Answered step by step

Verified Expert Solution

Question

1 Approved Answer

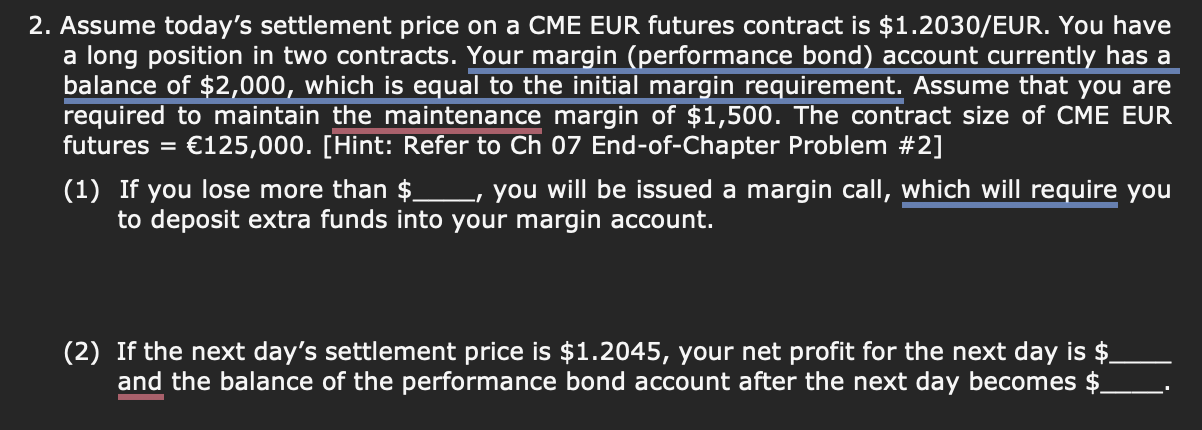

2. Assume today's settlement price on a CME EUR futures contract is $1.2030/EUR. You have a long position in two contracts. Your margin (performance bond)

2. Assume today's settlement price on a CME EUR futures contract is $1.2030/EUR. You have a long position in two contracts. Your margin (performance bond) account currently has a balance of $2,000, which is equal to the initial margin requirement. Assume that you are required to maintain the maintenance margin of $1,500. The contract size of CME EUR futures =125,000. [Hint: Refer to Ch 07 End-of-Chapter Problem \#2] (1) If you lose more than \$ , you will be issued a margin call, which will require you to deposit extra funds into your margin account. (2) If the next day's settlement price is $1.2045, your net profit for the next day is $ and the balance of the performance bond account after the next day becomes $

2. Assume today's settlement price on a CME EUR futures contract is $1.2030/EUR. You have a long position in two contracts. Your margin (performance bond) account currently has a balance of $2,000, which is equal to the initial margin requirement. Assume that you are required to maintain the maintenance margin of $1,500. The contract size of CME EUR futures =125,000. [Hint: Refer to Ch 07 End-of-Chapter Problem \#2] (1) If you lose more than \$ , you will be issued a margin call, which will require you to deposit extra funds into your margin account. (2) If the next day's settlement price is $1.2045, your net profit for the next day is $ and the balance of the performance bond account after the next day becomes $ Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Chains Of Finance How Investment Management Is Shaped

Authors: Diane-Laure Arjalies, Philip Grant, Iain Hardie, Donald MacKenzie, Ekaterina Svetlova

1st Edition

0198802943, 978-0198802945