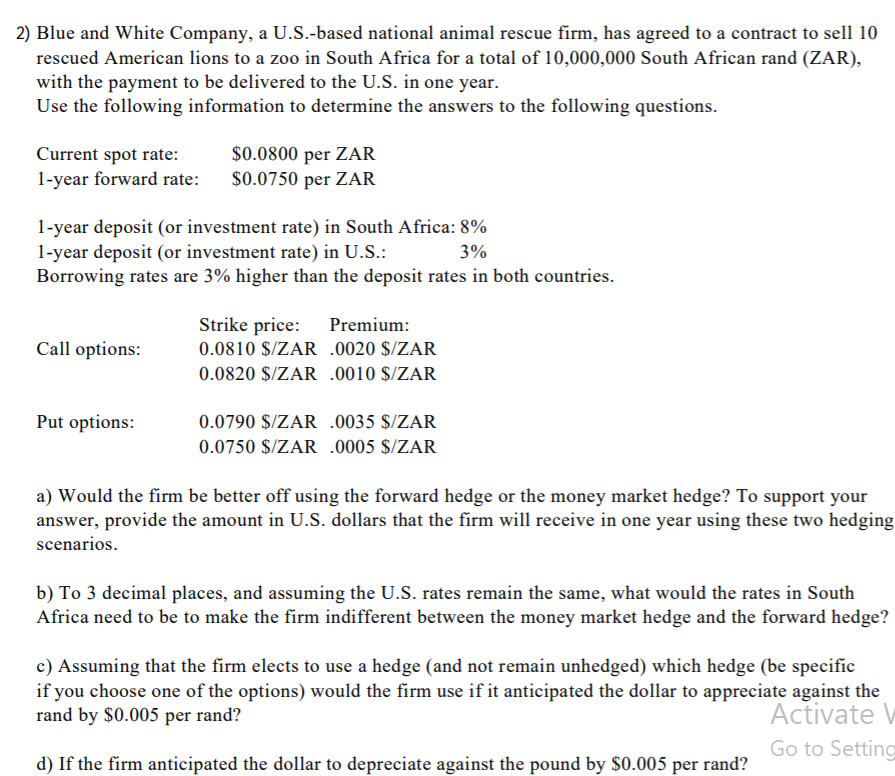

2) Blue and White Company, a U.S.-based national animal rescue firm, has agreed to a contract to sell 10 rescued American lions to a zoo in South Africa for a total of 10,000,000 South African rand (ZAR), with the payment to be delivered to the U.S. in one year. Use the following information to determine the answers to the following questions. Current spot rate: 1-year forward rate: $0.0800 per ZAR $0.0750 per ZAR 1-year deposit (or investment rate) in South Africa: 8% 1-year deposit (or investment rate) in U.S.: 3% Borrowing rates are 3% higher than the deposit rates in both countries. Call options: Strike price: Premium: 0.0810 $/ZAR .0020 $/ZAR 0.0820 $/ZAR .0010 $/ZAR Put options: 0.0790 $/ZAR .0035 $/ZAR 0.0750 $/ZAR .0005 $/ZAR a) Would the firm be better off using the forward hedge or the money market hedge? To support your answer, provide the amount in U.S. dollars that the firm will receive in one year using these two hedging scenarios. b) To 3 decimal places, and assuming the U.S. rates remain the same, what would the rates in South Africa need to be to make the firm indifferent between the money market hedge and the forward hedge? c) Assuming that the firm elects to use a hedge (and not remain unhedged) which hedge (be specific if you choose one of the options) would the firm use if it anticipated the dollar to appreciate against the rand by $0.005 per rand? Activate Go to Setting d) If the firm anticipated the dollar to depreciate against the pound by $0.005 per rand? 2) Blue and White Company, a U.S.-based national animal rescue firm, has agreed to a contract to sell 10 rescued American lions to a zoo in South Africa for a total of 10,000,000 South African rand (ZAR), with the payment to be delivered to the U.S. in one year. Use the following information to determine the answers to the following questions. Current spot rate: 1-year forward rate: $0.0800 per ZAR $0.0750 per ZAR 1-year deposit (or investment rate) in South Africa: 8% 1-year deposit (or investment rate) in U.S.: 3% Borrowing rates are 3% higher than the deposit rates in both countries. Call options: Strike price: Premium: 0.0810 $/ZAR .0020 $/ZAR 0.0820 $/ZAR .0010 $/ZAR Put options: 0.0790 $/ZAR .0035 $/ZAR 0.0750 $/ZAR .0005 $/ZAR a) Would the firm be better off using the forward hedge or the money market hedge? To support your answer, provide the amount in U.S. dollars that the firm will receive in one year using these two hedging scenarios. b) To 3 decimal places, and assuming the U.S. rates remain the same, what would the rates in South Africa need to be to make the firm indifferent between the money market hedge and the forward hedge? c) Assuming that the firm elects to use a hedge (and not remain unhedged) which hedge (be specific if you choose one of the options) would the firm use if it anticipated the dollar to appreciate against the rand by $0.005 per rand? Activate Go to Setting d) If the firm anticipated the dollar to depreciate against the pound by $0.005 per rand