Answered step by step

Verified Expert Solution

Question

1 Approved Answer

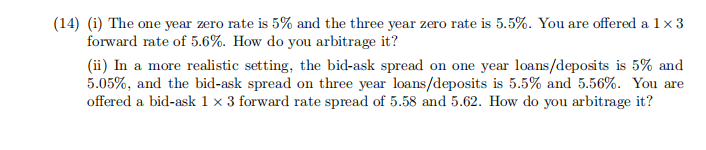

14) (i) The one year zero rate is 5% and the three year zero rate is 5.5%. You are offered a 13 forward rate of

14) (i) The one year zero rate is 5% and the three year zero rate is 5.5%. You are offered a 13 forward rate of 5.6%. How do you arbitrage it? (ii) In a more realistic setting, the bid-ask spread on one year loans/deposits is 5% and 5.05%, and the bid-ask spread on three year loans/deposits is 5.5% and 5.56%. You are offered a bid-ask 13 forward rate spread of 5.58 and 5.62. How do you arbitrage it

14) (i) The one year zero rate is 5% and the three year zero rate is 5.5%. You are offered a 13 forward rate of 5.6%. How do you arbitrage it? (ii) In a more realistic setting, the bid-ask spread on one year loans/deposits is 5% and 5.05%, and the bid-ask spread on three year loans/deposits is 5.5% and 5.56%. You are offered a bid-ask 13 forward rate spread of 5.58 and 5.62. How do you arbitrage it Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Quantitative Financial Analytics The Path To Investment Profits

Authors: Edward E Williams, John A Dobelman

1st Edition

9813224258, 978-9813224254