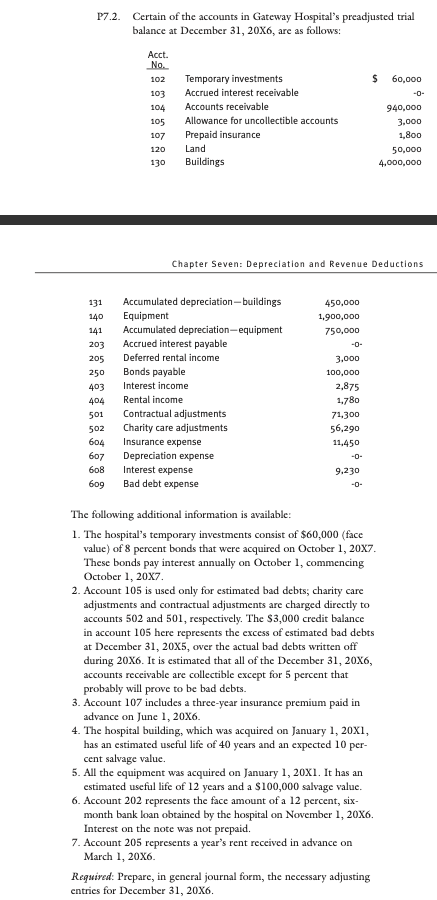

17.2. Certain of the accounts in Gateway Hospital's preadjusted trial balance at December 31, 20X6, are as follows: $ 60,000 Acct. No. 102 103 104 105 107 120 130 Temporary investments Accrued interest receivable Accounts receivable Allowance for uncollectible accounts Prepaid insurance Land Buildings 940,000 3.000 1,800 50,000 4.000.000 Chapter Seven: Depreciation and Revenue Deductions 450,000 1.900,000 750,000 131 140 141 203 205 250 403 404 501 502 604 607 608 609 Accumulated depreciation-buildings Equipment Accumulated depreciation-equipment Accrued interest payable Deferred rental income Bonds payable Interest income Rental income Contractual adjustments Charity care adjustments Insurance expense Depreciation expense Interest expense Bad debt expense 3,000 100,000 2,875 1.780 71,300 56,290 11.450 9.230 The following additional information is available: 1. The hospital's temporary investments consist of $60,000 (face value) of 8 percent bonds that were acquired on October 1, 20x7. These bonds pay interest annually on October 1, commencing October 1, 20x7. 2. Account 105 is used only for estimated bad debts, charity care adjustments and contractual adjustments are charged directly to accounts 502 and 501, respectively. The $3,000 credit balance in account 105 here represents the excess of estimated bad debts at December 31, 20x5, over the actual bad debts written off during 20X6. It is estimated that all of the December 31, 20X6, accounts receivable are collectible except for 5 percent that probably will prove to be bad debts. 3. Account 107 includes a three-year insurance premium paid in advance on June 1, 20X6. 4. The hospital building, which was acquired on January 1, 20x1, has an estimated useful life of 40 years and an expected 10 per- cent salvage value 5. All the equipment was acquired on January 1, 20X1. It has an estimated useful life of 12 years and a $100,000 salvage value. 6. Account 202 represents the face amount of a 12 percent, six- month bank loan obtained by the hospital on November 1, 20X6. Interest on the note was not prepaid. 7. Account 205 represents a year's rent received in advance on March 1, 20X6. Required: Prepare, in general journal form, the necessary adjusting entries for December 31, 20X6. 17.2. Certain of the accounts in Gateway Hospital's preadjusted trial balance at December 31, 20X6, are as follows: $ 60,000 Acct. No. 102 103 104 105 107 120 130 Temporary investments Accrued interest receivable Accounts receivable Allowance for uncollectible accounts Prepaid insurance Land Buildings 940,000 3.000 1,800 50,000 4.000.000 Chapter Seven: Depreciation and Revenue Deductions 450,000 1.900,000 750,000 131 140 141 203 205 250 403 404 501 502 604 607 608 609 Accumulated depreciation-buildings Equipment Accumulated depreciation-equipment Accrued interest payable Deferred rental income Bonds payable Interest income Rental income Contractual adjustments Charity care adjustments Insurance expense Depreciation expense Interest expense Bad debt expense 3,000 100,000 2,875 1.780 71,300 56,290 11.450 9.230 The following additional information is available: 1. The hospital's temporary investments consist of $60,000 (face value) of 8 percent bonds that were acquired on October 1, 20x7. These bonds pay interest annually on October 1, commencing October 1, 20x7. 2. Account 105 is used only for estimated bad debts, charity care adjustments and contractual adjustments are charged directly to accounts 502 and 501, respectively. The $3,000 credit balance in account 105 here represents the excess of estimated bad debts at December 31, 20x5, over the actual bad debts written off during 20X6. It is estimated that all of the December 31, 20X6, accounts receivable are collectible except for 5 percent that probably will prove to be bad debts. 3. Account 107 includes a three-year insurance premium paid in advance on June 1, 20X6. 4. The hospital building, which was acquired on January 1, 20x1, has an estimated useful life of 40 years and an expected 10 per- cent salvage value 5. All the equipment was acquired on January 1, 20X1. It has an estimated useful life of 12 years and a $100,000 salvage value. 6. Account 202 represents the face amount of a 12 percent, six- month bank loan obtained by the hospital on November 1, 20X6. Interest on the note was not prepaid. 7. Account 205 represents a year's rent received in advance on March 1, 20X6. Required: Prepare, in general journal form, the necessary adjusting entries for December 31, 20X6