Answered step by step

Verified Expert Solution

Question

1 Approved Answer

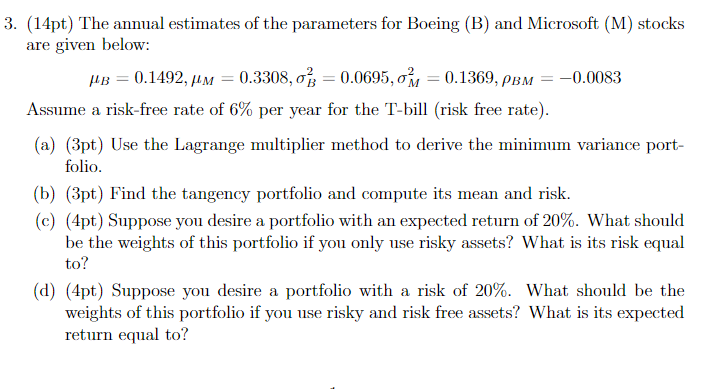

(14pt) The annual estimates of the parameters for Boeing (B) and Microsoft (M) stocks are given below: B=0.1492,M=0.3308,B2=0.0695,M2=0.1369,BM=0.0083 Assume a risk-free rate of 6% per

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Access To Finance And Its Challenge For Small Businesses Case Of Addis Ababa City Administration

Authors: Fetene Zeru

1st Edition

3639347846, 9783639347845