Answered step by step

Verified Expert Solution

Question

1 Approved Answer

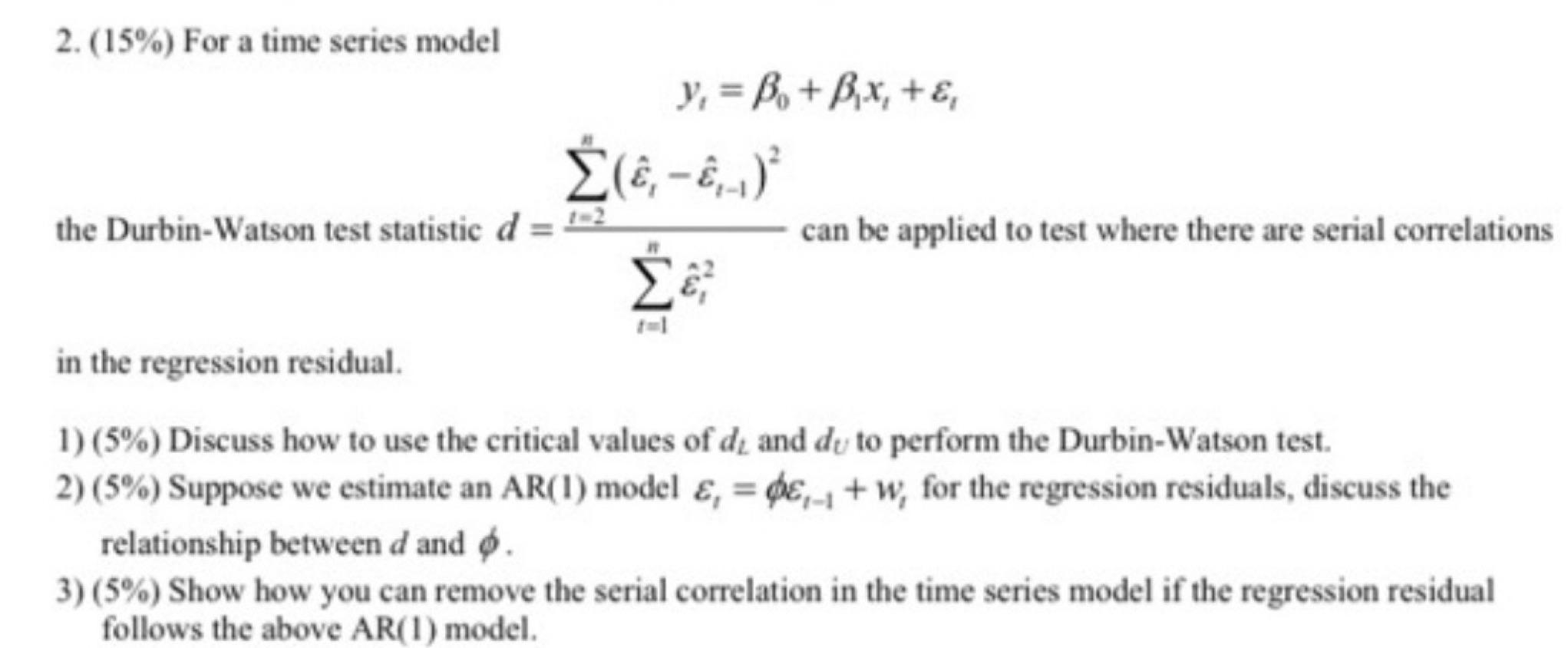

2. (15%) For a time series model the Durbin-Watson test statistic d y = B + Bx + (,-,.,) can be applied to test

2. (15%) For a time series model the Durbin-Watson test statistic d y = B + Bx + (,-,.,) can be applied to test where there are serial correlations in the regression residual. 1) (5%) Discuss how to use the critical values of de and de to perform the Durbin-Watson test. 2) (5%) Suppose we estimate an AR(1) model , =de,+w, for the regression residuals, discuss the relationship between d and . 3) (5%) Show how you can remove the serial correlation in the time series model if the regression residual follows the above AR(1) model.

Step by Step Solution

★★★★★

3.34 Rating (166 Votes )

There are 3 Steps involved in it

Step: 1

1 To perform the DurbinWatson test you compare the calculated DurbinWatson statistic d to the critic...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Applied Regression Analysis And Other Multivariable Methods

Authors: David G. Kleinbaum, Lawrence L. Kupper, Azhar Nizam, Eli S. Rosenberg

5th Edition

1285051084, 978-1285963754, 128596375X, 978-1285051086