Answered step by step

Verified Expert Solution

Question

1 Approved Answer

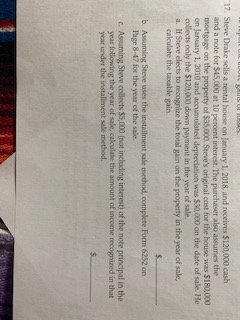

17. Steve Drake sells a rental house on January 1, 2018, and receives $120,000 cash and a note for $45,000 at 10 percent interest.The purchaser

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

College Accounting

Authors: Heintz and Parry

20th Edition

1285892070, 538489669, 9781111790301, 978-1285892078, 9780538489669, 1111790302, 978-0538745192