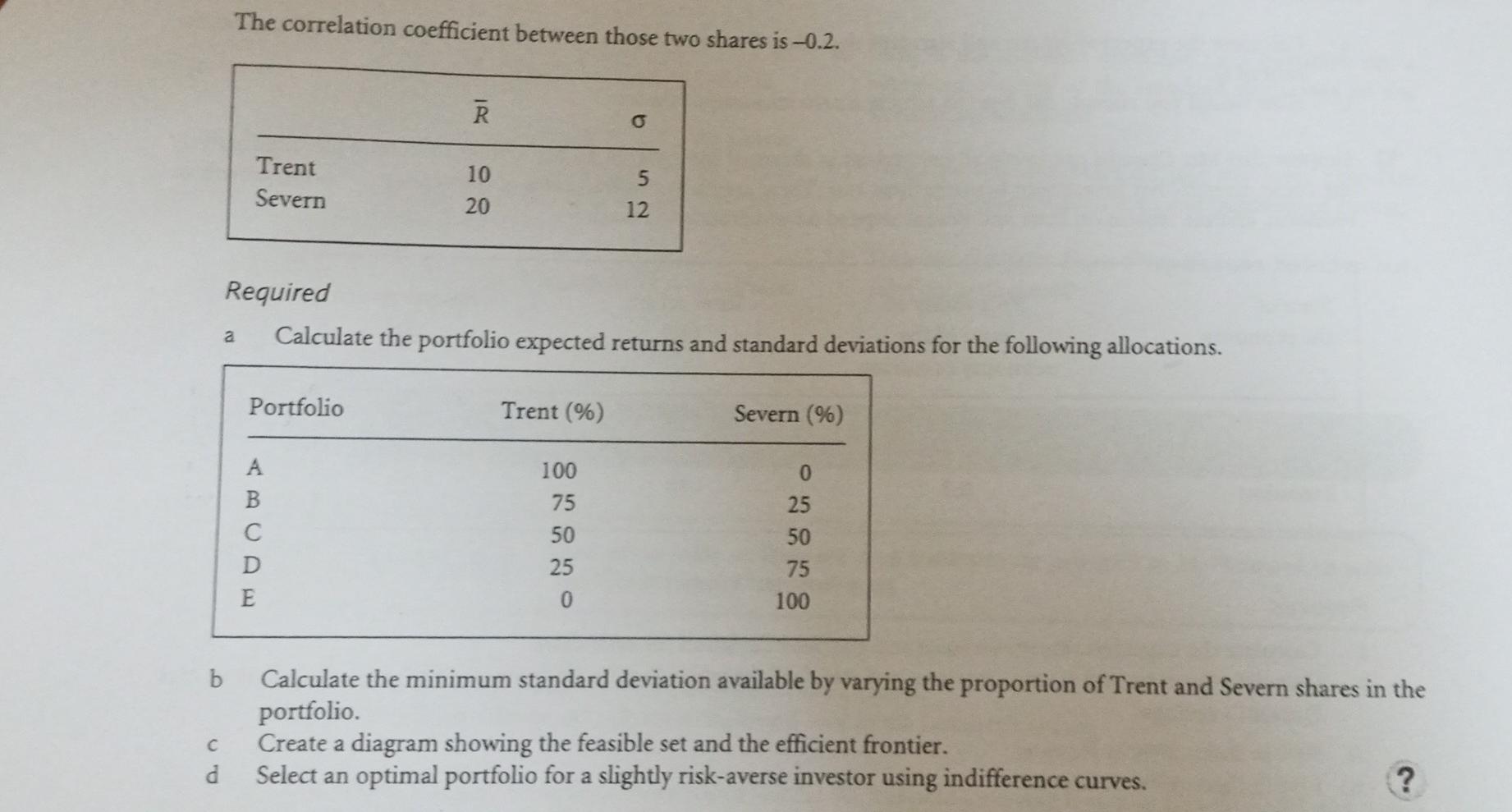

10 an investor has 100,000 to invest in shares of Trent or Severn the expected returns and standard deviations of which are as follows. The

10 an investor has 100,000 to invest in shares of Trent or Severn the expected returns and standard deviations of which are as follows. The correlation coefficient between those two shares is -0.2. b a Trent Severn 10 20 5 12 Required Calculate the portfolio expected returns and standard deviations for the following allocations. a Portfolio Trent (%) Severn (%) 0 B D E 100 75 50 25 25 50 75 0 100 b Calculate the minimum standard deviation available by varying the proportion of Trent and Severn shares in the portfolio Create a diagram showing the feasible set and the efficient frontier. Select an optimal portfolio for a slightly risk-averse investor using indifference curves. ? d

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Banking On Freedom Black Women In U.S. Finance Before The New Deal

Authors: Shennette Garrett-Scott

1st Edition

0231183917, 978-0231183918