Answered step by step

Verified Expert Solution

Question

1 Approved Answer

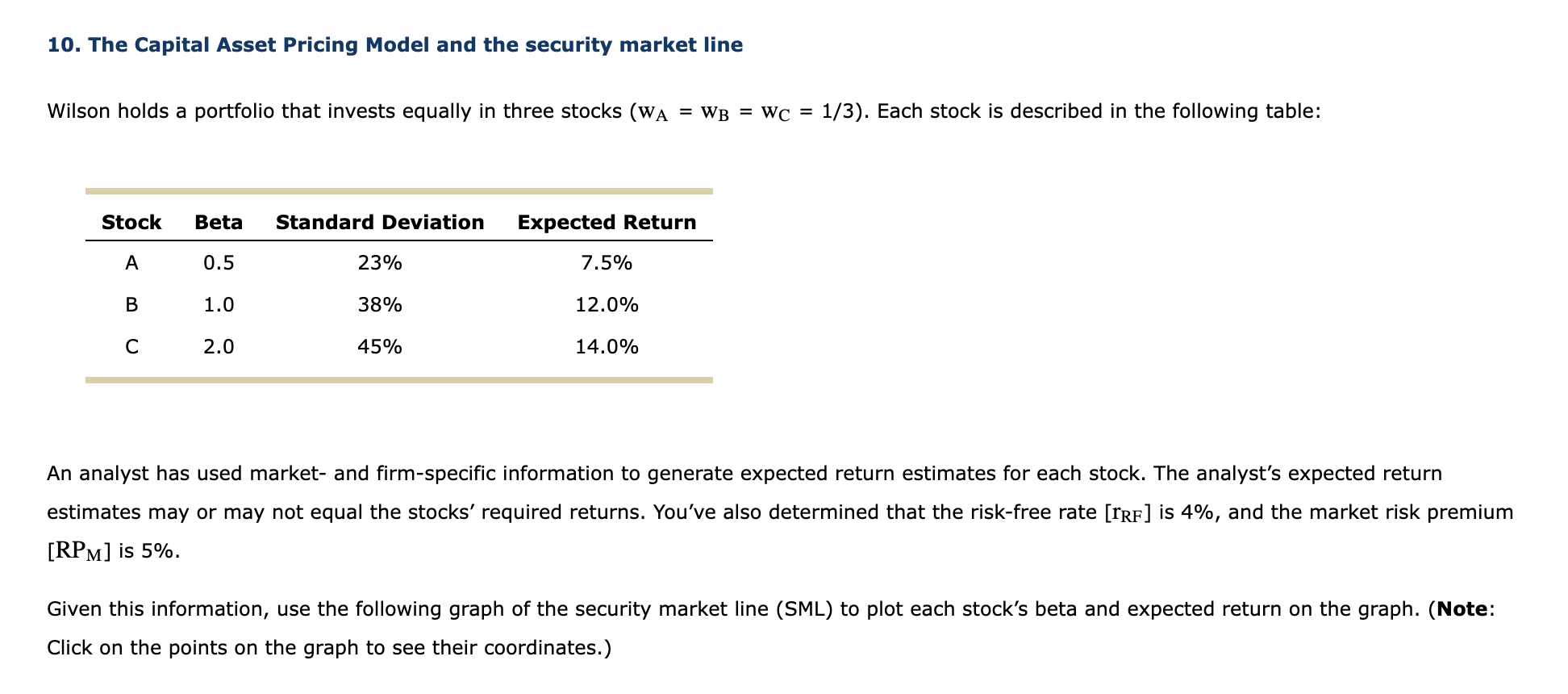

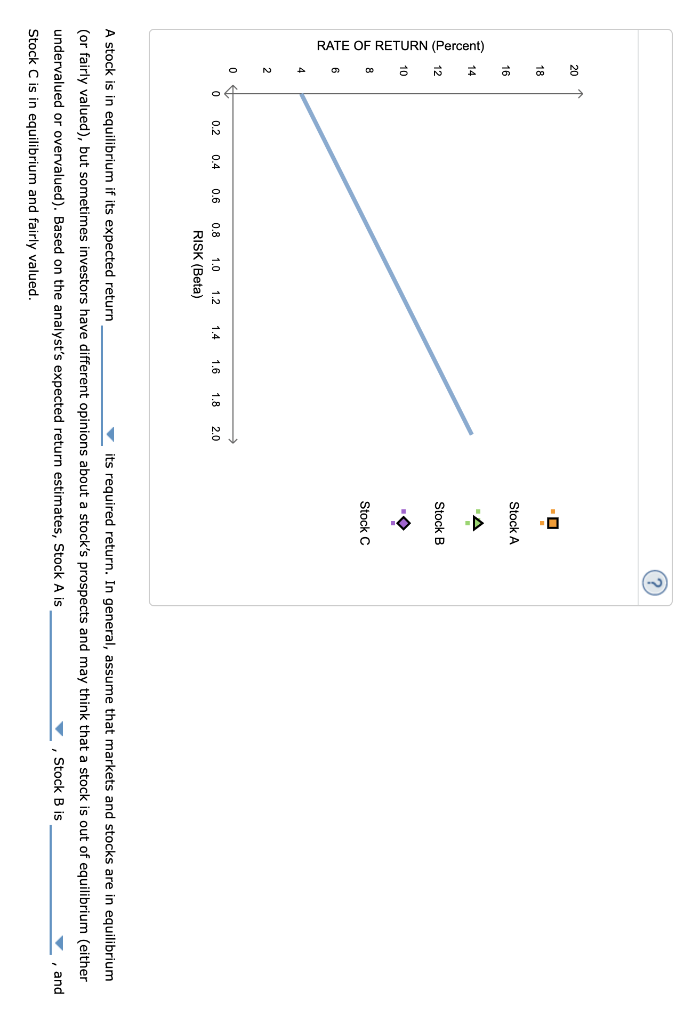

10. The Capital Asset Pricing Model and the security market line Wilson holds a portfolio that invests equally in three stocks ( wA=wB=wC=1/3). Each stock

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Environmental Finance And Investments

Authors: Marc Chesney, Jonathan Gheyssens, Anca Claudia Pana, Luca Taschini

2nd Edition

366248174X, 978-3662481745