Question

1.4: Using the Excel Solver and the estimates from (1.3), compute the set of weights required to form a portfolio from the six stocks that

1.4: Using the Excel Solver and the estimates from (1.3), compute the set of weights required to form a portfolio from the six stocks that has zero factor risk, an expected alpha of 1% per month, and satisfies the full investment constraint (weights sum to one). This portfolio is an arbitrage portfolio as it is expected to generate alpha without any risk exposure. Include a screen shot of the Solver Dialog box you used to solve for the portfolio weights.

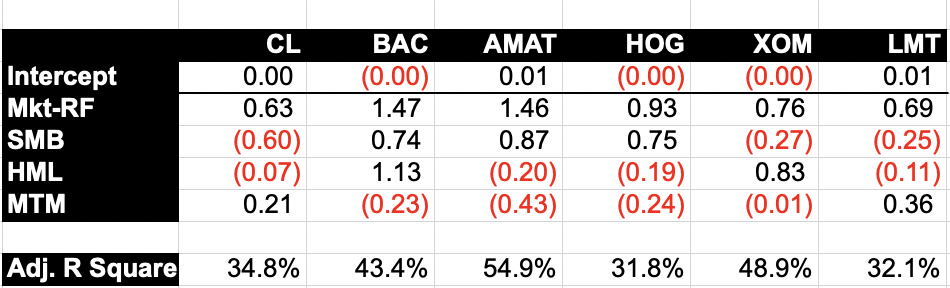

Estimates from 1.3:

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Risk Modeling Evaluation Handbook Rethinking Financial Risk Management Methodologies In The Global Capital Markets

Authors: Greg Gregoriou, Christian Hoppe, Carsten Wehn

1st Edition

0071663703, 978-0071663700