Answered step by step

Verified Expert Solution

Question

1 Approved Answer

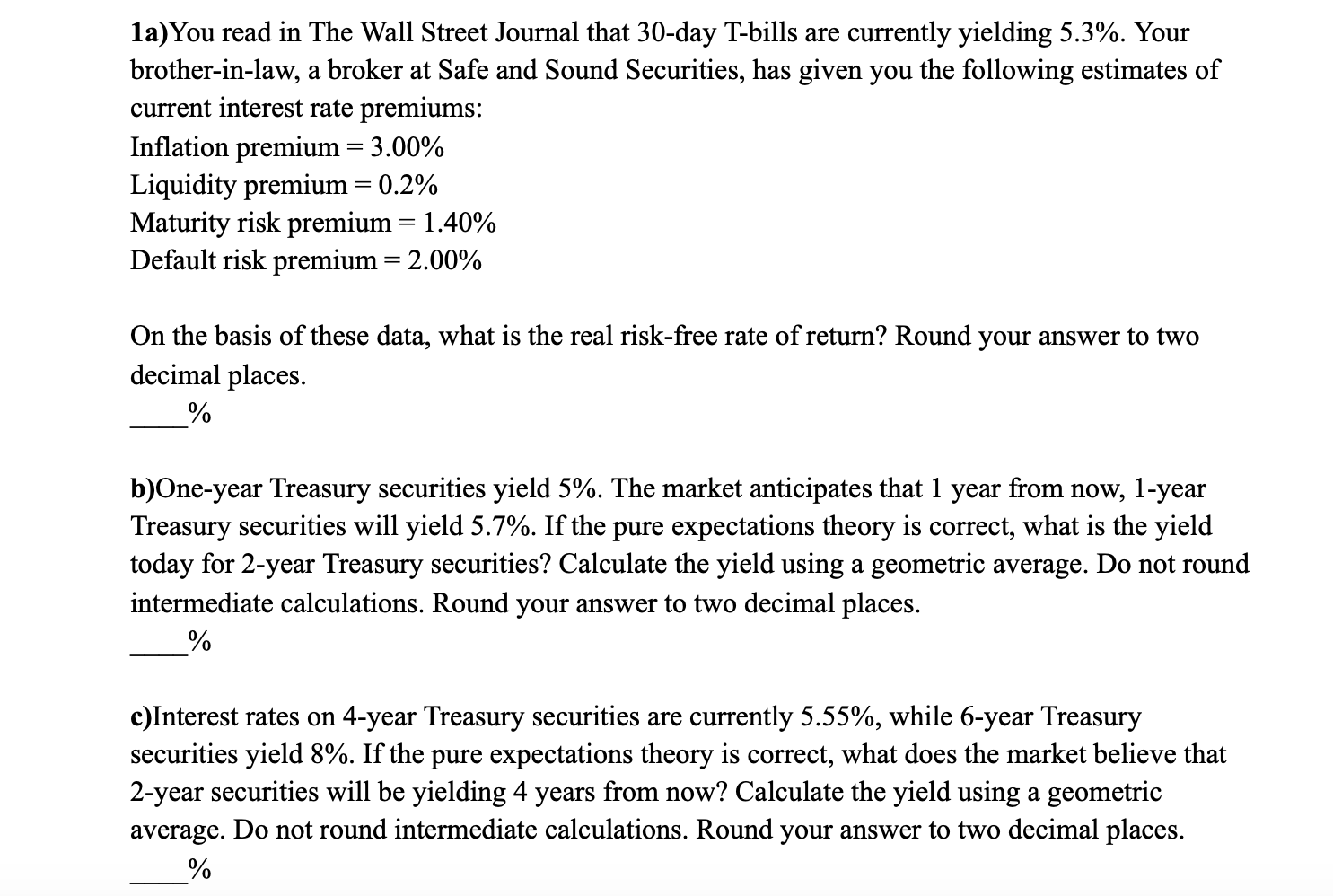

1a)You read in The Wall Street Journal that 30-day T-bills are currently yielding 5.3%. Your brother-in-law, a broker at Safe and Sound Securities, has given

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Sitting Pretty On A Fixed Income Personal Finance Secrets For Seniors

Authors: FC&A Medical Publishing

1st Edition

1935574582, 9781935574583