Answered step by step

Verified Expert Solution

Question

1 Approved Answer

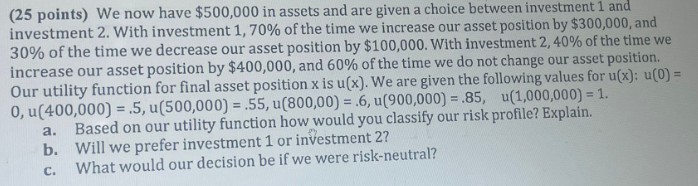

( 2 5 points ) We now have $ 5 0 0 , 0 0 0 in assets and are given a choice between investment

points We now have $ in assets and are given a choice between investment and

investment With investment of the time we increase our asset position by $ and

of the time we decrease our asset position by $ With investment of the time we

increase our asset position by $ and of the time we do not change our asset position.

Our utility function for final asset position is We are given the following values for :

a Based on our utility function how would you classify our risk profile? Explain.

b Will we prefer investment or investment

c What would our decision be if we were riskneutral?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Survey of Accounting

Authors: Edmonds, old, Mcnair, Tsay

2nd edition

9780077392659, 978-0-07-73417, 77392655, 0-07-734177-5, 73379557, 978-0073379555