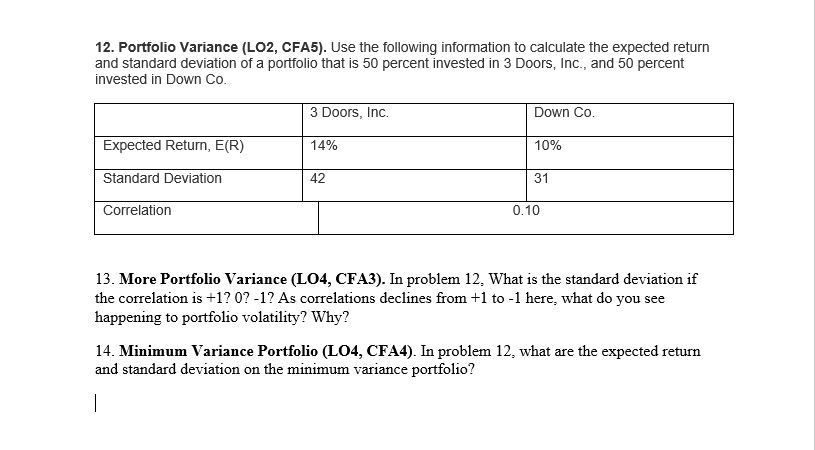

12. Portfolio Variance (LO2, CFA5). Use the following information to calculate the expected return and standard deviation of a portfolio that is 50 percent

12. Portfolio Variance (LO2, CFA5). Use the following information to calculate the expected return and standard deviation of a portfolio that is 50 percent invested in 3 Doors, Inc., and 50 percent invested in Down Co. 3 Doors, Inc. Expected Return, E(R) 14% 42 Standard Deviation Correlation Down Co. 10% 31 0.10 | 13. More Portfolio Variance (LO4, CFA3). In problem 12, What is the standard deviation if the correlation is +1? 0? -1? As correlations declines from +1 to -1 here, what do you see happening to portfolio volatility? Why? 14. Minimum Variance Portfolio (LO4, CFA4). In problem 12, what are the expected return and standard deviation on the minimum variance portfolio?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

12 Portfolio Variance Given information 3 Doors Inc Expected return ER 14 Standard deviation 42 Down Co Expected return ER 10 Standard deviation 31 Co... View full answer

Get step-by-step solutions from verified subject matter experts

100% Satisfaction Guaranteed-or Get a Refund!

Step: 2Unlock detailed examples and clear explanations to master concepts

Step: 3Unlock to practice, ask and learn with real-world examples

See step-by-step solutions with expert insights and AI powered tools for academic success

-

Access 30 Million+ textbook solutions.

Access 30 Million+ textbook solutions.

-

Ask unlimited questions from AI Tutors.

-

Order free textbooks.

-

100% Satisfaction Guaranteed-or Get a Refund!

Claim Your Hoodie Now!

Authors: Eugene F. Brigham and Michael C. Ehrhardt

13th edition

1439078106, 111197375X, 9781439078105, 9781111973759, 978-1439078099

Study Smart with AI Flashcards

Access a vast library of flashcards, create your own, and experience a game-changing transformation in how you learn and retain knowledge

Explore Flashcards