Answered step by step

Verified Expert Solution

Question

1 Approved Answer

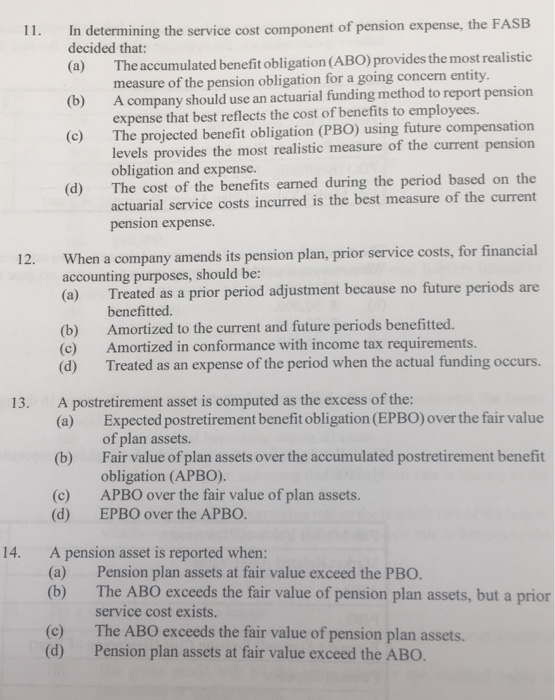

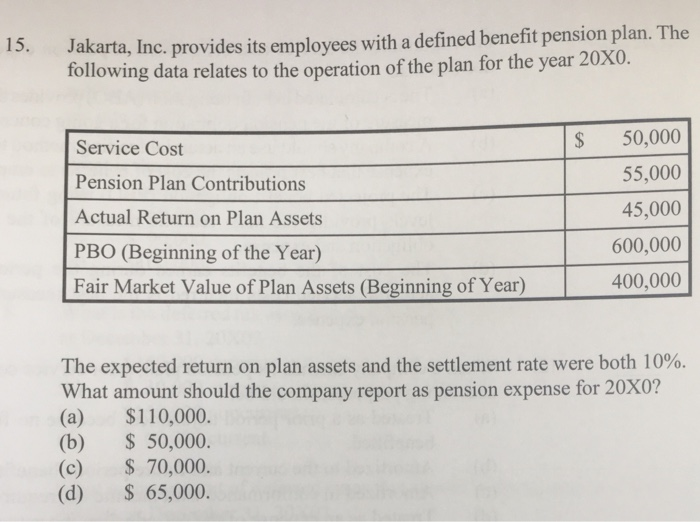

11. In determining the service cost component of pension expense, the FASB decided that: (a) The accumulated benefit obligation (ABO) provides the most realistic (b)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Guide On Marketing Audit Start Conducting A Successful Marketing Audit

Authors: Milly Anecelle

1st Edition

B0BM429R34, 979-8363321580