Answered step by step

Verified Expert Solution

Question

1 Approved Answer

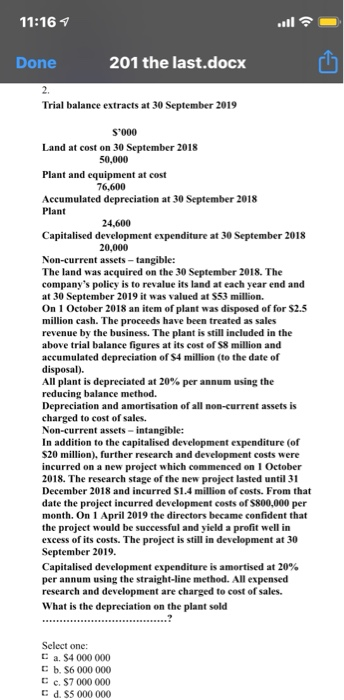

11:16 ul Done 201 the last.docx 2. Trial balance extracts at 30 September 2019 S'000 Land at cost on 30 September 2018 50,000 Plant and

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Easyinvoice Invoice Billing Reception Selling Easy To Use

Authors: Thian Thima

B0C87VL1CF