Answered step by step

Verified Expert Solution

Question

1 Approved Answer

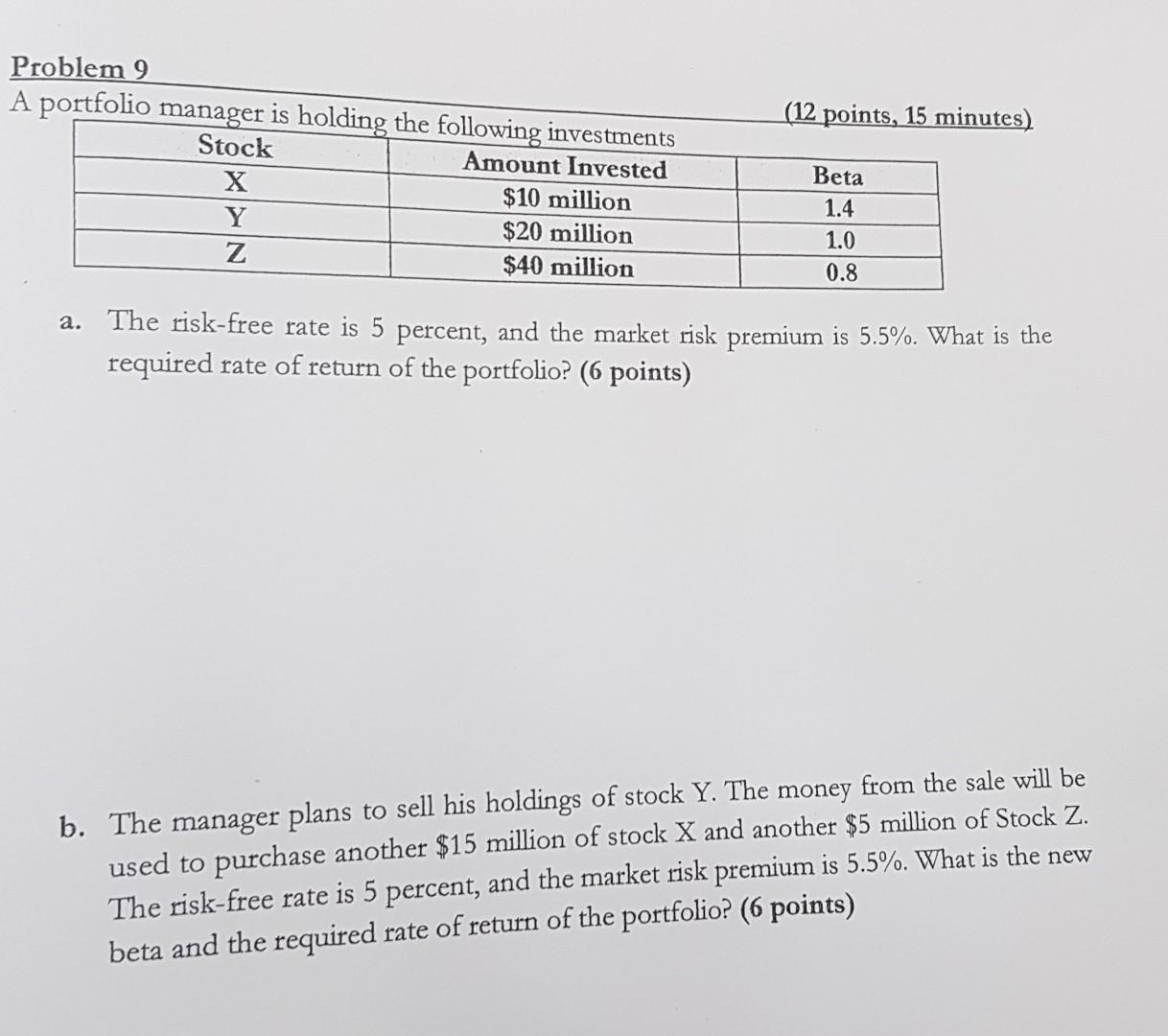

(12 points, 15 minutes) Problem 9 A portfolio manager is holding the following investments Stock Amount Invested X $10 million Y $20 million z $40

(12 points, 15 minutes) Problem 9 A portfolio manager is holding the following investments Stock Amount Invested X $10 million Y $20 million z $40 million Beta 1.4 1.0 0.8 a. The risk-free rate is 5 percent, and the market risk premium is 5.5%. What is the required rate of return of the portfolio? (6 points) b. The manager plans to sell his holdings of stock Y. The money from the sale will be used to purchase another $15 million of stock X and another $5 million of Stock Z. The risk-free rate is 5 percent, and the market risk premium is 5.5%. What is the new beta and the required rate of return of the portfolio? (6 points)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Oxford Handbook Of Sovereign Wealth Funds

Authors: Douglas J. Cumming, Geoffrey Wood, Igor Filatotchev, Juliane Reinecke

1st Edition

0198754809, 978-0198754800