Answered step by step

Verified Expert Solution

Question

1 Approved Answer

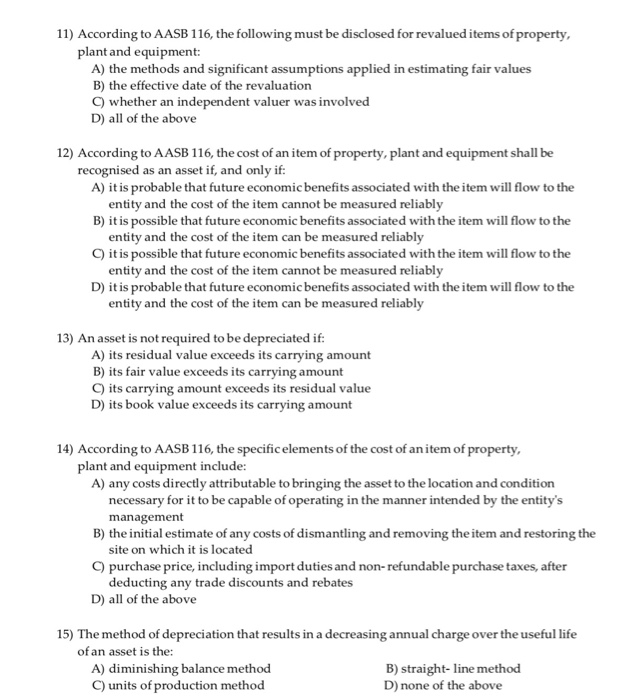

11) According to AASB 116, the following must be disclosed for revalued items of property plant and equipment: A) the methods and significant assumptions applied

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Rigos Primer Series CPA Exam Review Financial Accounting Questions And Answers

Authors: Mr. James J. Rigos

2020 Edition

979-8642293720