Answered step by step

Verified Expert Solution

Question

1 Approved Answer

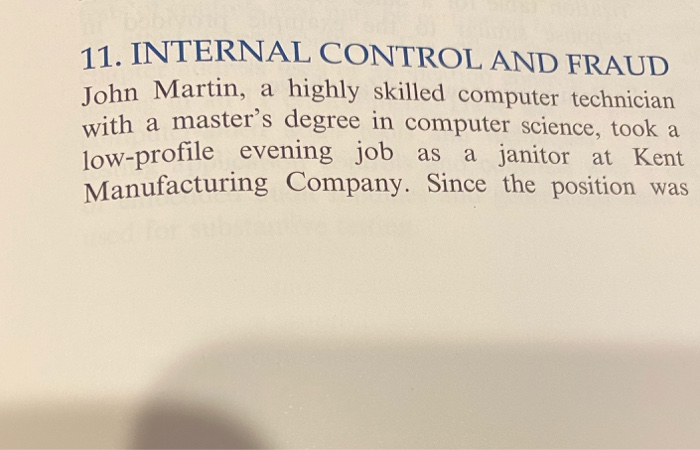

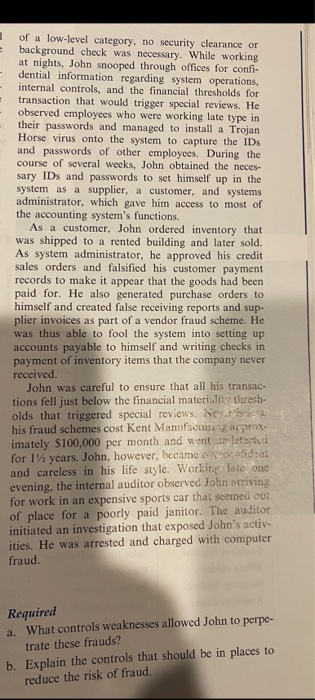

11. INTERNAL CONTROL AND FRAUD John Martin, a highly skilled computer technician with a master's degree in computer science, took a low-profile evening job as

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Quality Management Audits In Nuclear Medicine Practices

Authors: International Atomic Energy Agency (IAEA)

1st Edition

9201121083, 978-9201121080