Answered step by step

Verified Expert Solution

Question

1 Approved Answer

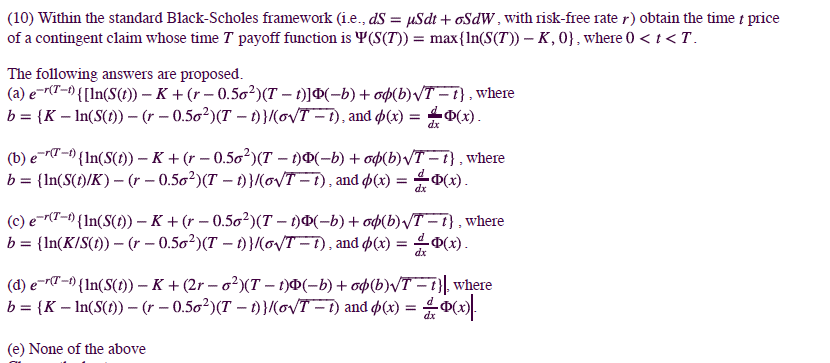

(10) Within the standard Black-Scholes framework (i.e., ds = usdt + SdW, with risk-free rate r) obtain the time price of a contingent claim whose

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Analysis for Financial Management

Authors: Robert Higgins

11th edition

77861787, 978-0077861780