Answered step by step

Verified Expert Solution

Question

1 Approved Answer

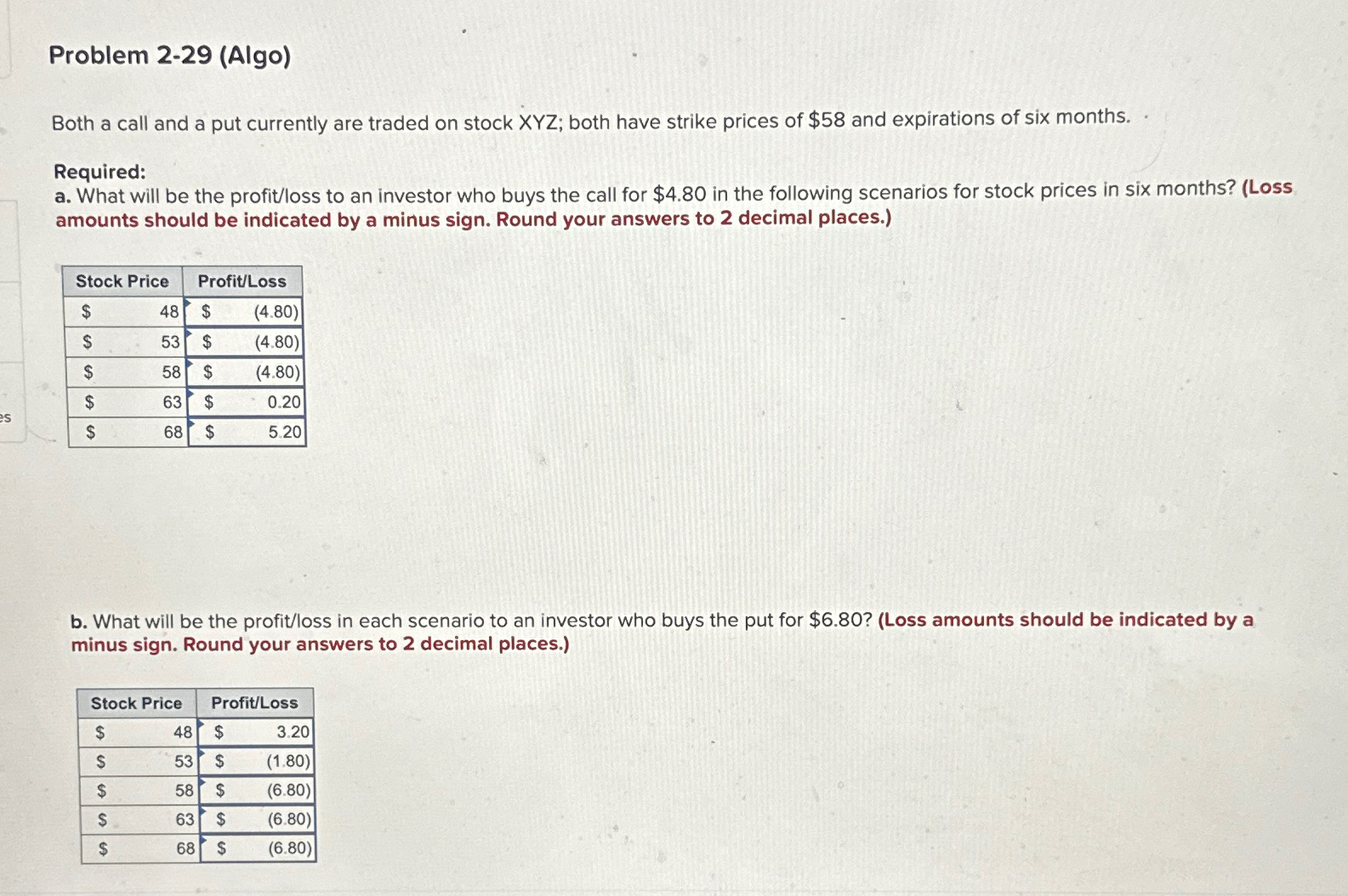

2 - 2 9 ( Algo ) Both a call and a put currently are traded on stock XYZ; both have strike prices of $

Algo

Both a call and a put currently are traded on stock XYZ; both have strike prices of $ and expirations of six months.

Required:

a What will be the profitloss to an investor who buys the call for $ in the following scenarios for stock prices in six months? Loss amounts should be indicated by a minus sign. Round your answers to decimal places.

tableS

tock Price,Profi

Can you please explain the math on how to get this answer

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Market Audit And Analysis

Authors: Nicole Lorat

1st Edition

3640438892, 978-3640438891