Answered step by step

Verified Expert Solution

Question

1 Approved Answer

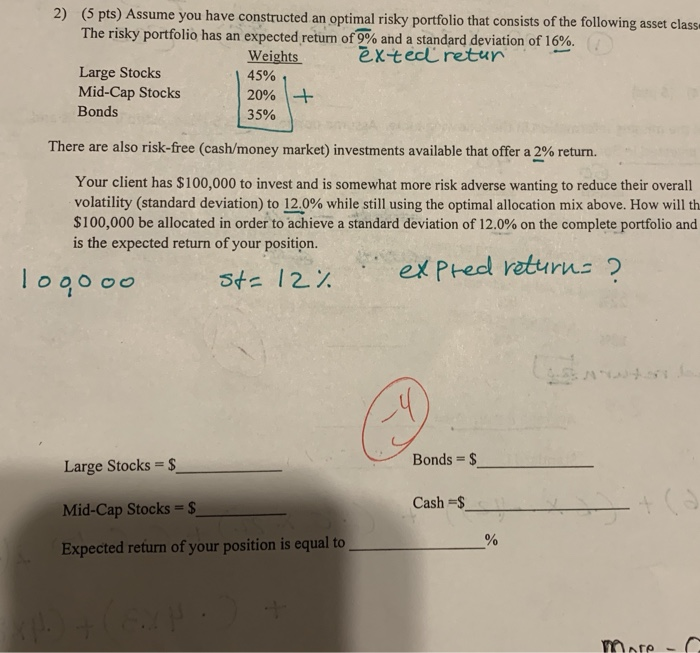

2) (5 pts) Assume you have constructed an optimal risky portfolio that consists of the following asset class The risky portfolio has an expected return

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Principles Of Managerial Finance

Authors: Lawrence J. Gitman, Chad J. Zutter

13th Edition

9780132738729, 136119468, 132738724, 978-0136119463