Answered step by step

Verified Expert Solution

Question

1 Approved Answer

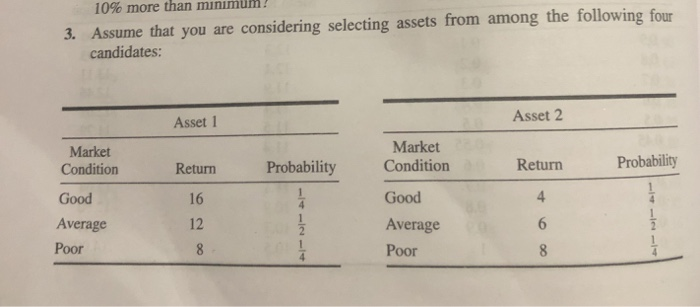

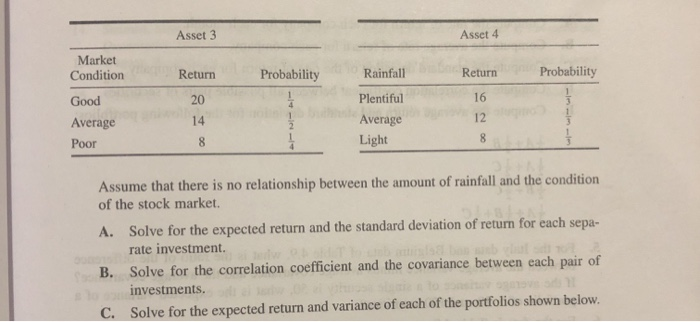

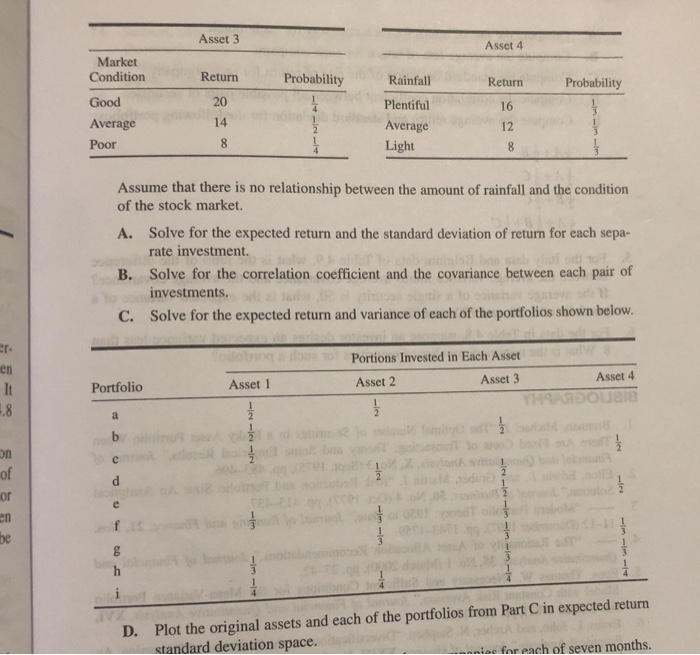

10% more than minimum! 3. Assume that you are considering selecting assets from among the following four candidates: Asset 1 Asset 2 Market Condition Market

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

ABC Finance Coloring Book Familys First Financial Literacy Book

Authors: Jason Conger

1st Edition

1955961026, 978-1955961028