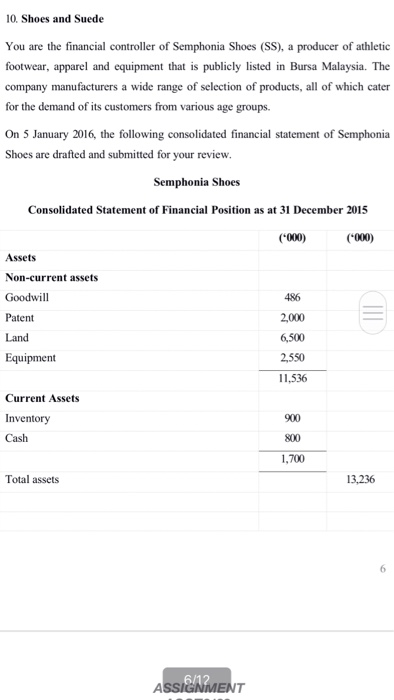

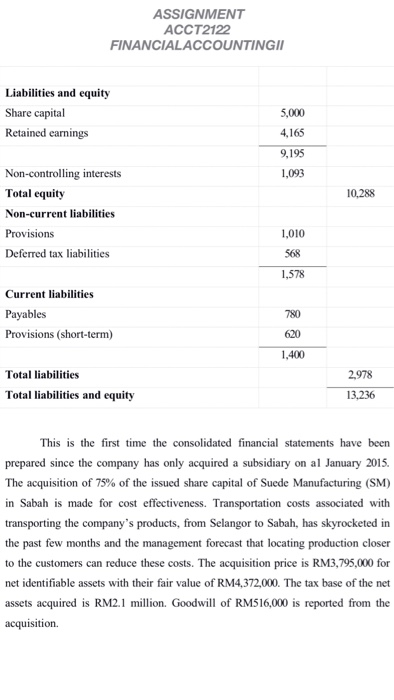

10. Shoes and Suede You are the financial controller of Semphonia Shoes (SS), a producer of athletic footwear, apparel and equipment that is publicly listed in Bursa Malaysia. The company manufacturers a wide range of selection of products, all of which cater for the demand of its customers from various age groups. On 5 January 2016, the following consolidated financial statement of Semphonia Shoes are drafted and submitted for your review. Semphonia Shoes Consolidated Statement of Financial Position as at 31 December 2015 ('000) 000) Assets Non-current assets Goodwill Patent Land Equipment 486 2,000 6,500 2,550 I 1.536 Current Assets Inventory Cash 900 800 1,700 Total assets 13,236 6/12 ASSIGNMENT ACCT2122 FINANCIALACCOUNTINGI Liabilities and equity Share capital Retained earnings 5,000 4,165 9,195 1,093 Non-controlling interests Total equity Non-current liabilities Provisions Deferred tax liabilities 10,288 1,010 568 1,578 Current liabilities Payables Provisions (short-term) 780 620 1.400 Total liabilities 2,978 Total liabilities and equity 13,236 This is the first time the consolidated financial statements have been prepared since the company has only acquired a subsidiary on al January 2015. The acquisition of 75% of the issued share capital of Suede Manufacturing (SM) in Sabah is made for cost effectiveness. Transportation costs associated with transporting the company's products, from Selangor to Sabah, has skyrocketed in the past few months and the management forecast that locating production closer to the customers can reduce these costs. The acquisition price is RM3,795,000 for net identifiable assets with their fair value of RM4,372,000. The tax base of the net assets acquired is RM2.1 milion. Goodwill of RM516,000 is reported from the FINANCIALACCOUNTINGI While most of the drafted consolidated accounts seem to be in place, you gave come across transactions with SM tha probably would affect the consolidated accounts, especially the deferred tax liability component. More specifically, you are concerned with the following a) During the current year, SM has sold goods of RM10,000 to SS. SM has made a profit of 20% on the selling price in the transaction. SS has RM5,000 worth of these goods recorded in its statement of financial position at the current year-end. b) During the year, he management of SM as declared a dividend of RM100,000, which is payable after the year-end. A liability has not been recognized in the financial statement of SM as at the year-end. Also, it has become known to you that while SS is subjected to 29% corporate income tax rate. SM is a pioneer status company that is enjoying its five years of tax exemption. Required: You need to write a memorandum to your staff to elaborate deferred tax implications that they need to consider in preparation of the consolidated financial statements. More specifically: a) Elaborate on deferred tax implications on unrealized intra-group profits eliminated on consolidation. b) The differences between goodwill on acquisition date and in the drafted accounts indicate thatoodwill is being amortized. You have identified that no impairment has occurred that involves goodwill during the year Advice on whether the amortization of goodwill has any deferred tax implications. c) There seems to be discrepancies in the calculation of deferred tax arising from the consolidation since SS and SM are subject to different tax rates. Advice on the applicable tax rates in determining deferred tax from consolidation. b) During the year, he management of SM as declared a dividend of RM100,000, which is payable after the year-end. A liability has not been recognized in the financial statement of SM as at the year-end. Also, it has become known to you that while SS is subjected to 25% corporate income tax rate. SM is a pioneer status company that is enjoying its five years of tax exemption Required: You need to write a memorandum to your staff to elaborate deferred tax implications that they need to consider in preparation of the consolidated financial statements. More specifically a) Elaborate on deferred tax implications on unrealized intra-group profits eliminated on consolidation. b) The differences between goodwill on acquisition date and in the drafted accounts indicate that good is being amortized. You have identified that no impairment has occurred that involves goodwill during the year Advice on whether the amortization of goodwill has any deferred tax implications. c) There seems to be discrepancies in the calculation of deferred tax arising from the consolidation since SS and SM are subject to different tax rates. Advice on the applicable tax rates in determining deferred tax from consolidation. ASSIGNMENT ACCT2122 FINANCIALACCOUNTINGI d) Suggest disclosures to be included in the company's consolidated financial statements for the year ended 31 December 2015. 10. Shoes and Suede You are the financial controller of Semphonia Shoes (SS), a producer of athletic footwear, apparel and equipment that is publicly listed in Bursa Malaysia. The company manufacturers a wide range of selection of products, all of which cater for the demand of its customers from various age groups. On 5 January 2016, the following consolidated financial statement of Semphonia Shoes are drafted and submitted for your review. Semphonia Shoes Consolidated Statement of Financial Position as at 31 December 2015 ('000) 000) Assets Non-current assets Goodwill Patent Land Equipment 486 2,000 6,500 2,550 I 1.536 Current Assets Inventory Cash 900 800 1,700 Total assets 13,236 6/12 ASSIGNMENT ACCT2122 FINANCIALACCOUNTINGI Liabilities and equity Share capital Retained earnings 5,000 4,165 9,195 1,093 Non-controlling interests Total equity Non-current liabilities Provisions Deferred tax liabilities 10,288 1,010 568 1,578 Current liabilities Payables Provisions (short-term) 780 620 1.400 Total liabilities 2,978 Total liabilities and equity 13,236 This is the first time the consolidated financial statements have been prepared since the company has only acquired a subsidiary on al January 2015. The acquisition of 75% of the issued share capital of Suede Manufacturing (SM) in Sabah is made for cost effectiveness. Transportation costs associated with transporting the company's products, from Selangor to Sabah, has skyrocketed in the past few months and the management forecast that locating production closer to the customers can reduce these costs. The acquisition price is RM3,795,000 for net identifiable assets with their fair value of RM4,372,000. The tax base of the net assets acquired is RM2.1 milion. Goodwill of RM516,000 is reported from the FINANCIALACCOUNTINGI While most of the drafted consolidated accounts seem to be in place, you gave come across transactions with SM tha probably would affect the consolidated accounts, especially the deferred tax liability component. More specifically, you are concerned with the following a) During the current year, SM has sold goods of RM10,000 to SS. SM has made a profit of 20% on the selling price in the transaction. SS has RM5,000 worth of these goods recorded in its statement of financial position at the current year-end. b) During the year, he management of SM as declared a dividend of RM100,000, which is payable after the year-end. A liability has not been recognized in the financial statement of SM as at the year-end. Also, it has become known to you that while SS is subjected to 29% corporate income tax rate. SM is a pioneer status company that is enjoying its five years of tax exemption. Required: You need to write a memorandum to your staff to elaborate deferred tax implications that they need to consider in preparation of the consolidated financial statements. More specifically: a) Elaborate on deferred tax implications on unrealized intra-group profits eliminated on consolidation. b) The differences between goodwill on acquisition date and in the drafted accounts indicate thatoodwill is being amortized. You have identified that no impairment has occurred that involves goodwill during the year Advice on whether the amortization of goodwill has any deferred tax implications. c) There seems to be discrepancies in the calculation of deferred tax arising from the consolidation since SS and SM are subject to different tax rates. Advice on the applicable tax rates in determining deferred tax from consolidation. b) During the year, he management of SM as declared a dividend of RM100,000, which is payable after the year-end. A liability has not been recognized in the financial statement of SM as at the year-end. Also, it has become known to you that while SS is subjected to 25% corporate income tax rate. SM is a pioneer status company that is enjoying its five years of tax exemption Required: You need to write a memorandum to your staff to elaborate deferred tax implications that they need to consider in preparation of the consolidated financial statements. More specifically a) Elaborate on deferred tax implications on unrealized intra-group profits eliminated on consolidation. b) The differences between goodwill on acquisition date and in the drafted accounts indicate that good is being amortized. You have identified that no impairment has occurred that involves goodwill during the year Advice on whether the amortization of goodwill has any deferred tax implications. c) There seems to be discrepancies in the calculation of deferred tax arising from the consolidation since SS and SM are subject to different tax rates. Advice on the applicable tax rates in determining deferred tax from consolidation. ASSIGNMENT ACCT2122 FINANCIALACCOUNTINGI d) Suggest disclosures to be included in the company's consolidated financial statements for the year ended 31 December 2015