Answered step by step

Verified Expert Solution

Question

1 Approved Answer

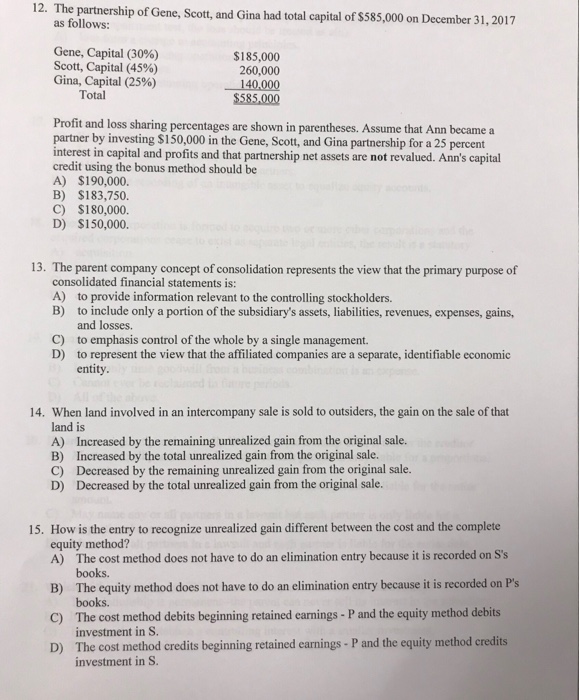

12. The partnership of Gene, Scott,and Gina had total capital of $585,000 on December 31, 2017 as follows: Gene, Capital (30%) Scott, Capital (45%) Gina,

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Marketing Audit Guide What It Is Why Your Business Needs One And How To Do It

Authors: Susan G Tyson

1st Edition

B0C12D3DD6, 979-8388994868