Answered step by step

Verified Expert Solution

Question

1 Approved Answer

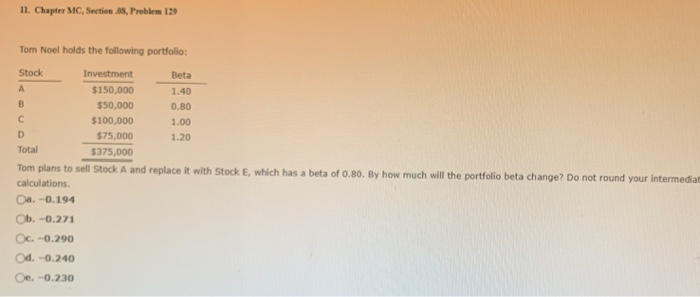

11. Chapter MC, Section 68, Problem 129 Stock Tom Noel holds the following portfolio: Investment Beta $150,000 1.40 B $50,000 0.80 $100,000 1.00 D $75,000

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cadmus Operational Auditing W R Institute Of Internal Auditors Professional Books Series

Authors: David S. Kowalczyk

1st Edition

047182660X, 978-0471826606