Answered step by step

Verified Expert Solution

Question

1 Approved Answer

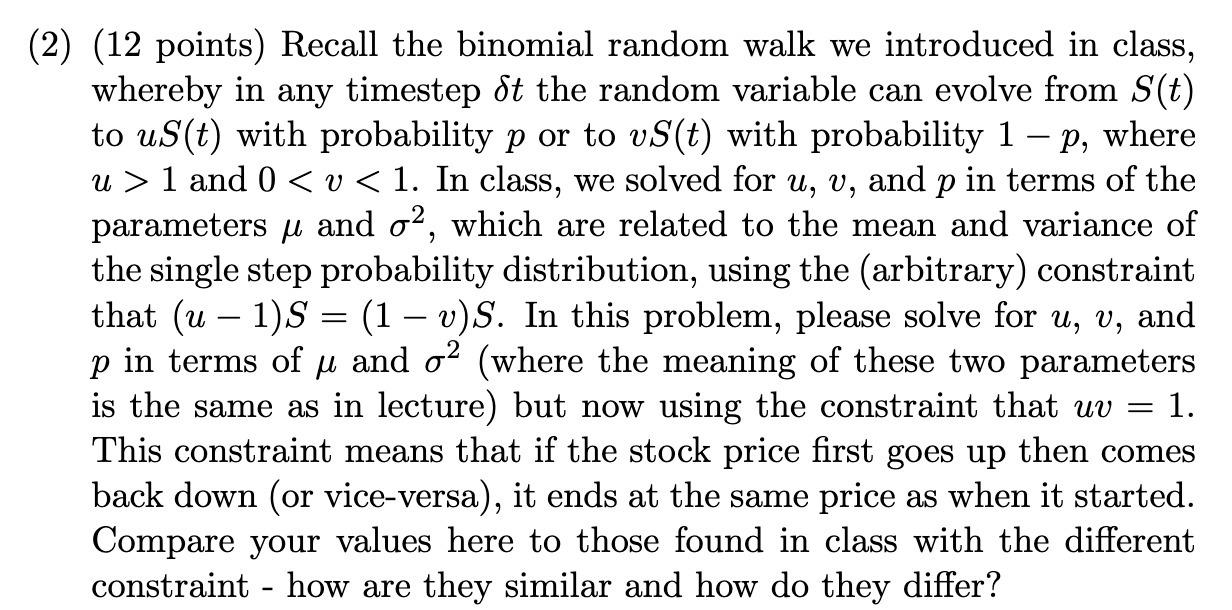

(2) (12 points) Recall the binomial random walk we introduced in class, whereby in any timestep dt the random variable can evolve from S(t)

(2) (12 points) Recall the binomial random walk we introduced in class, whereby in any timestep dt the random variable can evolve from S(t) to uS(t) with probability p or to vS(t) with probability 1-p, where u >1 and 0 < v < 1. In class, we solved for u, v, and p in terms of the parameters and o, which are related to the mean and variance of the single step probability distribution, using the (arbitrary) constraint that (u 1)S = (1 - v)S. In this problem, please solve for u, v, and p in terms of u and o (where the meaning of these two parameters is the same as in lecture) but now using the constraint that uv = 1. This constraint means that if the stock price first goes up then comes back down (or vice-versa), it ends at the same price as when it started. Compare your values here to those found in class with the different constraint - how are they similar and how do they differ? -

Step by Step Solution

★★★★★

3.35 Rating (170 Votes )

There are 3 Steps involved in it

Step: 1

To solve for u v and p in terms of and with the constraint uv 1 we can use the following steps 1 Sta...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Understanding Basic Statistics

Authors: Charles Henry Brase, Corrinne Pellillo Brase

6th Edition

978-1133525097, 1133525091, 1111827028, 978-1133110316, 1133110312, 978-1111827021