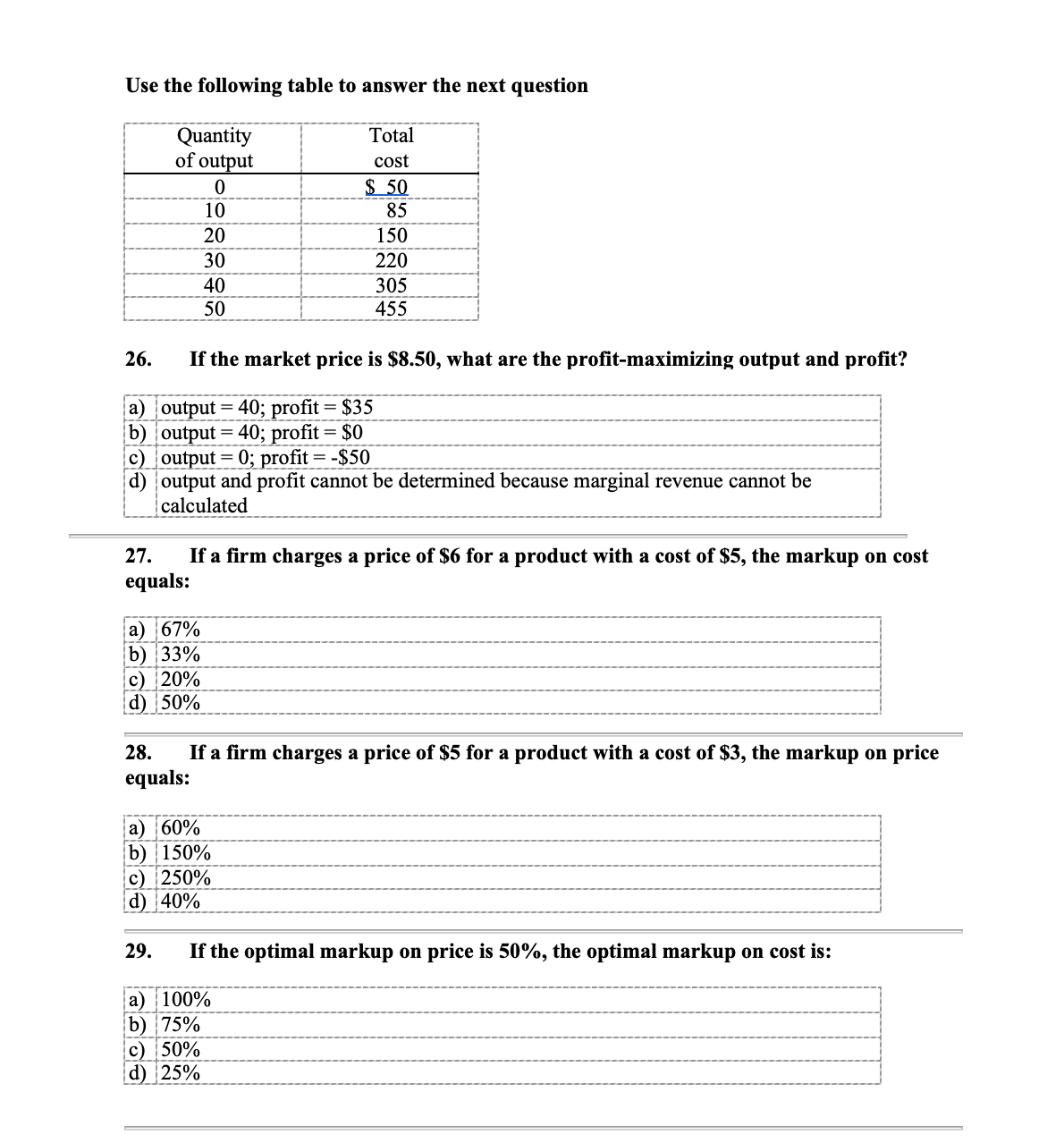

Question

16. If variable cost rises from $60 to $100 as output increases from 15 to 20 units, the marginal cost of the twentieth unit a)

16. If variable cost rises from $60 to $100 as output increases from 15 to 20 units, the marginal cost of the twentieth unit

a) is $100

b) is $5

c) is $40

d) is $8

17.Suppose Guild produces 5,000 guitars per year. Its average total cost is $90, and its fixed cost is $250,000. What is its variable cost?

a) $250,000

b) $450,000

c) $25,000

d) $200,000

18.If an increase in the price of a product from $1 to $2 per unit leads to a decrease in the quantity demanded from 100 to 80 units, then the value of price elasticity of demand is

a) -1/3

b) -2 1/3

c) -1/4

d) -3

19.So long as P > AVC, the competitive firm's short-run supply curve is equal to:

a) AVC

b) MC

c) P

d) none of these.

20.At the profit maximizing level of output for a monopolist:

a) P = AR and AR = AC

b) P > MC and MR = MC

c) P = MC and MR > MC

d) P = MR and AC = MC

21.Holding supply conditions constant, the costs of regulation fall wholly on producers when:

a) EP = 1

b) EP => 1

c) EP = ?

d) EP = 0

22.A 100% markup on cost is equivalent to a markup on price of:

a) 25%

b) 33%

c) 50%

d) 100%

23.A 25% markup on price is equivalent to a markup on cost of:

a) 25%

b) 33%

c) 50%

d) 100%

24.When EP = -3, the optimal markup on cost is:

a) 100%

b) 67%

c) 50%

d) 33%

25.When EP = -2, the optimal markup on price is:

a) 100%

b) 67%

c) 50%

d) 33%

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Capitalist Political Economy Thinkers And Theories

Authors: Heather Whiteside

1st Edition

0429888031, 9780429888038