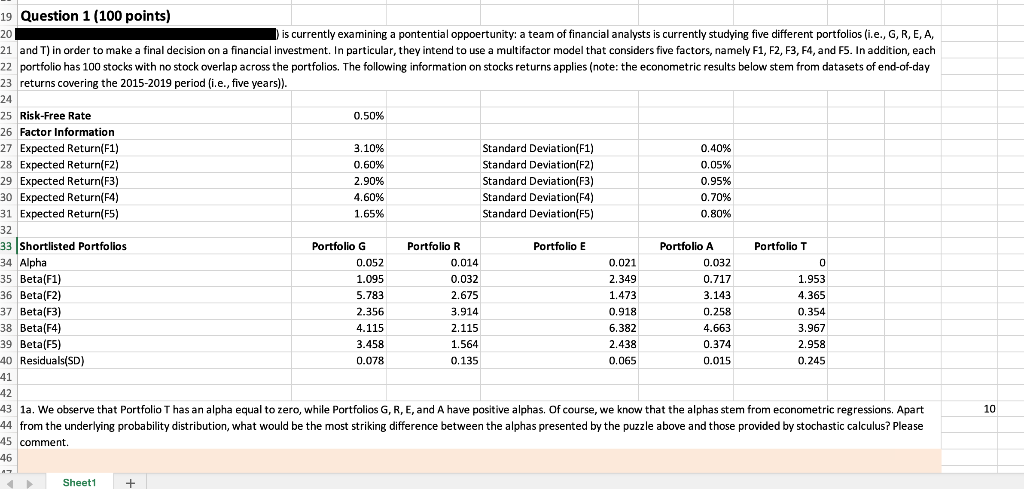

19 Question 1 (100 points) 20 is currently examining a pontential oppoertunity: a team of financial analysts is currently studying five different portfolios (i.e., G, R, E, A, 21 and T) in order to make a final decision on a financial investment. In particular, they intend to use a multifactor model that considers five factors, namely F1, F2, F3, F4, and F5. In addition, each 22 portfolio has 100 stocks with no stock overlap across the portfolios. The following information on stocks returns applies (note: the econometric results below stem from datasets of end-of-day 23 returns covering the 2015-2019 period (i.e., five years)). 24 25 Risk-Free Rate 0.50% 26 Factor Information 27 Expected Return(F1) 3.10% Standard Deviation(F1) 0.40% 28 Expected Return(F2) 0,60% Standard Deviation(F2) 0.05% 29 Expected Return(F3) 2.90% Standard Deviation(F3) 0.95% 30 Expected Return(4) 4.60% Standard Deviation(F4) 0.70% 31 Expected Return(F5) 1,65% Standard Deviation(F5) 0.80% 32 33 Shortlisted Portfolios Portfolio G Portfolio R Portfolio E Portfolio A Portfolio T 34 Alpha 0.052 0.014 0.021 0.032 0 35 Beta(F1) 1.095 0.032 2.349 0.717 1.953 36 Beta(F2) 5.783 2.675 1.473 3.143 4.365 37 Beta(F3) 2.356 3.914 0.918 0.258 0.354 38 Beta(F4) 4.115 2.115 6.382 4.663 3.967 39 Beta(F5) 3.458 1.564 2.438 0.374 2.958 40 Residuals(SD) 0.078 0.135 0.065 0.015 0.245 41 42 12 43 1a. We observe that Portfolio T has an alpha equal to zero, while Portfolios G, R, E, and A have positive alphas. Of course, we know that the alphas stem from econometric regressions. Apart 44 from the underlying probability distribution, what would be the most striking difference between the alphas presented by the puzzle above and those provided by stochastic calculus? Please 45 comment. 46 10 Sheet1 + 19 Question 1 (100 points) 20 is currently examining a pontential oppoertunity: a team of financial analysts is currently studying five different portfolios (i.e., G, R, E, A, 21 and T) in order to make a final decision on a financial investment. In particular, they intend to use a multifactor model that considers five factors, namely F1, F2, F3, F4, and F5. In addition, each 22 portfolio has 100 stocks with no stock overlap across the portfolios. The following information on stocks returns applies (note: the econometric results below stem from datasets of end-of-day 23 returns covering the 2015-2019 period (i.e., five years)). 24 25 Risk-Free Rate 0.50% 26 Factor Information 27 Expected Return(F1) 3.10% Standard Deviation(F1) 0.40% 28 Expected Return(F2) 0,60% Standard Deviation(F2) 0.05% 29 Expected Return(F3) 2.90% Standard Deviation(F3) 0.95% 30 Expected Return(4) 4.60% Standard Deviation(F4) 0.70% 31 Expected Return(F5) 1,65% Standard Deviation(F5) 0.80% 32 33 Shortlisted Portfolios Portfolio G Portfolio R Portfolio E Portfolio A Portfolio T 34 Alpha 0.052 0.014 0.021 0.032 0 35 Beta(F1) 1.095 0.032 2.349 0.717 1.953 36 Beta(F2) 5.783 2.675 1.473 3.143 4.365 37 Beta(F3) 2.356 3.914 0.918 0.258 0.354 38 Beta(F4) 4.115 2.115 6.382 4.663 3.967 39 Beta(F5) 3.458 1.564 2.438 0.374 2.958 40 Residuals(SD) 0.078 0.135 0.065 0.015 0.245 41 42 12 43 1a. We observe that Portfolio T has an alpha equal to zero, while Portfolios G, R, E, and A have positive alphas. Of course, we know that the alphas stem from econometric regressions. Apart 44 from the underlying probability distribution, what would be the most striking difference between the alphas presented by the puzzle above and those provided by stochastic calculus? Please 45 comment. 46 10 Sheet1 +