Answered step by step

Verified Expert Solution

Question

1 Approved Answer

14-29 Job costing, journal entries. The University of Delhi Press is wholly owned by the university. It per- business enterprise. The press also publishes and

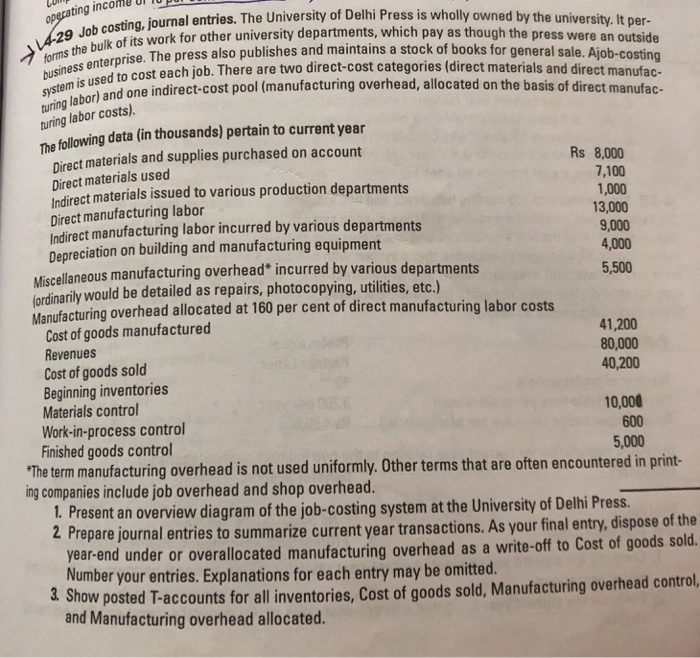

14-29 Job costing, journal entries. The University of Delhi Press is wholly owned by the university. It per- business enterprise. The press also publishes and maintains a stock of books for general sale. Ajob-costing forms the bulk of its work for other university departments, which pay as though the press were an outside turing labor) and one indirect-cost pool (manufacturing overhead, allocated on the basis of direct manufac- system is used to cost each job. There are two direct-cost categories (direct materials and direct manufac- The following data (in thousands) pertain to current year operating inco turing labor costs). Direct materials used Direct materials and supplies purchased on account Rs 8,000 7,100 Indirect materials issued to various production departments 1,000 Direct manufacturing labor 13,000 Indirect manufacturing labor incurred by various departments 9,000 Depreciation on building and manufacturing equipment 4,000 Miscellaneous manufacturing overhead* incurred by various departments 5,500 fordinarily would be detailed as repairs, photocopying, utilities, etc.) Manufacturing overhead allocated at 160 per cent of direct manufacturing labor costs Cost of goods manufactured 41,200 Revenues 80,000 Cost of goods sold 40,200 Beginning inventories Materials control 10,000 Work-in-process control 600 Finished goods control 5,000 *The term manufacturing overhead is not used uniformly. Other terms that are often encountered in print- ing companies include job overhead and shop overhead. 1. Present an overview diagram of the job-costing system at the University of Delhi Press. 2 Prepare journal entries to summarize current year transactions. As your final entry, dispose of the year-end under or overallocated manufacturing overhead as a write-off to Cost of goods sold. Number your entries. Explanations for each entry may be omitted. 3. Show posted T-accounts for all inventories, Cost of goods sold, Manufacturing overhead control, and Manufacturing overhead allocated

14-29 Job costing, journal entries. The University of Delhi Press is wholly owned by the university. It per- business enterprise. The press also publishes and maintains a stock of books for general sale. Ajob-costing forms the bulk of its work for other university departments, which pay as though the press were an outside turing labor) and one indirect-cost pool (manufacturing overhead, allocated on the basis of direct manufac- system is used to cost each job. There are two direct-cost categories (direct materials and direct manufac- The following data (in thousands) pertain to current year operating inco turing labor costs). Direct materials used Direct materials and supplies purchased on account Rs 8,000 7,100 Indirect materials issued to various production departments 1,000 Direct manufacturing labor 13,000 Indirect manufacturing labor incurred by various departments 9,000 Depreciation on building and manufacturing equipment 4,000 Miscellaneous manufacturing overhead* incurred by various departments 5,500 fordinarily would be detailed as repairs, photocopying, utilities, etc.) Manufacturing overhead allocated at 160 per cent of direct manufacturing labor costs Cost of goods manufactured 41,200 Revenues 80,000 Cost of goods sold 40,200 Beginning inventories Materials control 10,000 Work-in-process control 600 Finished goods control 5,000 *The term manufacturing overhead is not used uniformly. Other terms that are often encountered in print- ing companies include job overhead and shop overhead. 1. Present an overview diagram of the job-costing system at the University of Delhi Press. 2 Prepare journal entries to summarize current year transactions. As your final entry, dispose of the year-end under or overallocated manufacturing overhead as a write-off to Cost of goods sold. Number your entries. Explanations for each entry may be omitted. 3. Show posted T-accounts for all inventories, Cost of goods sold, Manufacturing overhead control, and Manufacturing overhead allocated

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Rehabilitation Tax Credit IRS Audit Techniques Guide

Authors: Internal Revenue Service

1st Edition

1304114686, 978-1304114686