Answered step by step

Verified Expert Solution

Question

1 Approved Answer

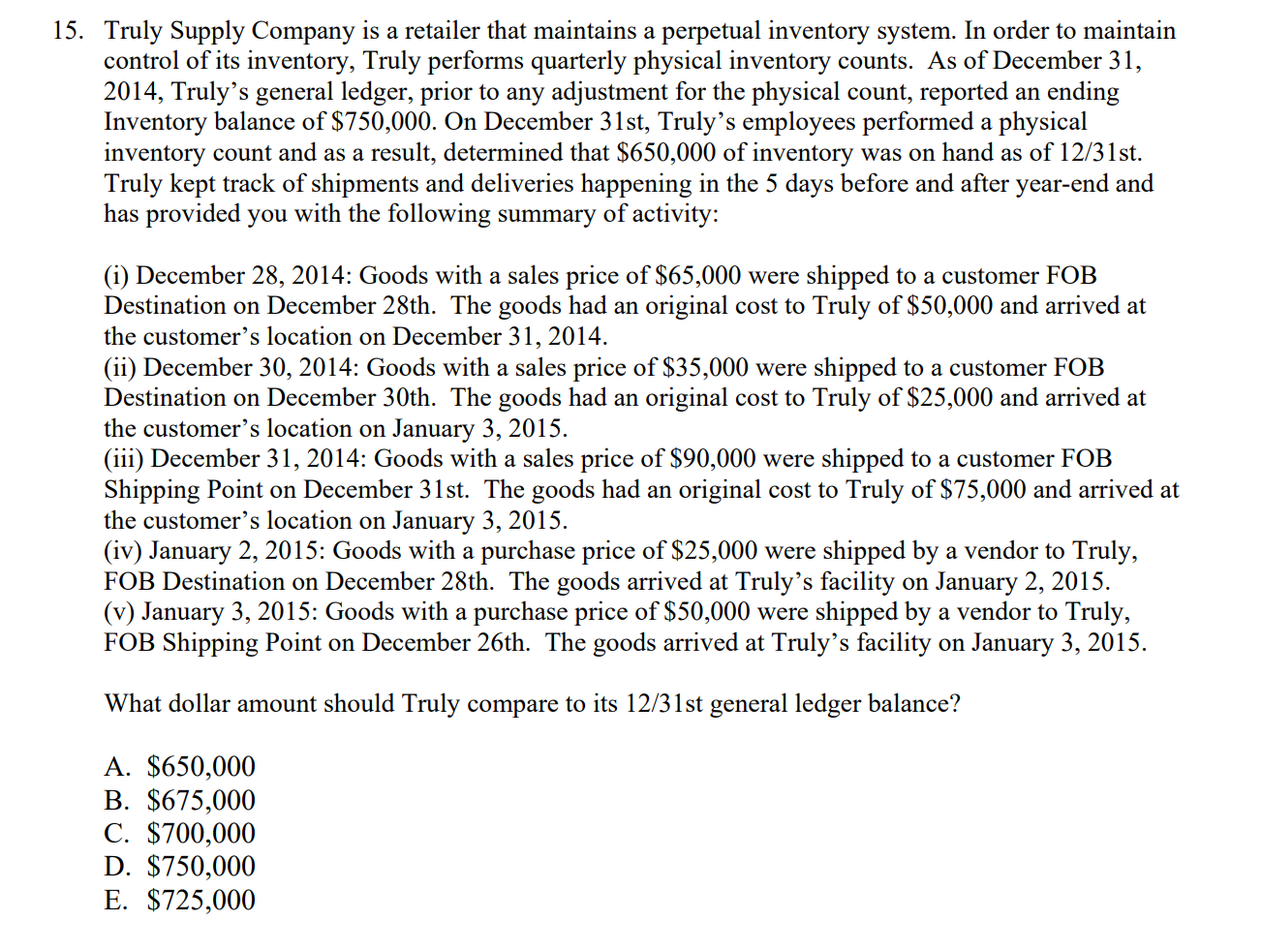

15. Truly Supply Company is a retailer that maintains a perpetual inventory system. In order to maintain control of its inventory, Truly performs quarterly physical

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Ethical Hacking The Ultimate Guide To Using Penetration Testing To Audit And Improve The Cybersecurity Of Computer Networks For Beginners Including Tips On Social Engineering

Authors: Lester Evans

1st Edition

1647481813, 978-1647481810