Answered step by step

Verified Expert Solution

Question

1 Approved Answer

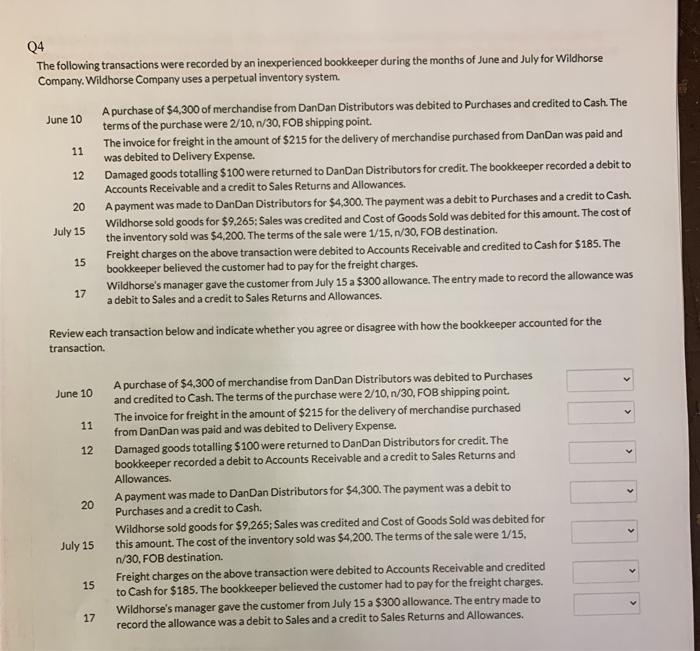

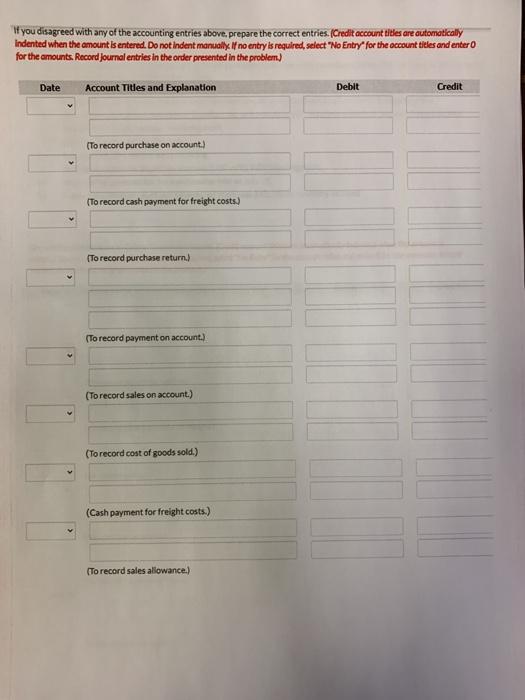

11 12 04 The following transactions were recorded by an inexperienced bookkeeper during the months of June and July for Wildhorse Company. Wildhorse Company uses

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Human Resources Audit Analysis Of And Collective Staff Performance

Authors: Hassani Moindjie MLIMI

1st Edition

6203356999, 978-6203356991