Answered step by step

Verified Expert Solution

Question

1 Approved Answer

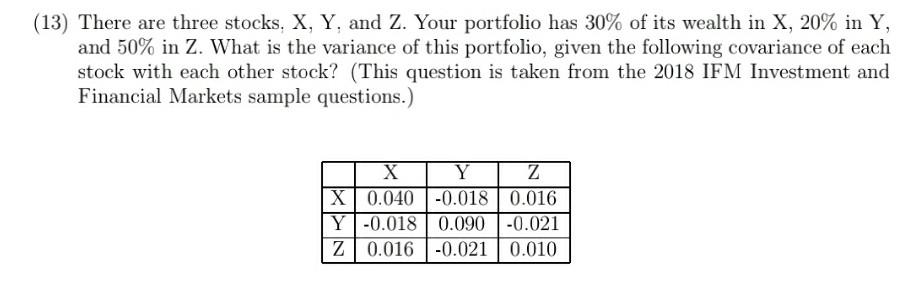

(13) There are three stocks, X, Y, and Z. Your portfolio has 30% of its wealth in X, 20% in Y, and 50% in 2.

(13) There are three stocks, X, Y, and Z. Your portfolio has 30% of its wealth in X, 20% in Y, and 50% in 2. What is the variance of this portfolio, given the following covariance of each stock with each other stock? (This question is taken from the 2018 IFM Investment and Financial Markets sample questions.) X Y Z X 0.040 -0.018 | 0.016 Y-0.018 | 0.090 -0.021 Z 0.016 -0.021 0.010

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Valuation, Measuring And Managing The Value Of Companies

Authors: Tim Koller, Marc Goedhart, David Wessels

7th Edition

1119611865, 9781119611868