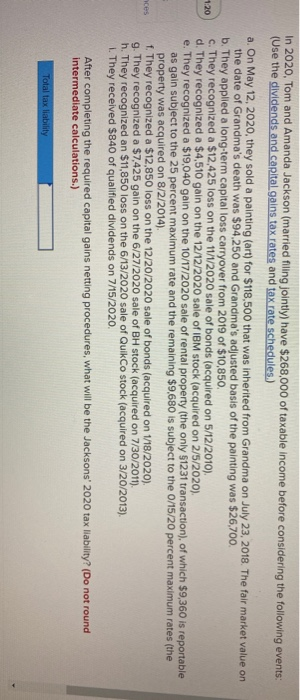

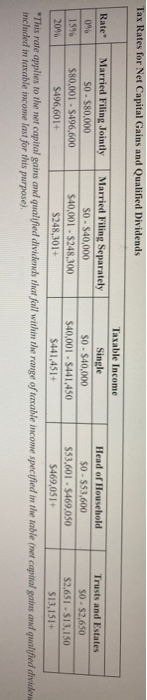

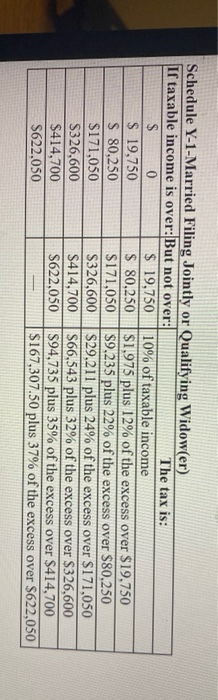

1:20 In 2020, Tom and Amanda Jackson (married filing jointly) have $268,000 of taxable income before considering the following events: (Use the dividends and capital gains tax rates and tax rate schedules.) a. On May 12, 2020, they sold a painting (art) for $118,500 that was inherited from Grandma on July 23, 2018. The fair market value on the date of Grandma's death was $94,250 and Grandma's adjusted basis of the painting was $26,700. b. They applied a long-term capital loss carryover from 2019 of $10,850. c. They recognized a $12,425 loss on the 11/1/2020 sale of bonds (acquired on 5/12/2010). d. They recognized a $4,510 gain on the 12/12/2020 sale of IBM stock (acquired on 2/5/2020). e. They recognized a $19,040 gain on the 10/17/2020 sale of rental property (the only $1231 transaction), of which $9,360 is reportable as gain subject to the 25 percent maximum rate and the remaining $9,680 is subject to the 0/15/20 percent maximum rates (the property was acquired on 8/2/2014) f. They recognized a $12,850 loss on the 12/20/2020 sale of bonds (acquired on 1/18/2020). 9. They recognized a $7,425 gain on the 6/27/2020 sale of BH stock (acquired on 7/30/2011). h. They recognized an $11,850 loss on the 6/13/2020 sale of QulkCo stock (acquired on 3/20/2013). 1. They received $840 of qualified dividends on 7/15/2020. After completing the required capital gains netting procedures, what will be the Jacksons' 2020 tax liability? (Do not round intermediate calculations.) nces Total tax liability Tax Rates for Net Capital Gains and Qualified Dividends Taxable income Rate" Married Filing Jointly Married Filing Separately Single Head of Household Trusts and Estates 09 SO - $80,000 SO - S40,000 SO - $40,000 50 - 553,600 50 - 52,650 1596 $80,001 - S496,600 $40,001 - $248,300 $40,001 - $441,450 S53,601 - $469,050 $2,651 - 513,150 20 S496,601+ S248,301 + $441,451+ $469,051+ $13,151+ *This rate applies to the ner capital gains and qualified dividends that fall within the range of taxable income specified in the table nel capital gains and qualified divide included in taxable income last for this purpose), Schedule Y-1-Married Filing Jointly or Qualifying Widow(er) If taxable income is over: But not over: The tax is: $ 0 $ 19,750 10% of taxable income $ 19,750 S 80,250 $1,975 plus 12% of the excess over $19,750 S 80,250 $171,050 $9.235 plus 22% of the excess over $80,250 $171,050 S326,600 $29.211 plus 24% of the excess over $171,050 $326,600 S414,700 $66,543 plus 32% of the excess over $326,600 $414,700 $622,050 $94,735 plus 35% of the excess over $414,700 $622,050 $167,307.50 plus 37% of the excess over $622,050