Answered step by step

Verified Expert Solution

Question

1 Approved Answer

10.5.......................................................... Please answer.B Suppose the market portfolio is equally likely to increase by 30% or decrease by 10%. Also suppose that the risk-free interest rate

10.5..........................................................

Please answer.B

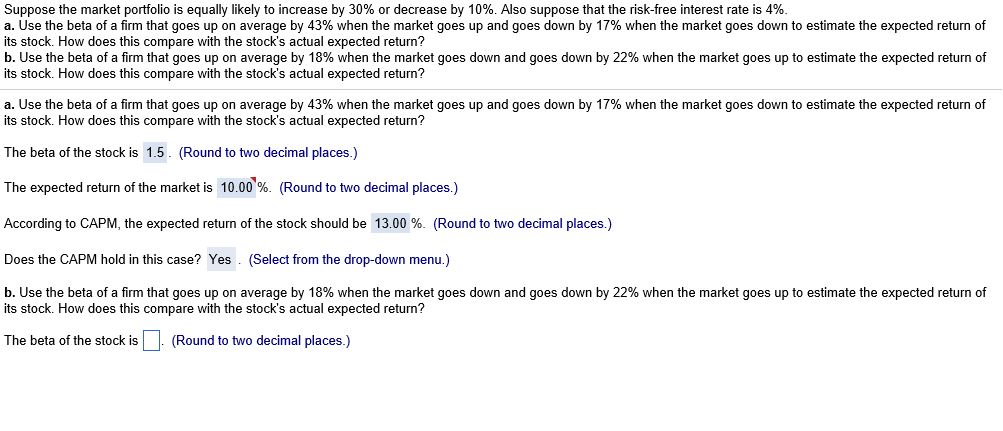

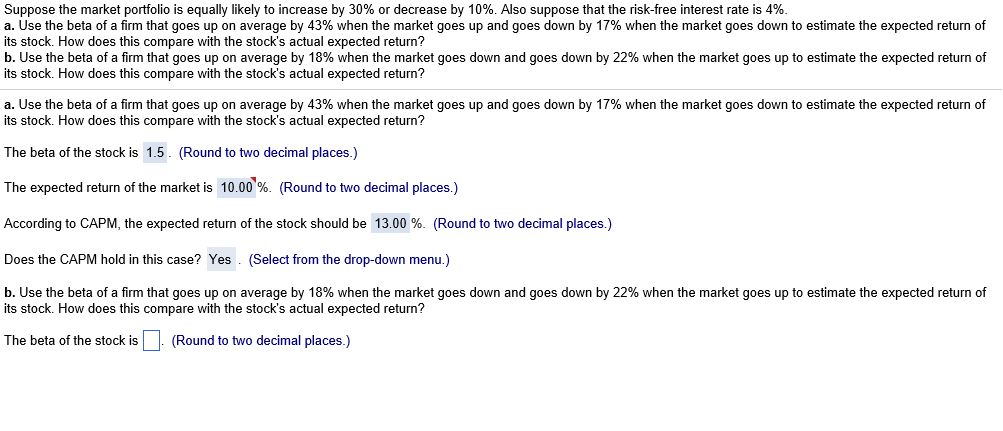

Suppose the market portfolio is equally likely to increase by 30% or decrease by 10%. Also suppose that the risk-free interest rate is 4%. a. Use the beta of a firm that goes up on average by 43% when the market goes up and goes down by 17% when the market goes down to estimate the expected retum of its stock. How does this compare with the stocks actual expected return? b. Use the beta of a firm that goes up on average by 18% when the market goes down and goes down by 22% when the market goes up to estimate the expected return of its stock. How does this compare with the stocks actual expected return? a. Use the beta of a firm that goes up on average by 43% when the market goes up and goes down by 17% when the market goes down to estimate the expected retum of its stock. How does this compare with the stock's actual expected return? The beta of the stockis f _5_ (Round to two decimal places.) The expected return of the marketis 10.00* 0K (Roundto two decimal places.) According to CAPM, the expected retum ofthe stock should be 13.00 0/0. (Roundto two decimal places.) Does the CAPM hold in this case? Yes . (Select from the drop-down menu.) b. Use the beta of a firm that goes up on average by 18% when the market goes down and goes down by 22% when the market goes up to estimate the expected return of its stock. How does this compare with the stock's actual expected retum? (Round to two decimal places.) The beta of the stock is

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Exchange Rates and International Finance

Authors: Laurence Copeland

6th edition

273786040, 978-0273786047