Answered step by step

Verified Expert Solution

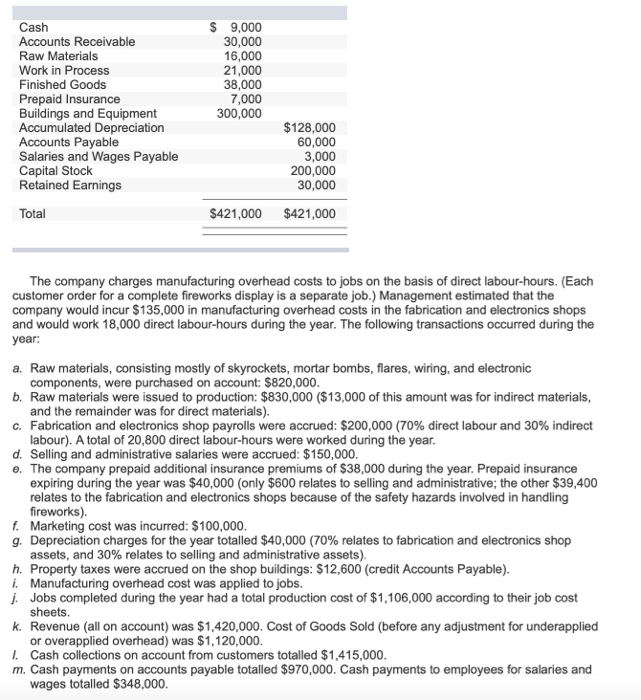

Question

1 Approved Answer

1.Prepare journal entries for the years transactions. (Do not round intermediate calculations. If no entry is required for a transaction/event, select No journal entry required

1.Prepare journal entries for the years transactions. (Do not round intermediate calculations. If no entry is required for a transaction/event, select "No journal entry required" in the first account field.)

2.Prepare a T-account for each account in the companys trial balance, and enter the opening balances given above. Post your journal entries to the T-accounts. Prepare new T-accounts as needed. Compute the ending balance in each account.

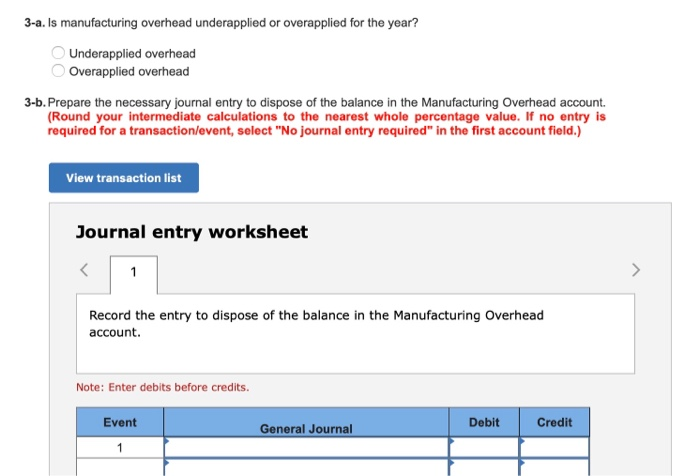

4.Prepare an income statement for the year. (Do not prepare a statement of cost of goods manufactured; all of the information needed for the income statement is available in the T-accounts.)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Audit Effectiveness Meeting The IT Challenge

Authors: Kamil Omoteso

1st Edition

1409434680, 978-1409434689